2022.04.04

이미 몇몇 전기차는 차 한대당 메모리 반도체 장착 비용이 750달러에 달해서, 일반 가솔린 차의 15배에 달한다고

마이크론 사장은 말했다. 이는 향후 몇년간 회사 성장에 상당히 강력한 뒷받침이 될것임이 틀림없다.

2021년 글로벌 전기차 판매량은 660만대이다.

Buy Micron Stock. The Chip Stock Deserves Better. | Barron's (barrons.com)

All of that is true, and beside the point. Micron last week reported results for its fiscal second quarter that comfortably topped its own outlook for revenue, profits, and margins. The company also offered fiscal third quarter guidance that blew past Wall Street expectations. For the May quarter, Micron is projecting revenue of $8.7 billion, up 17%, and well ahead of the old analyst consensus of $8.1 billion.

마이크론은 지난주 자사의 전망을 웃도는 2분기 매출과 이익 실적을 발표했다.

또 회사는 시장 전망치를 상회하는 3분기 실적 예상치를 발표했다.

5월말 끝나는 분기 매출을 시장 컨센서스 81억달러를 상회하는 87억달러로 예상했다.

In an interview this past week, Sumit Sadana, Micron’s chief business officer and acting chief financial officer, said demand from the PC industry remains strong. While Micron sees flat unit sales for PCs in calendar 2022, Sadana noted that softening consumer demand is offset by growth in enterprise PCs, which tend to have more memory than consumer laptops.

마이크론 사장은 2022년 PC 판매대수는 전년과 비슷할것이고, 개인용 PC판매는 감소할 것이나,

더 많은 메모리를 장착하는 기업용 PC 판매 증가가 이를 상쇄할 것으로 예상했다.

Sadana said Micron’s largest opportunity comes from the automotive sector. The shift to electric vehicles—and down the road, cars with at least some level of autonomy—will make memory chips a much higher portion of the bill of materials in future cars.

마이크론은 자동차 시장에서 가장 큰 기회가 올것으로 분석했다.

전기차로의 이동은 , 길에서 달리는 전기차는 적어도 어느 정도의 자율주행 기능을 가지는데,

미래 자동차에 내장되는 메모리 비용 비중이 점점더 커질 것이다.

Sadana says that some EVs already require as much as $750 of memory chips per car—about 15 times the memory used in a conventional gas-powered vehicle. The shift to EVs, he says, should be “an incredibly powerful tailwind for years to come.”

이미 몇몇 전기차는 차 한대당 메모리 반도체 장착 비용이 750달러에 달해서, 일반 가솔린 차의 15배에 달한다고

마이크론 사장은 말했다. 이는 향후 몇년간 회사 성장에 상당히 강력한 뒷받침이 될것임이 틀림없다.

He’s not the only one who thinks so. In a report released on Friday, McKinsey projected that the overall semiconductor industry would reach $1 trillion in sales in 2030, up from $600 billion in 2021.

McKinsey projects the automotive sector will be 13% to 15% of overall chip sales by 2030, up from 8% in 2021.

이는 마이크론 사장만의 생각이 아니다.

지난 금요일(4월1일) 발표된 맥킨지 보고서에서 반도체 매출이 2021년 6천억달러에서 2030년 1조달러로 증가할 것이고,

자동차부문 반도체 매출 비중은 전체 반도체 매출 2021년 8%에서 2030년에는 13%~15%로 증가할 것이라 하였다.

Ondrej Burkacky, who leads McKinsey’s global semiconductor practice, says the expected spike in auto industry demand assumes no sudden boost in production—he’s modeling unit sales will remain at about 100 million a year. And he doesn’t expect the arrival of fully autonomous anytime soon. For that, he says, you’ll have to wait until 2035, 2040, or maybe longer.

매킨지에서 자동차부문을 담당하는 버카키는 자동차 산업 수요의 예상되는 급증은 생산량이 갑자기 증가하지

않는다는 것을 전제로 하고 있다고 말했습니다. 그

의 모델링 단위 판매는 연간 약 1억대로 유지될 것입니다. 그리고 그는 완전한 자율주행 시대가 곧 도래할 것이라고

기대하지 않습니다. 그는 이를 위해서는 2035년, 2040년 또는 그 이상을 기다려야 한다고 말합니다.

But Burkacky does see a rapid shift to electric vehicles—he expects EVs to be 30% to 40% of total production by 2030. And he foresees growing adoption of memory-intensive driver-assistance technologies, like parking assist and lane departure notifications. He also expects to see increased use of sophisticated digital cockpit displays. It all adds up, Burkacky thinks, to a doubling of dollar value in chips per car by the end of the decade.

그러나 Burkacky는 전기 자동차로의 급속한 전환을 보고 있습니다. 그는 2030년까지 전기 자동차가 전체 생산량의 30~40%를 차지할 것으로 예상합니다. 그리고 그는 주차 지원 및 차선 이탈 알림과 같은 메모리 집약적인 운전자 지원 기술의 채택이 증가할 것으로 예상합니다.

그는 또한 정교한 디지털 운전석 디스플레이의 사용이 증가할 것으로 기대하고 있습니다.

Burkacky는 이 모든 것이 10년훙에는 자동차당 칩 비용이 두 배로 증가할 것이라고 생각합니다.

A good portion of that is going to come in the form of increased memory. Sadana says Micron is already seeing some cars with as much as a terabyte of NAND, the same amount of storage in Apple ’s most powerful iPhone.

So here’s a company with strong growth prospects, a huge emerging market opportunity, and leading technology, and what does it cost investors? Not very much. Micron shares trade for about two times estimated fiscal 2023 revenue, and about 6.5 times expected fiscal 2023 profits.

그 중 좋은 부분은 메모리 증가의 형태로 올 것입니다. Sadana는 Micron이 이미 Apple의 가장 강력한 iPhone에 있는

동일한 용량인 테라바이트(천 기가바이트)의 NAND를 탑재한 일부 차량을 보고 있다고 말했습니다.

강력한 성장 전망, 거대한 신흥 시장 기회 및 선도적인 기술을 갖춘 회사가 있으며 투자자에게 비용은 얼마입니까?

별로들지 않습니다.

마이크론 주식은 2023 회계연도 예상 매출의 약 2배, 예상 이익의 약 6.5배에 거래되고 있습니다.

Compare that to Qualcomm (QCOM) at 12 times forward profits, Intel (INTC) at 13 times, Advanced Micro Devices (AMD) at 23 times, and Nvidia (NVDA) at 40 times. Micron’s revenue next year will be about even with Nvidia’s, but it has about an eighth of the market value.

Meanwhile, Micron shares are down 16% year to date. For investors, it’s a memorable buying opportunity.

마이크론은 올해들어 16% 하락하였다. 이것은 투자자에게 기억할만한 매수 기회이다.

댓글중 재미있는 글을 하나 퍼왔어요

I've been operating electromagnetic simulation software for about three decades, and every year I get several problems to simulate that require more memory than my computer has. Working around the RAM shortage takes many times the amount of hours. Employers never want to spend the money for the RAM, but wind up paying about 10 times the cost in hours. By the time they do upgrade, the newer software requires several times more RAM, so the shortage continues. It's been that way my entire career.

So Micron will always have huge demand, its like the oil of the electronics industry.

나는 전자기 시뮬레이션 소프트웨어를 사용하는 일을 30년간 해왔다.

매년 소프트웨어 작동시키는데 컴퓨터 메모리가 부족하였다.

메모리가 부족한 상태에서 작업을하면 시간이 몇배나 더 걸렸다.

사장은 메모리 추가에 더많은 돈을 싸용하기를 거부했고, 결과는 시간이 10배 더 걸리게 되었다.

컴퓨터를 업그레이드할 때 즈음에는 새로운 소프트웨어가 더 많은 메모리를 필요로 하게된다.

그래서 메모리 부족은 계속되고, 내 캐리어 내내 그랬다.

마이크론은 항상 엄청난 수요를 가질것이고, 전자 산업의 석유와 같은 존재이다.

----------------------------------

2022.04.04

Micron Stock: Undervalued With Massive Potential - Here's Why (NASDAQ:MU) | Seeking Alpha

-------------------------------------

How Micron Makes Money: Memory Solutions and Storage Products (investopedia.com)

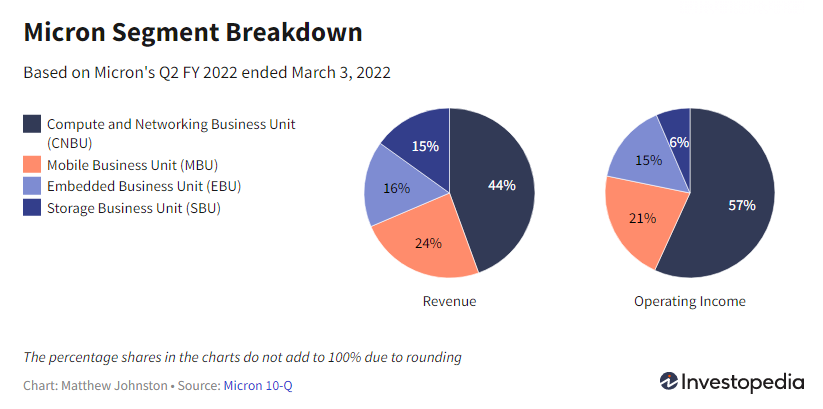

Micron's Business Segments

Micron operates through four different reportable segments: Compute and Networking Business Unit (CNBU), Mobile Business Unit (MBU), Storage Business Unit (SBU), and Embedded Business Unit (EBU).6 The company provides a breakdown of revenue and operating income for each of these segments.7

It also reports an additional miscellaneous category to cover other revenue sources. This "All Other" unit contributes a negligible amount to total revenue and operating income.7 Results from this "All Other" unit are thus excluded from the revenue and operating income percentage share calculations below and in the pie charts above.

Compute and Networking Business Unit (CNBU)

Micron's CNBU segment includes memory products that are sold into markets for cloud server, enterprise, graphics, networking, and other clients.6 CNBU generated $3.5 billion in revenue in Q2 FY 2022, up 31.8% compared to the year-ago quarter. The segment accounted for the majority of the company's revenue during the quarter, with a revenue share of more than 44% across all four segments. Operating income rose 120.3% YOY to $1.6 billion, comprising nearly 57% of the total across all segments.7

Mobile Business Unit (MBU)

The MBU segment includes memory and storage products sold into the mobile-device and smartphone markets.6 MBU's revenue grew 3.5% YOY to $1.9 billion, accounting for about 24% of the company's revenue across all segments in Q2 FY 2022. The segment generated $588 million in operating income, up 26.7% compared to the year-ago quarter. It accounted for over 21% of total operating income across all four segments.7

Storage Business Unit (SBU)

Micron's SBU segment includes solid-state drives as well as component-level solutions sold to cloud, client, enterprise, and other storage markets.6 SBU generated $1.2 billion in revenue in Q2 FY 2022, up 37.7% compared to the year-ago quarter. The segmented accounted for 15% of total revenue across all four segments. It posted $178 million in operating income, a significant improvement from the $59 million operating loss reported in the year-ago quarter. The segmented accounted for more than 6% of total operating income across all segments.7

Embedded Business Unit (EBU)

The EBU segment covers memory and storage products used in a variety of industries, including automotive, consumer markets, and industrial applications.6 EBU's revenue in Q2 FY 2022 rose 36.6% YOY to $1.3 billion, comprising over 16% of total revenue across all segments. The segment generated $421 million in operating income, up 198.6% compared to the year-ago quarter. It accounted for more than 15% of total operating income across all four segments.

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| AI 기술의 다양한 응용 분야_AI 반도체의 현황과 미래전망 (0) | 2022.04.05 |

|---|---|

| SK하이닉스, 솔리다임과 첫 ‘합작 제품’ 공개, “낸드 사업 양사 시너지 본격화” (0) | 2022.04.05 |

| 마이크론 2022년2분기 실적발표(2022.03.29) (0) | 2022.03.30 |

| 서버용 부품 부족은 2022년 내내 지속될 듯(2022.03.23) (0) | 2022.03.23 |

| 마이크론 목표가 155달러(2022.03.22) (0) | 2022.03.23 |