Memory Industry Revenue Expected to Reach Record High in 2025 Due to Increasing Average Prices and the Rise of HBM and QLC, Says TrendForce

메모리 산업, HBM 및 QLC의 부상과 평균 가격 상승으로 2025년에 사상 최고 수익 예상 - 트렌드포스

TrendForce’s latest report on the memory industry reveals that DRAM and NAND Flash revenues are expected to see significant increases of 75% and 77%, respectively, in 2024, driven by increased bit demand, an improved supply-demand structure, and the rise of high-value products like HBM.

트렌드포스의 메모리 산업에 대한 최신 보고서에 따르면, DRAM과 NAND 플래시 매출이 2024년에 각각 75%와 77% 증가할 것으로 예상됩니다. 이는 비트 수요 증가, 개선된 수급 구조, HBM과 같은 고부가가치 제품의 부상이 주요 요인으로 작용할 것입니다.

Furthermore, industry revenues are projected to continue growing in 2025, with DRAM expected to increase by 51% and NAND Flash by 29%, reaching record highs. This growth is anticipated to revive capital expenditures and boost demand for upstream raw materials, although it will also increase cost pressure for memory buyers.

더욱이, 산업 매출은 2025년에도 계속 성장할 것으로 전망되며, DRAM은 51%, NAND 플래시는 29% 증가하여 사상 최고치를 기록할 것으로 보입니다. 이러한 성장은 자본 지출을 회복시키고 업스트림 원자재에 대한 수요를 증대시킬 것으로 예상되지만, 동시에 메모리 구매자들에게 비용 압박을 가중시킬 것입니다.

Rise of HBM boosts DRAM revenue

HBM의 부상이 DRAM 매출을 증대시킨다

TrendForce estimates that benefiting from an increase in average DRAM prices by 53% in 2024 and 35% in 2025, DRAM revenue will reach US$90.7 billion in 2024—a 75% YoY increase—and $136.5 billion in 2025—a 51% YoY increase.

트렌드포스에 따르면, 2024년 DRAM 평균 가격이 53%, 2025년에는 35% 상승함에 따라 DRAM 매출은 2024년에 907억 달러에 도달하여 전년 대비 75% 증가하고, 2025년에는 1365억 달러에 도달하여 전년 대비 51% 증가할 것으로 예상됩니다.

TrendForce identifies four key factors driving the revenue growth of DRAM: the rise of HBM, the generational evolution of general DRAM products, restrained capital expenditures by manufacturers limiting supply, and the recovery in server demand.

Compared to general DRAM, HBM not only boosts bit demand but also raises the industry’s average price. HBM is expected to contribute 5% of DRAM bit shipments and 20% of revenue in 2024.

트렌드포스는 DRAM 매출 증가를 이끄는 네 가지 주요 요인을 다음과 같이 식별했습니다: HBM의 부상, 일반 DRAM 제품의 세대 진화, 제조업체의 자본 지출 억제로 인한 공급 제한, 서버 수요의 회복.

일반 DRAM과 비교할 때, HBM은 비트 수요를 증가시킬 뿐만 아니라 업계의 평균 가격도 상승시킵니다. HBM은 2024년 DRAM 비트 출하량의 5%와 매출의 20%를 차지할 것으로 예상됩니다.

Additionally, the penetration of high-value products like DDR5 and LPDDR5/5X will help raise the industry’s average price. TrendForce estimates that DDR5 will account for 40% of server DRAM bit shipments in 2024, increasing to 60–65% in 2025. LPDDR5/5X is expected to contribute 50% and 60% of mobile DRAM bit shipments in 2024 and 2025, respectively.

또한, DDR5와 LPDDR5/5X와 같은 고부가가치 제품의 보급은 업계 평균 가격을 상승시키는 데 기여할 것입니다. 트렌드포스는 2024년 서버 DRAM 비트 출하량의 40%가 DDR5가 차지할 것이며, 2025년에는 60-65%로 증가할 것으로 예상합니다. LPDDR5/5X는 2024년과 2025년에 각각 모바일 DRAM 비트 출하량의 50%와 60%를 차지할 것으로 예상됩니다.

아래 그래프는 2017년부터 2025년까지의 디램 산업의 매출과 매출 전망치.

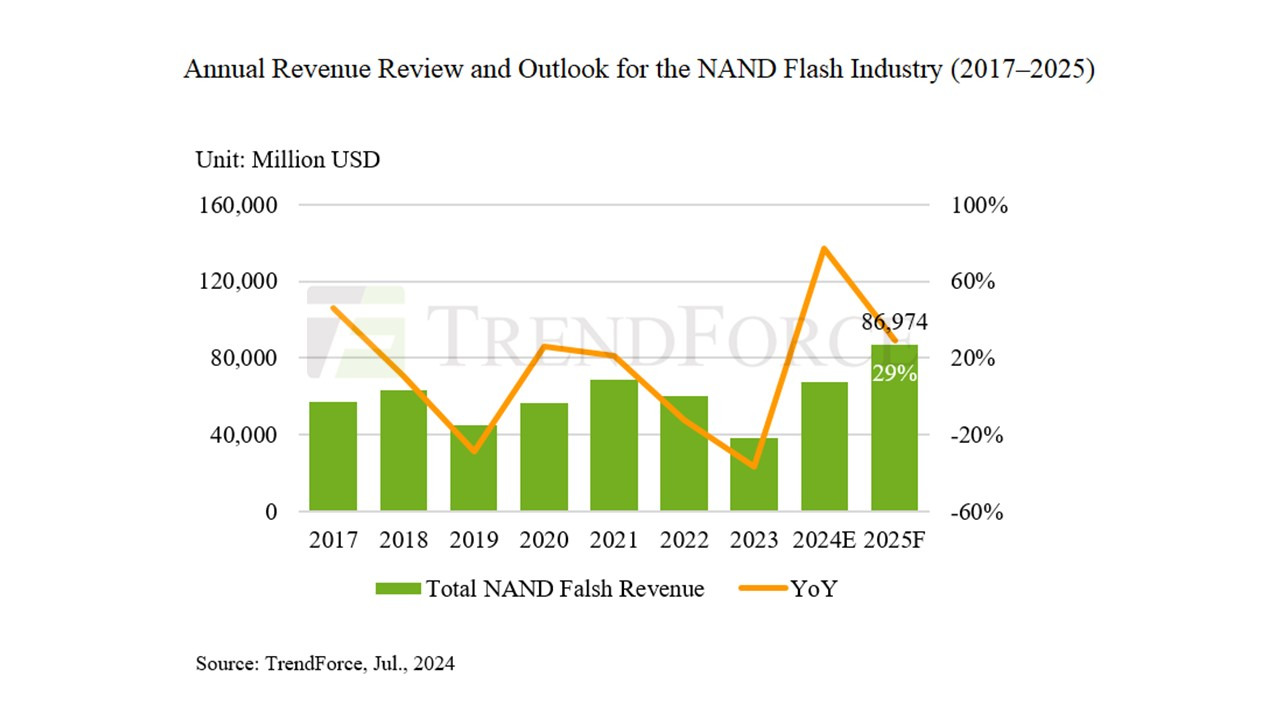

High-capacity QLC enterprise SSDs and UFS to drive record NAND Flash revenue in 2025

대용량 QLC 엔터프라이즈 SSD와 UFS, 2025년 NAND 플래시 매출 기록 경신 주도

TrendForce projects that NAND Flash revenue will reach $67.4 billion in 2024, a 77% YoY increase. In 2025, driven by the rise of high-capacity QLC enterprise SSDs, the adoption of QLC UFS in smartphones, restrained capital expenditures by manufacturers limiting supply, and the recovery in server demand, NAND Flash revenue is expected to reach $87.0 billion—a 29% YoY increase. North American CSPs have already begun extensively adopting QLC enterprise SSDs in inference AI servers, especially those with high-capacity specifications.

트렌드포스는 2024년 NAND 플래시 매출이 674억 달러에 도달하여 전년 대비 77% 증가할 것으로 예상합니다. 2025년에는 대용량 QLC 엔터프라이즈 SSD의 부상, 스마트폰에서 QLC UFS 채택, 제조업체의 자본 지출 억제로 인한 공급 제한, 서버 수요 회복에 힘입어 NAND 플래시 매출이 870억 달러에 도달하여 전년 대비 29% 증가할 것으로 예상됩니다. 북미 CSP(클라우드 서비스 제공업체)들은 이미 고용량 사양을 가진 추론 AI 서버에서 QLC 엔터프라이즈 SSD를 광범위하게 채택하기 시작했습니다.

TrendForce estimates that QLC will contribute 20% of NAND Flash bit shipments in 2024, with this share expected to increase in 2025. In smartphone applications, QLC is expected to gradually penetrate the UFS market, with some Chinese smartphone manufacturers planning to adopt QLC UFS solutions starting in Q4 2024. Apple is anticipated to begin incorporating QLC into iPhones by 2026.

트렌드포스는 QLC가 2024년 NAND 플래시 비트 출하량의 20%를 차지할 것으로 추정하며, 이 비율은 2025년에 증가할 것으로 예상됩니다. 스마트폰 애플리케이션에서는 QLC가 점차 UFS 시장에 침투할 것으로 예상되며, 일부 중국 스마트폰 제조업체들은 2024년 4분기부터 QLC UFS 솔루션을 채택할 계획입니다. 애플은 2026년까지 iPhone에 QLC를 통합할 것으로 예상됩니다.

Rising DRAM and NAND Flash revenues set to impact industry ecosystem

증가하는 DRAM 및 NAND 플래시 매출이 산업 생태계에 미치는 영향

TrendForce reports that with record-breaking revenues in the memory industry, manufacturers will have sufficient cash flow to accelerate investments. Capital expenditures in DRAM and NAND Flash industries are expected to increase by 25% and 10%, respectively, in 2025, with the potential for further upward revisions.

트렌드포스는 메모리 산업의 기록적인 매출 덕분에 제조업체들이 충분한 현금 흐름을 확보하여 투자를 가속화할 수 있을 것이라고 보고합니다. DRAM과 NAND 플래시 산업의 자본 지출은 2025년에 각각 25%와 10% 증가할 것으로 예상되며, 추가 상향 조정의 가능성도 있습니다.

The expansion of memory production will boost demand for upstream raw materials such as silicon wafers and chemicals. Conversely, rising memory prices will increase the cost of electronic products. ODM/OEM companies will find it challenging to fully pass on these costs to retail prices, leading to compressed profit margins. This cost increase may also dampen end-user sales, potentially causing a decline in demand.

메모리 생산의 확장은 실리콘 웨이퍼 및 화학물질과 같은 상류 원자재에 대한 수요를 증대시킬 것입니다. 반면, 메모리 가격 상승은 전자 제품의 비용을 증가시킬 것입니다. ODM/OEM 업체들은 이러한 비용을 소매 가격에 완전히 반영하기 어려워 이윤 마진이 축소될 것입니다. 이 비용 증가는 또한 최종 사용자 판매를 저하시켜 수요 감소를 초래할 수 있습니다.

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| AMD가 Zen 5에 대한 더 많은 정보를 공개 (0) | 2024.07.26 |

|---|---|

| SK하이닉스 '24년 2분기 실적(2024.07.25) (0) | 2024.07.25 |

| '24년6월 수출입 동향 (0) | 2024.07.08 |

| 삼성전자는 세계 최초로 CXL 인프라를 구축(2024.06.28) (0) | 2024.06.28 |

| 마이크론24'3분기 실적(2024.06.27) (0) | 2024.06.27 |