2025.06..17

2 No-Brainer Artificial Intelligence (AI) Stocks to Buy Right Now

2 No-Brainer Artificial Intelligence (AI) Stocks to Buy Right Now

지금 당장 매수해야 할 '고민할 필요 없는' 인공지능(AI) 관련 주식 2종

핵심 요점

- AI 하드웨어 및 소프트웨어에 대한 지출은 향후 수년간 크게 증가할 것으로 예상됩니다.

- 이미 AI 확산의 수혜를 받고 있는 두 기업은 앞으로 더 큰 상승 잠재력을 가지고 있습니다.

인공지능(AI)은 여러 산업에서 판도를 바꾸는 역할을 하고 있습니다. 이 기술은 반복적인 작업을 자동화하고 특정 기능을 대체할 수 있는 능력을 통해 기업, 정부, 조직들이 생산성과 효율성을 높일 수 있도록 돕기 때문입니다.

The potential of AI helps explain why its increasing adoption is expected to give global gross domestic product (GDP) a big boost going forward, adding trillions of dollars to the world's economy.

AI의 잠재력은 왜 이 기술의 확산이 향후 전 세계 국내총생산(GDP)을 크게 끌어올릴 것으로 예상되는지를 설명해줍니다. AI는 앞으로 수조 달러 규모의 경제적 가치를 창출하며 세계 경제에 막대한 기여를 할 것으로 전망됩니다.

Not surprisingly, a lot of money is being spent on AI-related hardware and software to help capture some of this economic potential. Market research firm IDC expects global spending on AI infrastructure to exceed $200 billion by 2028, which would be a nice increase over this year's projected spending of $150 billion.

이러한 잠재력을 실현하기 위해 AI 관련 하드웨어와 소프트웨어에 대한 투자도 빠르게 증가하고 있습니다.

시장조사업체 IDC는 전 세계 AI 인프라 지출이 2028년까지 2,000억 달러를 넘어설 것으로 예상하고 있으며, 이는 올해 예상 지출액인 1,500억 달러보다 크게 늘어나는 수치입니다.

On the other hand, the research firm expects the AI software platforms market to clock an annual growth rate of almost 41% through 2028. That's why now is a good time to take a closer look at the prospects of two companies that are taking advantage of these lucrative end markets and have the potential to deliver healthy long-term gains for their investors.

한편, 해당 시장조사업체는 AI 소프트웨어 플랫폼 시장이 2028년까지 연평균 약 41%의 고성장을 기록할 것으로 예상하고 있습니다.

이러한 이유로 지금이야말로 이처럼 수익성이 높은 최종 시장을 적극적으로 공략하고 있으며, 장기적으로 투자자에게 높은 수익을 안겨줄 잠재력이 있는 두 기업의 전망을 자세히 살펴볼 적기입니다.

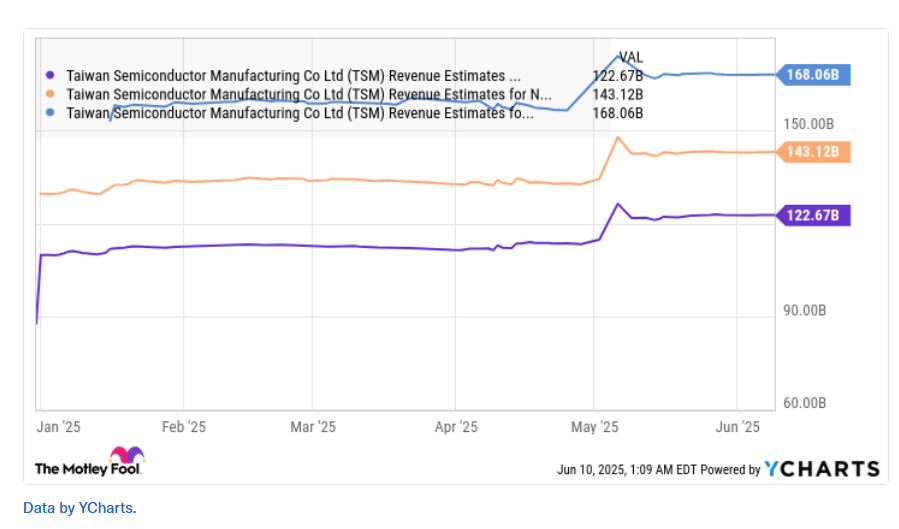

1. Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing (NYSE: TSM) offers a great way for investors to capitalize on the huge investments in AI infrastructure. Popularly known as TSMC, this Taiwan-based company is the largest semiconductor foundry in the world, fabricating semiconductors on a large scale for major chip designers such as Nvidia, Broadcom, AMD, Marvell Technology, and others.

Taiwan Semiconductor Manufacturing(뉴욕증권거래소: TSM)은 AI 인프라에 대한 대규모 투자를 활용할 수 있는 훌륭한 투자처입니다. 흔히 TSMC로 알려진 이 대만 기업은 세계 최대의 반도체 파운드리로, Nvidia, Broadcom, AMD, Marvell Technology 등 주요 반도체 설계업체들을 위해 대규모로 칩을 생산하고 있습니다.

These customers are seeing terrific growth in sales of their AI chips, and that's having a positive impact on TSMC's financial results. For instance, all the customers mentioned above saw remarkable growth in their AI chip revenue in their latest quarters.

이들 고객사는 AI 반도체 판매에서 눈에 띄는 성장을 보이고 있으며, 이는 TSMC의 실적에도 긍정적인 영향을 미치고 있습니다. 예를 들어, 앞서 언급한 모든 고객사들은 최근 분기에서 AI 반도체 매출이 크게 증가했습니다.

Nvidia reported 73% growth in data center revenue for the previous quarter, while Broadcom's AI revenue jumped 46%. A similar story unfolded for Marvell Technology as well, driven by healthy demand for its custom AI processors.

엔비디아(Nvidia)는 지난 분기 데이터센터 부문 매출이 73% 증가했다고 발표했으며, 브로드컴(Broadcom)의 AI 관련 매출도 46% 급증했습니다. 마벨 테크놀로지(Marvell Technology) 역시 맞춤형 AI 프로세서에 대한 수요가 견조하게 유지되면서 비슷한 성장세를 보였습니다.

중요한 점은, 이들 기업 모두 각자의 분야에서 선도적인 위치를 차지하고 있으며, 향후 전망 또한 이들이 현재의 견조한 성장세를 지속할 수 있음을 보여준다는 것입니다.

예를 들어, 브로드컴(Broadcom)은 자사의 칩이 향후 3년간 공략 가능한 시장 규모(SAM, Serviceable Addressable Market)를 무려 600억~900억 달러로 추정하고 있으며, 여기에 현재 협력 중인 신규 고객들로부터 발생할 수 있는 잠재적 매출은 아직 포함되지 않은 수치입니다.

Meanwhile, the data center graphics card market is expected to clock a 30% annual growth rate over the next decade. This explains why TSMC is forecasting its AI accelerator revenue to double this year, followed by a compound annual growth rate (CAGR) in the mid-40% range over the next five years.

한편, 데이터센터용 그래픽카드 시장은 향후 10년간 연평균 30%의 성장률을 기록할 것으로 전망되고 있습니다.

이러한 추세를 반영하듯, TSMC는 올해 AI 가속기 관련 매출이 두 배로 증가할 것으로 예상하고 있으며, 향후 5년 동안에는 연평균 성장률(CAGR)이 40% 중반대에 이를 것으로 내다보고 있습니다.

The impressive growth in the AI chip market is the reason why TSMC's revenue in the first four months of 2025 has increased by 43% from the same period last year.

AI 반도체 시장의 이처럼 눈부신 성장 덕분에 TSMC는 2025년 1월부터 4월까지의 누적 매출이 전년 동기 대비 43% 증가한 것으로 나타났습니다.

That's an improvement over the 30% revenue growth the company delivered in 2024 to $90 billion. The strong start to 2025 is the reason why TSMC's growth is set to accelerate this year, followed by healthy, double-digit growth rates in the next couple of years as well.

이는 TSMC가 2024년에 기록한 30% 매출 성장(총매출 900억 달러)보다 더욱 개선된 수치입니다.

2025년 초반의 강력한 실적 흐름 덕분에, TSMC는 올해 성장 속도가 더욱 빨라질 것으로 예상되며, 향후 몇 년간에도 두 자릿수의 견조한 성장세를 이어갈 것으로 보입니다.

What's worth noting is that TSMC's 67% share of the global foundry market gives the company a solid competitive advantage and puts it in a nice position to make the most of the secular growth opportunity in AI chips. And finally, TSMC's trailing earnings multiple of 24 means that investors are getting a great deal on this AI stock right now, and they should consider grabbing this opportunity with both hands before it flies higher following the 37% gains it has clocked in the past two months.

주목할 점은 TSMC가 전 세계 파운드리 시장의 67%를 차지하고 있다는 사실입니다. 이 압도적인 시장 점유율은 TSMC에 강력한 경쟁 우위를 제공하며, AI 반도체라는 구조적 성장 기회를 최대한 활용할 수 있는 유리한 위치에 있다는 뜻입니다.

또한 현재 TSMC의 주가는 과거 12개월 기준 주가수익비율(PER)이 24배 수준으로, 투자자 입장에서는 이 유망한 AI 종목을 비교적 합리적인 가격에 매수할 수 있는 기회를 제공하고 있습니다. 지난 두 달 동안 주가가 37% 상승했음에도 불구하고, 지금이 이 종목에 투자하기에 적기일 수 있습니다. 더 오르기 전에 이 기회를 놓치지 말고 적극적으로 검토해볼 만합니다.

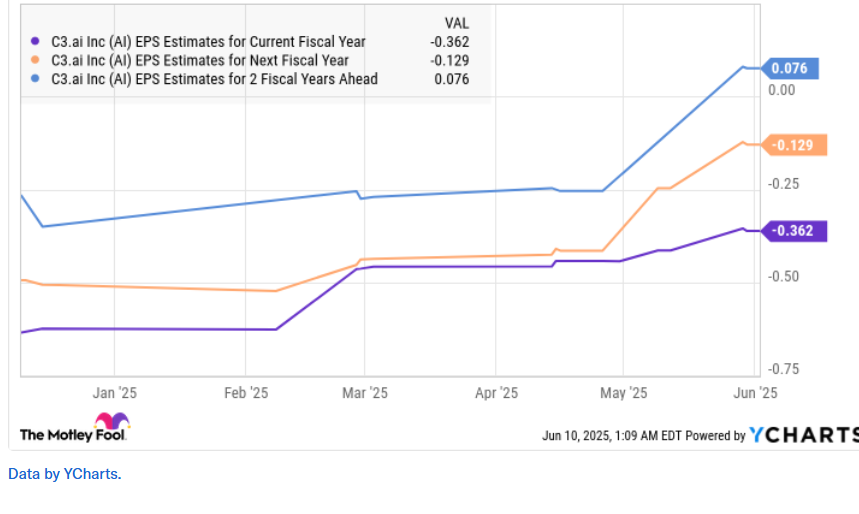

2. C3.ai

The adoption of AI software by businesses and governments is turning out to be a tailwind for C3.ai (NYSE: AI), a pure-play enterprise AI software provider that's witnessing strong customer interest.

기업과 정부 기관의 AI 소프트웨어 도입이 증가하면서, 순수 AI 소프트웨어 전문 기업인 C3.ai(뉴욕증권거래소: AI)에게 강력한 성장 동력이 되고 있습니다. 이 회사는 엔터프라이즈(기업용) AI 소프트웨어 시장에 집중하고 있으며, 현재 고객들의 관심과 수요가 크게 증가하고 있습니다.

C3.ai has been in the news of late for winning contracts from the U.S. Air Force (USAF), which has been deploying its platform for predictive maintenance of aircraft, weapons systems, and ground assets. Specifically, the USAF has raised its contract ceiling for C3.ai's generative AI software to $450 million from an initial $100 million. The good part is that the company has started executing contracts for the USAF under this program.

최근 C3.ai는 미 공군(USAF)으로부터 계약을 수주하며 주목받고 있습니다. 미 공군은 항공기, 무기 시스템, 지상 장비 등의 예측 정비를 위해 C3.ai의 플랫폼을 도입하고 있으며, 특히 생성형 AI 소프트웨어에 대한 계약 한도를 기존 1억 달러에서 4억5천만 달러로 대폭 상향 조정했습니다.

더욱 긍정적인 점은, C3.ai가 이 프로그램에 따라 미 공군과의 계약을 실제로 이행하기 시작했다는 것입니다.

This, however, is one of the many contracts that C3.ai has been winning, apart from getting more business from existing customers. In the recently concluded fiscal year 2025, C3.ai closed 264 agreements with customers, an increase of 38%. This number included 174 initial production deployments, which refers to the pilot projects that the company is currently undertaking.

하지만 이는 C3.ai가 수주한 많은 계약 중 하나에 불과하며, 기존 고객들로부터의 추가 수주도 계속 늘어나고 있습니다. 최근 마무리된 2025 회계연도 동안 C3.ai는 총 264건의 고객 계약을 체결했으며, 이는 전년 대비 38% 증가한 수치입니다.

이 가운데 174건은 초기 생산 배치(initial production deployments)로 분류되며, 이는 현재 회사가 진행 중인 파일럿 프로젝트를 의미합니다.

C3.ai CFO Hitesh Lath remarked on the company's recent earnings conference call:

C3.ai의 최고재무책임자(CFO) 히테시 라스(Hitesh Lath)는 최근 실적 발표 컨퍼런스 콜에서 다음과 같이 언급했습니다:

At the end of the quarter, we had cumulatively signed 346 initial production deployments, of which 263 are still active. This means they are either in their original 3- to 6-month term or extended for some duration, converted to an ongoing subscription contract or are currently being negotiated for conversion to ongoing subscription contracts.

“분기 말 기준으로, 우리는 누적 총 346건의 초기 생산 배치 계약을 체결했으며, 이 중 263건은 여전히 활성 상태입니다. 이는 해당 프로젝트들이 아직 원래의 3~6개월 기간 내에 있거나, 일정 기간 연장되었거나, 정기 구독 계약으로 전환되었거나, 또는 현재 구독 계약으로 전환하기 위한 협상이 진행 중이라는 의미입니다.”

So, there is a good chance that C3.ai's growth rate could keep getting better following the 25% increase in its revenue last fiscal year, which was an improvement of nine percentage points over its fiscal 2024 top-line growth. Management has guided for a 20% increase in revenue for the current fiscal year to $465 million. However, C3.ai could exceed that mark if it can convert its ongoing pilot projects into long-term contracts.

따라서 C3.ai는 지난 회계연도에 기록한 25%의 매출 성장(전년도 대비 9%포인트 상승)을 바탕으로, 앞으로 성장률이 더욱 가속화될 가능성이 높습니다.

경영진은 현재 회계연도 매출이 4억 6,500만 달러로 전년 대비 약 20% 증가할 것으로 가이던스를 제시했습니다. 그러나 현재 진행 중인 파일럿 프로젝트들이 장기 계약으로 전환된다면, 이 목표치를 초과 달성할 가능성도 충분합니다.

After all, the company's relationship with key federal agencies and big names such as ExxonMobil, U.S. Steel, Bristol Myers Squibb, and many others establishes it as a credible player in the AI software market, and that could help it attract more customers into its fold. This is probably why analysts expect C3.ai's growth rate to pick up in the future and project that it will become profitable in the next couple of fiscal years.

결국 C3.ai는 엑손모빌(ExxonMobil), US 스틸(U.S. Steel), 브리스톨 마이어스 스퀴브(Bristol Myers Squibb) 등 주요 대기업뿐만 아니라 미국 연방 정부 기관들과도 협력 관계를 맺고 있어, AI 소프트웨어 시장에서 신뢰할 수 있는 기업으로 자리매김하고 있습니다.

이러한 고객 기반은 향후 더 많은 신규 고객을 유치하는 데에도 긍정적인 영향을 줄 수 있으며, 이는 아마도 애널리스트들이 C3.ai의 향후 성장 속도가 다시 빨라질 것으로 예상하고, 향후 몇 회계연도 내에 흑자 전환할 것으로 전망하는 이유일 것입니다.

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| 메모리 반도체는 AI 워크로드의 핵심 요소다(2025.06.20) (0) | 2025.06.21 |

|---|---|

| 마벨 테크놀로지, AI용 커스텀 칩 시장의 기회 규모를 2028년까지 550억 달러로 제시(2025.06.18) (2) | 2025.06.19 |

| 시장 전망 상향에 힘입어 AI 반도체 주가 상승(2025.06.17) (0) | 2025.06.17 |

| SK하이닉스,1분기 D램 영업이익 중 HBM이 절반 이상(2025.06.13) (0) | 2025.06.13 |

| 'HBM의 아버지' 김정호 카이스트 교수, 차세대 HBM 로드맵 발표(2025.06.11) (0) | 2025.06.11 |