2021년4분기 디램 가격 3-8% 하락 예상

2021.09.23

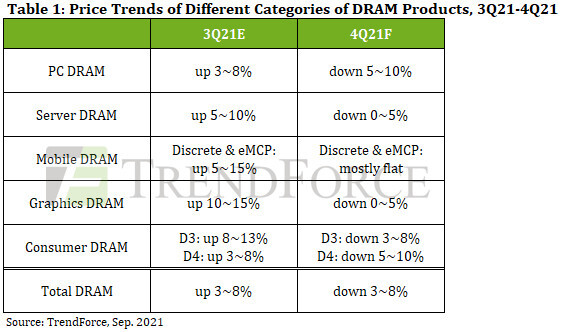

고객사 재고 증가로 2021년4분기 디램 계약가격은 3-8% 하락 예상.

PC 디램은 노트북 수용 약화로 5-10% 하락 예상.

서버 디램은 고객사 재고 부담으로 0-5% 하락 예상.

모바일 디램은 3분기와 비슷할 것.

그래픽 디램은 공급 과잉으로 0-5% 하락 예상.

DRAM Prices Projected to Decline by 3-8% QoQ in 4Q21 Due to Rising Level of Client Inventory, Says TrendForce

시장조사업체 트렌드포스는 4분기 디램 고정 가격은 고객사들의 재고 증가로 3-8%정도 하락할 것으로 분석했다.

Following the peak period of production in 3Q21, the supply of DRAM will likely begin to outpace demand in 4Q21, according to TrendForce’s latest investigations (the surplus of DRAM supply is henceforth referred to as “sufficiency ratio”, expressed as a percentage).

3분기 디램 생산이 정점을 찍으면서, 4분기 디램 공급은 수요를 초과하기 시작할 것같다고 트렌드포스는

최근 퍼센드로 나타내는 "공급충족률"로 공급과잉으로 분석했다.

In addition, while DRAM suppliers are generally carrying a healthy level of inventory, most of their clients in the end-product markets are carrying a higher level of DRAM inventory than what is considered healthy, meaning these clients will be less willing to procure additional DRAM going forward.

게다가 디램 공급자들은 건전한 재고 수준을 가지고 있으나, 디램 수요자들의 재고 수준은 정상적인 수준보다

높아서, 디램 수요자들은 더 많은 재고를 가지길 꺼리고 있다.

TrendForce therefore forecasts a downward trajectory for DRAM ASP in 4Q21. More specifically, DRAM products that are currently in oversupply may experience price drops of more than 5% QoQ, and the overall DRAM ASP will likely decline by about 3-8% QoQ in 4Q21.

그래서 트렌드포스는 4분기 디램 판매 가격이 하락할 것으로 예상했다.

특히 과잉 공급인 디램 제품은 4분기에 저분기대비 5%이상 하락할 것이고, 전체적으로

디램 평균 판매 가격은 3-8%정도 하락할 것이다.

PC DRAM prices are expected to decline by 5-10% QoQ as market demand for notebook computers weakens

PC디램 가격은 노트북 수요가 약해지기때문에 전분기대비 5-10% 하락할 것이다.

Although WFH and distance learning applications previously generated high demand for notebook computers, increasingly widespread vaccinations in Europe and North America have now weakened this demand, particularly for Chromebooks.

As a result, global production of notebooks is expected to decline in 4Q21, in turn propelling the sufficiency ratio of PC DRAM to 1.38%, which indicates that PC DRAM will no longer be in short supply in 4Q21. However, PC DRAM accounts for a relatively low share of DRAM manufacturers’ DRAM supply bits, since these suppliers have allocated more production capacities to server DRAM, which is in relatively high demand. Hence, there will unlikely be a severe surplus of PC DRAM in 4Q21. It should also be pointed out that, on average, the current spot prices of PC DRAM modules are far lower than their contract prices for 3Q21. TrendForce therefore expects an imminent 5-10% QoQ decline in PC DRAM contract prices for 4Q21, with potential for declines that are even greater than 10% for certain transactions, as PC OEMs anticipate further price drops in PC DRAM prices in the future.

Server DRAM prices are expected to decline for the first time this year, by 0-5% QoQ due to high client-side inventory

CSPs in North America and China currently carry more than eight weeks’ worth of server DRAM inventory, with some carrying more than 10 weeks’ worth of inventory, as they procured massive amounts of server DRAM in the previous two quarters to avoid shipment issues with whole server units caused by component shortages. In view of this aggressive procurement effort, the overall demand for server DRAM has gradually slowed, although certain Tier 2 data centers are still procuring server DRAM to make up for previous gaps. As server DRAM buyers continue to gravitate towards destocking their server DRAM inventory in 4Q21, demand will likely fall short of the previous quarters. Furthermore, due to long lead times for certain key components, shipment of whole servers is also expected to undergo quarterly declines. On the supply side, the three major DRAM suppliers (Samsung, SK hynix, and Micron) reallocated some of their production capacity for mobile DRAM to server DRAM in early 2Q21, and this reallocated capacity is expected to gradually begin outputting server DRAM in 4Q21. Given the slowdown in server DRAM demand, contract negotiations for server DRAM procurement in 3Q21 lasted until early August. Although server DRAM contract prices underwent a 5-10% QoQ increase in 3Q21 due to suppliers’ best attempts during contract negotiations, further price hikes going forward are unlikely. TrendForce expects server DRAM prices to undergo a decline for the first time this year in 4Q21 with a QoQ drop of 0-5%.

Mobile DRAM prices are expected to remain relative unchanged from 3Q21 levels despite a possible price drop ahead of time at the end of the year

In light of fluctuations in the COVID-19 pandemic, the global demand for smartphones and the supply of smartphone components are both still at the risk of experiencing declines. In addition, after smartphone brands revised down their production targets at the end of 2Q21, brands and distributors alike have been facing the pressure of high smartphone inventory levels. In response to factors such as pandemic-related uncertainties and declines in mobile DRAM prices for 2022, smartphone brands will slow down their mobile DRAM procurement and prioritize inventory reduction instead. Hence, bit demand for mobile DRAM will decline even further in 4Q21. On the whole, given the uncertain state of the pandemic in the coming winter, smartphone brands will adopt a more conservative attitude towards both smartphone production and component procurement in 4Q21. As a result, even if DRAM suppliers are willing to lower mobile DRAM prices, such an effort will only result in limited sales growths. In addition, mobile DRAM still lags behind other DRAM product categories in terms of profitability, meaning a drop in mobile DRAM prices is unlikely. Taking these factors into account, TrendForce expects prices of discrete DRAM, eMCP, and uMCP to mostly hold flat in 4Q21 compared with 3Q21.

It should be noted that, by the end of the year, DRAM suppliers may potentially start supplying mobile DRAM at 1Q22 prices ahead of time, primarily for two reasons: First, DRAM suppliers will be faced with revenue performance pressures at the end of the year; second, smartphones and DRAM suppliers will enter into new LTAs (long term agreements) for 2022. These factors are expected to impact mobile DRAM ASP for 4Q21 and bring about a price drop ahead of time.

Graphics DRAM contract prices are expected to decline by 0-5% QoQ due to excess supply

Market demand for discrete graphics cards and notebook graphics cards still remains due to the stable market for commercial notebooks and the resurging cryptocurrency mining market, which saw cryptocurrency prices rebounding from rock bottom levels within the past two months. However, severe issues with the availability of components in the graphics card supply chain currently present the most significant bottleneck in graphics card production. In particular, components such as driver IC, PMIC, and other peripheral components are all in shortage, while graphics DRAM is in relative oversupply compared to these other components. Graphics card manufacturers are therefore revising down their graphics DRAM procurement. Consequently, even though DRAM suppliers have not significantly increased their graphics DRAM production, demand from the purchasing end will remain sluggish until the shortage of other components is resolved. Demand for graphics DRAM will unlikely see a resurgence before the end of 2021. On the supply side, the three major DRAM suppliers are primarily focused on GDDR6 for their current graphics DRAM production. As well, graphics card demand from the cryptocurrency mining market is generally aimed at newer graphics cards that feature GDDR6 memory. Accordingly, both production and sales of GDDR5 memory are relatively weak, and this bearish trend is especially reflected in spot prices. As spot prices are the first to enter a downturn, and the aforementioned market conditions lead to sluggish procurement activities, graphics DRAM prices are in turn expected to plummet from previous levels in 4Q21, although this decline is projected at a minor 0-5% QoQ owing to DRAM suppliers’ efforts to keep prices constant.

QoQ decline of DDR4 Consumer DRAM prices is expected to be among the highest drops, at 5-10% as procurement activities decelerate

Gradual easing of lockdowns in Europe and North America has led to a decline in consumer spending on home entertainment applications. This, along with the severe shortage in electronic components, has adversely affected the demand for consumer electronics, such as TVs, STBs (set-top boxes), and networking devices, as well as industrial-use products, thereby also reducing the procurement demand for consumer DRAM. On the other hand, while DRAM suppliers were in the process of transitioning from DDR3 manufacturing to other products, the massive price hike of DDR3 products in 1H21 led DRAM suppliers to slow this transition. Even so, certain market conditions are now placing downward pressure on DDR3 prices, so next year the three major suppliers may potentially speed up the transition of mature DDR3 manufacturing to other products, such as CMOS image sensors or other logic ICs, instead. As server and PC manufacturers’ DRAM inventory level rises, contract prices of those DRAM products will likely decline in 4Q21. Thus, given that the movement of DDR4 consumer DRAM prices is highly correlated with PC DRAM and server DRAM and has been trending relatively high, DDR4 consumer DRAM prices are expected to decline by 5-10% QoQ in 4Q21. Likewise, although the supply of DDR3 consumer DRAM has been gradually decreasing, DDR3 consumer DRAM prices will also undergo an overall decline, particularly for 4Gb chips. DDR3 consumer DRAM prices are expected to decline by 3-8% QoQ in 4Q21.

----------------------------------------------------

2021.10.18

"4분기 모바일 D램 가격 유지 또는 소폭 상승 전망"-삼성 (newstomato.com)

[뉴스토마토 최성남 기자] 삼성증권은 18일 올 4분기 모바일 디램 가격은 유지 또는 소폭 상승할 것이라며 4분기 시장의 가격 전망은 틀린 것으로 판단된다고 밝혔다.

이 증권사 황민성 연구원은 "크게 내릴 것이라던 4분기 디램 가격은 거의 보합 수준으로 예상된다"면서 "가격이 떨어지길 기다리던 구매 전략은 잘 통하지 않는다. 구매와 판매 모두 관습적인 패턴에 대해 다시 생각해볼 시점"이라고 판단했다.

황 연구원은 "시장의 단기적인 가격에 대한 의견은 주로 주요 고객의 희망을 대변하는 경우가 많다"며 "예를 들어 HP나 아마존 같은 고객이 얼마의 가격을 희망한다면 시장 조사를 하는 입장에서는 그 의견을 따라가는 것은 나쁜 선택이 아니지만, 그러나 자꾸 틀린다면 같은 방식을 고집하는 것은 문제가 있다"고 지적했다.

그는 "기다리면 가격을 반드시 깎을 수 있으며, 하지만 가격 조금 깎으려다 나중에 물량 확보 못하는 소탐대실을 걱정할 필요가 있다"면서도 "4분기가 막 시작한 초입인 현재 아마 고객 모두가 기다린다면 이는 수요가 나쁘지 않다는 의미이기 때문에 당초 가격 인하를 목표했던 고객의 협상정책을 듣고 (가격은 내릴 것이다, 주문을 줄일 것이다)라는 큰 폭의 가격하락을 예상했다면 좀더 균형 잡힌 시각이 필요하다"고 분석했다.

따라서 그는 "영업마진 40% 이상을 내는 SK하이닉스(000660)가 PBR(주가순자산비율) 1배에 거래된다면 이는 그만큼 시장이 사이클 논란에 무관심하다는 것을 반증하고 있는 것"이며 "인플레이션으로 가격이 오르는 곳이 여기저기 보이는 상황에 굳이 사이클 논란이 심하고 가격이 내릴 것 같은 상품을 사고 싶은 사람은 많지 않지만, 틀린 것은 틀린가격(Misprice)가 됐다는 것이며, 이것은 투자자에게 언제나 기회로 작용한다"고 덧붙였다.

최성남 기자 drksn@etomato.com