2022.05.26

Nvidia falls short on guidance, stock down 9% after hours (yahoo.com)

엔비디아는 장마감후 실적을 발표.

1분기 실적은 시장 예상치를 상회했으나, 2분기 실적 전망치가 시장 컨센서스를 하회함으로

시간외 거래에서 6% 하락.

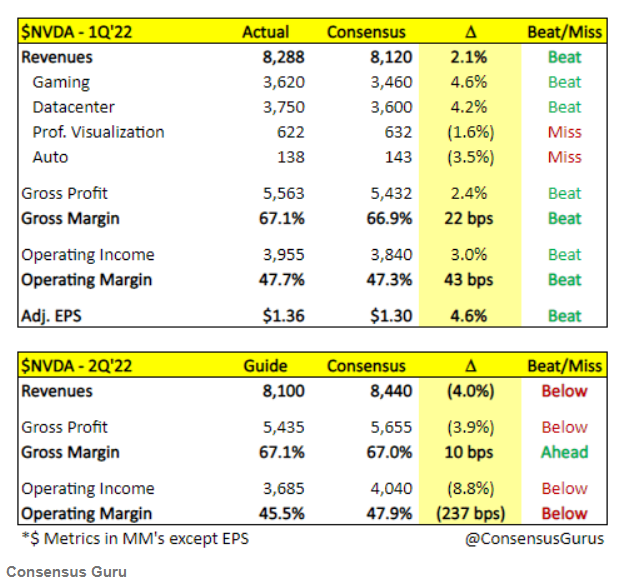

1분기 매출 82.9억달러 및 주당 순이익 1.36달러는 애널리스트들의 예상을 웃돌았지만 2분기 예상치는 미치지 못했습니다.

매출은 전년 동기대비 46%, 전기대비 8% 증가.

2분기 매출 예상치는 81억달러로 시장 전망치 84.4억달러를 하회.

NVIDIA Announces Financial Results for First Quarter Fiscal 2023 | Seeking Alpha

Nvidia (NVDA) reported its Q1 earnings after the bell Wednesday, beating analysts' expectations on revenue and earnings per share, but falling short on Q2 estimates.

Nvidia(NVDA)는 수요일 장마감 후에 1분기 실적을 발표하였다.

매출 82.9억달러 및 주당 순이익 1.36달러는 애널리스트들의 예상을 웃돌았지만 2분기 예상치는 미치지 못했습니다.

2분기 매출 예상치는 81억달러로 시장 전망치 84.4억달러를 하회.

Nvidia는 우크라이나 전쟁과 중국의 COVID 봉쇄의 영향으로 2분기에 약 5억 달러의 매출이 감소할 것이라고 말했습니다.

Here are the most important numbers from the report compared to what Wall Street was expecting from the graphics card giant in the quarter.

다음은 엔비디아의 실제 실적과 전망치를 비교한 수치입니다.

- Revenue: $8.29 billion versus $8.10 billion expected매출: 82억 9000만 달러 대 예상 81억 달러

- Adjusted EPS: $1.36 versus $1.29 expected 조정 EPS: $1.36 대 예상 $1.29

- Net income totalled $1.6 billion (-15% y/y; -46% q/q)

- 순이익은 16억달러로 전년 동기대비 15% 감소, 전분기대비 46% 감소.

- Data Center: $3.75 billion versus $3.63 billion expected

- 데이터 센터: 37억 5000만 달러 대 예상 36억 3000만 달러

- 데이터센터 매출은 전년 동기대비 83%, 전분기대비 15% 증가.

- 전체 매출의 45% 차지.

- Gaming: $3.62 billion versus $3.53 billion expected

- 게이밍: 36억 2000만 달러 대 예상 35억 3000만 달러

- 게이밍부문 매출은 전년 동기대비 31%, 전분기대비 6% 증가.

- 전체 매출의 44% 차지.

Nvidia, however, missed on its Q2 revenue expectations. The company says it will see $8.1 billion in the upcoming quarter, while Wall Street was expecting $8.44 billion. Nvidia says it will miss out on some $500 million in revenue in the quarter due to the war in Ukraine and the impact of COV ID lockdowns in China.

Shares of Nvidia were down more than 9%.

그러나 Nvidia는 2분기 시장의 매출 기대치를 충족하지 못했습니다.

회사는 다가오는 분기에 81억 달러의 매출을 올릴 것이라고 밝혔고 월스트리트는 84억 4천만 달러를 예상했습니다.

Nvidia는 우크라이나 전쟁과 중국의 COVID 봉쇄의 영향으로 분기에 약 5억 달러의 매출이 감소할 것이라고 말했습니다.

Nvidia의 주가는 시간외에서 9% 이상 하락했습니다.

Nvidia’s earnings come as tech stocks have been especially pounded amid a broader market selloff. Nvidia shares are off more than 28% over the last three months, while shares of rival AMD (AMD) are off more than 20%.

Nvidia의 수익은 기술주가 특히 광범위한 시장 매도세 속에서 두드려지면서 나온 것입니다.

Nvidia 주가는 지난 3개월 동안 28% 이상 하락한 반면 경쟁사 AMD(AMD)의 주가는 20% 이상 하락했습니다.

Shares of Qualcomm (QCOM) have also suffered, falling 22%. Intel (INTC), meanwhile, has managed to stay roughly in line with the S&P 500, with shares dropping more than 9% compared to the index’s 7% decline.

Qualcomm(QCOM)의 주가도 22% 하락했습니다. 한편 인텔(INTC)은 S&P 500 지수의 7% 하락에 비해

주가가 9% 이상 하락하면서 대략 S&P 500과 거의 비슷한 수준을 유지했습니다.

Crucially for Nvidia, and gamers, graphics cards are finally returning to store shelves after months of crushing supply chain disruptions. That’s not to say the chip shortage is over, not by a long shot.

Nvidia와 게이머에게 결정적으로 그래픽 카드는 공급망 혼란을 가중시킨 몇 개월 후 마침내 매장 선반으로 돌아왔습니다. 그렇다고 칩 부족이 끝났다는 말은 아닙니다.

Intel CEO Pat Gelsinger predicts that the shortage will continue into 2024, which means we’re still far from returning to pre-pandemic availability for many semiconductors.

Intel CEO Pat Gelsinger는 칩부족이 2024년까지 계속될 것이라고 예측합니다.

That said, Nvidia’s cards, along with AMD’s, are dropping in price thanks to the crash in cryptocurrency prices.

A decrease in the price of crypto usually coincides with a drop in card prices as miners turn their attention away from buying up available supplies to mine coins.

즉, AMD와 함께 Nvidia의 카드는 암호화폐 가격 폭락으로 가격이 떨어지고 있습니다.

암호화폐 가격의 하락은 일반적으로 코인 채굴자가 코인을 채굴하기 위해 카드를 구매하려는

관심이 적어지기 때문에 카드 가격 하락과 일치합니다.

Nvidia is also expected to unveil its latest graphics card lineup in the coming months. Dubbed the RTX 4000-series, the cards should provide a welcome performance boost over the company’s current RTX 3000-series line, not to mention boost Nvidia’s bottom line.

RTX 4000 시리즈라고 불리는 이 카드는 Nvidia의 수익 증대는 말할 것도 없고 회사의 현재 RTX 3000 시리즈 라인보다 뛰어난 성능 향상을 제공할 것입니다.

--------------------

Nvidia Stock: Gaming Normalizes, But Datacenter Remains Solid (NASDAQ:NVDA) | Seeking Alpha

-----------------------------------

2022.05.27

Nvidia Q1 2023 Review: Pioneering Innovation With Innovation (NASDAQ:NVDA) | Seeking Alpha

Nvidia reported first quarter revenues of $8.3 billion (+46% y/y; +8% q/q), beating consensus estimate of $8.09 billion (+43% y/y; +6% q/q) and its previous guidance of $8.1 billion (+43% y/y; +6% q/q).

Gaming segment represented 44% of consolidated sales, with growth of 31% from the same period in the prior year (+6% q/q) to a record-setting $3.6 billion.

Data center sales also maintained strong double-digit year-on-year growth of 83% (+15% q/q) to $3.75 billion in the fiscal first quarter, and now drive 45% of consolidated revenues. Meanwhile, automotive's performance remained soft in comparison as expected, largely due to continued car production challenges observed across OEMs in the first quarter due to supply chain bottlenecks that have been further exacerbated by recent COVID-related lockdowns in China.

Despite rising input costs, Nvidia also posted a fiscal first quarter earnings beat at $1.36 per share, compared with consensus estimate of $1.29 per share. Net income totalled $1.6 billion (-15% y/y; -46% q/q), thanks to robust gross margins of close to 66% (+140 bps y/y; +10 bps q/q) and free cash flow margins of 16%.

For the fiscal second quarter, Nvidia is guiding revenues of $8.1 billion (+24% y/y; -2% q/q), which is slightly down from consensus estimates of $8.5 billion (+31% y/y; +3% q/q) due to an estimated $500 million negative impact from the ongoing Russia-Ukraine war and protracted COVID-related lockdowns in China.

Specifically, data center revenues will continue to benefit from strong cloud computing uptake while gaming revenues will see some normalization to previously tight inventory levels, with sequential revenue declines estimated "in the teens".

Gross margins will also see some slight decline to 65.1%, as management continues to press forward with cost-cutting measures that include a "slowdown to its hiring pace" to counter near-term macroeconomic headwinds.

-------------------------

엔비디아 컨콜

NVIDIA Corporation (NASDAQ:NVDA) Q1 2023 Earnings Conference Call May 25, 2022 5:00 PM ET

Company Participants 회사 참가자

Simona Jankowski - Vice President, Investor Relations 투자자 관계 담당 부사장

Colette Kress - Executive Vice President & Chief Financial Officer 부사장 겸 최고재무책임자(CFO)

Jensen Huang - President & Chief Executive Officer 사장 겸 CEO

Conference Call Participants회의 통화 참가자

C.J. Muse - Evercore ISI 에버코어 ISI

Matt Ramsay - Cowen

Stacy Rasgon - Bernstein Research

Mark Lipacis - Jefferies

Vivek Arya - BofA Securities

Tim Arcuri - UBS

Ambrish Srivastava - BMO

Harlan Sur - JPMorgan

Chris Caso - Raymond James

Aaron Rakers - Wells Fargo

Operator

Good afternoon. My name is David, and I'll be your conference operator today. At this time, I'd like to welcome everyone to NVIDIA's first quarter earnings call. Today's conference is being recorded. All lines have been placed on mute to prevent any background noise. After the speaker’s remarks, there will be question-and-answer session. [Operator Instructions]

Thank you. Simona Jankowski, you may begin your conference.

안녕하세요. 제 이름은 David이고 오늘 회의 진행 맡겠습니다. 현재 NVIDIA의 1분기 실적 발표에 참석하신 모든 분들을 환영합니다. 오늘 회의가 녹화 중입니다. 배경 소음을 방지하기 위해 모든 라인을 음소거 상태로 설정했습니다. 연사 발언 후에는 질의응답 시간이 이어진다. [진행자 지침]

Simona Jankowski

Thank you. Good afternoon, everyone, and welcome to NVIDIA's conference call for the First Quarter of Fiscal 2023. With me today from NVIDIA are Jensen Huang, President and Chief Executive Officer; and Colette Kress, Executive Vice President and Chief Financial Officer.

오늘 NVIDIA의 사장 겸 CEO인 Jensen Huang과 Colette Kress,수석 부사장 겸 최고 재무 책임자가

저와 함께 합니다.

I'd like to remind you that, our call is being webcast live on NVIDIA's Investor Relations website. The webcast will be available for replay until the conference call to discuss our financial results for the second quarter of fiscal 2023. The content of today's call is NVIDIA's property. It can't be reproduced or transcribed without our prior written consent.

During this call, we may make forward-looking statements based on current expectations. These are subject to a number of significant risks and uncertainties and our actual results may differ materially.

For a discussion of factors that could affect our future financial results and business, please refer to the disclosure in today's earnings release, our most recent Forms 10-K and 10-Q and the reports that we may file on Form 8-K with the Securities and Exchange Commission.

All our statements are made as of today, May 25, 2022, based on information currently available to us. Except as required by law, we assume no obligation to update any such statements.

During this call, we will discuss non-GAAP financial measures. You can find a reconciliation of these non-GAAP financial measures to GAAP financial measures in our CFO commentary, which is posted on our website.

With that, let me turn the call over to Colette.

Colette Kress

Thanks, Simona. We delivered a strong quarter driven by record revenue in both Data Center and Gaming with strong fundamentals and execution against a challenging macro backdrop.

우리는 강력한 펀더멘털과 도전적인 거시적 배경에 대한 실행으로 데이터 센터와 게이밍부문 모두에서

기록적인 매출을 창출하는 강력한 분기를 제공했습니다.

Total revenue of $8.3 billion was a record, up 8% sequentially and up 46% year-on-year.

Data Center has become our largest market platform, and we see continued strong momentum going forward.

총 매출은 83억 달러로 전분기 대비 8%, 전년 대비 46% 증가한 기록을 세웠다.

데이터 센터는 우리의 가장 큰 시장 플랫폼이 되었으며 앞으로도 계속 강한 모멘텀을 기대하고 있습니다.

Starting with Gaming. Revenue of $3.6 billion rose 6% sequentially and 31% year-on-year, powered by the GeForce RTX 30 Series product cycle. Since launching in the fall of 2020, the RTX 30 Series has been our best Gaming product cycle ever.

The gaming industry has grown tremendously with 100 million new PC gamers added in the past two years according to Newzoo.

And NVIDIA RTX has set new standard for the industry with demand from both first-time GPU buyers as well as those upgrading their PCs to experience the 250-plus RTX-optimized games and apps, double from last year.

게이밍부문부터 시작합니다.

게이밍부문 매출은 36억달러로 GeForce RTX 30 시리즈 제품에 힘입어 전분기대비 6%, 전년 대비 31% 증가했습니다.

2020년 가을 출시 이후 RTX 30 시리즈는 최고의 게임 제품 주기였습니다.

Newzoo에 따르면 게임 산업은 지난 2년 동안 1억 명의 새로운 PC 게이머가 추가되면서 엄청나게 성장했습니다.

그리고 NVIDIA RTX는 GPU를 처음 구매하는 사람들과 PC를 업그레이드하는 수요로 업계의 새로운 표준이 되었습니다.

작년보다 2배 증가한 250개 이상의 RTX 최적화 게임과 앱을 경험하는 사람들의 수요로 업계의 새로운 표준이 되었습니다.

We estimate that almost a-third of the GeForce Gaming GPU installed base is now on RTX.

RTX has brought tremendous energy into the gaming world, and has helped drive a sustained expansion in our higher-end platforms and installed base with significant runway still ahead. Overall, end demand remained solid though mixed by region, and demand in America's remained strong.

우리는 GeForce Gaming GPU 설치 기반의 거의 3분의 1이 현재 RTX로 추정합니다.

RTX는 게임 세계에 엄청난 에너지를 가져다주었고, 우리의 고급 플랫폼과 설치 기반에서 지속적인 확장을 추진하는 데 도움이 되었으며 상당한 활주로가 아직 남아 있습니다. 전반적으로 최종 수요는 지역별로 혼재했지만 견조한 상태를 유지했으며 미국의 수요는 강세를 유지했습니다.

However, we started seeing softness in parts of Europe related to the war in the Ukraine and parts of China due to the COVID lockdowns. As we expect some ongoing impact as we prepare for a new architectural transition later in the year, we are projecting Gaming revenue to decline sequentially in Q2.

그러나 우리는 우크라이나의 전쟁과 관련된 유럽 일부와 COVID 봉쇄로 인해 중국 일부에서 약함을 보기 시작했습니다. 올해 후반에 새로운 아키텍처 전환을 준비하면서 지속적인 영향이 있을 것으로 예상하므로

게이밍부문 매출이 2분기에 전분기대비 감소할 것으로 예상합니다.

Channel inventory has nearly normalized and we expect it to remain around these levels in Q2.

The extent in which cryptocurrency mining contributed to Gaming demand is difficult for us to quantify with any reasonable degree of precision.

The reduced pace of increase in Ethereum network hash rate likely reflects lower mining activity on GPUs. W

e expect a diminishing contribution going forward.

채널 재고는 거의 정상화되었으며 2분기에도 이 수준을 유지할 것으로 예상합니다.

암호화폐 채굴이 게이밍부문 수요에 기여한 정도는 합리적인 정밀도로 정량화하기 어렵습니다.

이더리움 네트워크 해시 비율의 증가 속도 감소는 GPU에서 더 낮은 채굴 활동을 반영할 가능성이 있습니다.

우리는 앞으로 감소를 예상합니다.

Laptop Gaming revenue posted strong sequential and year-on-year growth, driven by the ramp of the NVIDIA RTX 30 Series lineup. With this year's spring refresh and ahead of the upcoming back-to-school season, there are now over 180 laptop models featuring RTX 30 Series GPUs and our energy-efficient thin and light Max-Q technologies, up from 140 at this time last year.

노트북 게이밍부문 매출은 NVIDIA RTX 30 시리즈 라인업의 증가에 힘입어 강력한 전분기대비 및 전년 대비 성장을 기록했습니다. 올해 봄의 새로 고침과 다가오는 개학 시즌을 앞두고 RTX 30 시리즈 GPU와 에너지 효율적인 얇고 가벼운 Max-Q 기술을 탑재한 180개 이상의 노트북 모델이 있습니다.

Driving this growth are not just gamers, but also the fast-growing category of content creators from whom we offer dedicated NVIDIA studio drivers. We've also developed applications and tools to empower artists from Omniverse for advanced 3D and collaboration to broadcast for live streaming to canvas for painting landscapes with AI.

이러한 성장을 주도하는 것은 게이머뿐만 아니라 NVIDIA 스튜디오 전용 드라이버를 제공하는 빠르게 성장하는 콘텐츠 제작자 카테고리입니다. 또한 고급 3D 및 협업을 위해 Omniverse의 아티스트가 AI로 풍경을 그리기 위해 캔버스로 라이브 스트리밍을 방송할 수 있도록 지원하는 응용 프로그램과 도구를 개발했습니다.

The creator economy is estimated at $100 billion and powered by 80 million individual creators and broadcasters. We continued to build out our GeForce NOW cloud gaming service.

제작자 경제는 1,000억 달러로 추산되며 8천만 명의 개인 제작자와 방송인이 운영합니다.

우리는 계속해서 GeForce NOW 클라우드 게임 서비스를 구축했습니다.

Gamers can now access RTX 3080 class streaming, our new top-tier offering with subscription plans of $19.99 a month. We added over 100 games to the GeForce NOW library, bringing the total to over 1,300 games.

And last week, we launched Fortnite on GeForce NOW with touch controls for mobile devices, streaming through the Safari web browser on iOS and the GeForce NOW Android app.

이제 게이머는 RTX 3080 클래스 스트리밍에 액세스할 수 있습니다.

RTX 3080 클래스 스트리밍은 월 $19.99의 구독 요금제가 포함된 새로운 최상위 제품입니다.

GeForce NOW 라이브러리에 100개 이상의 게임을 추가하여 총 1,300개 이상의 게임을 제공합니다.

그리고 지난 주에 iOS의 Safari 웹 브라우저와 GeForce NOW Android 앱을 통해 스트리밍하는 모바일 장치용 터치 컨트롤이 있는 GeForce NOW에서 Fortnite를 출시했습니다.

Moving to Pro Visualization. Q1 revenue was $622 million was down sequentially 3% and up 67% from a year ago. Demand remains strong as enterprises continued to build out their employee's remote office infrastructure to support hybrid work. Sequential growth in the mobile workstation GPUs was offset by lower desktop revenue.

Pro Visualization으로 이동합니다.

1분기 매출은 6억 2,200만 달러로 전분기대비 3% 감소했고 전년 동기대비 67% 증가했습니다.

기업이 하이브리드 작업을 지원하기 위해 직원의 원격 사무실 인프라를 계속 구축함에 따라 수요는 여전히 강력합니다.

모바일 워크스테이션 GPU의 전분기대비 성장은 데스크톱 매출 감소로 상쇄되었습니다.

Strong year-on-year growth was supported by the NVIDIA RTX Ampere architecture product cycle.

Top use cases include digital content creation at customers such as Sony Pictures Animation and medical imaging at customers such as Medtronic.

전년 동기대비 강력한 성장은 NVIDIA RTX Ampere 아키텍처 제품 주기에 의해 뒷받침되었습니다.

주요 사용 사례로는 Sony Pictures Animation과 같은 고객의 디지털 콘텐츠 제작과 Medtronic과 같은 고객의 의료 영상이 있습니다.

In just its second quarter of general availability, our Omniverse enterprise software is being adopted by some of the world's largest companies. Amazon is using Omniverse to better optimize warehouse design and flow and to train more intelligent robots.

일반 공급의 2분기만에 우리의 Omniverse 엔터프라이즈 소프트웨어가 세계 최대 기업들에 의해 채택되고 있습니다. Amazon은 Omniverse를 사용하여 창고 설계와 흐름을 더 잘 최적화하고 더 지능적인 로봇을 훈련시키고 있습니다.

Kroger is using Omniverse to optimize store efficiency with digital twin store simulation. And PepsiCo is using Omniverse digital twins to improve the efficiency and environmental sustainability of the supply chain.

Kroger는 Omniverse를 사용하여 디지털 트윈 매장 시뮬레이션으로 매장 효율성을 최적화하고 있습니다.

그리고 PepsiCo는 Omniverse 디지털 트윈을 사용하여 공급망의 효율성과 환경적 지속 가능성을 개선하고 있습니다.

(분:디지털트윈은 엔비디아의 메타버스 플랫폼으로 가상세계에서 현실세계와 똑같은 환경을 만들어

여러가지 실험들을 실시하여 데이터 값을 얻는 것이다.)

Omniverse is also expanding our GPU sales pipeline, driving higher end and multiple GPU configurations.

The Omniverse ecosystem continues to rapidly expand with third-party developers in the robotics, industrial automation, 3D design and rendering ecosystems developing connections to Omniverse.

Omniverse는 또한 GPU 판매 파이프라인을 확장하여 고급 및 다중 GPU 구성을 추진하고 있습니다.

Omniverse 에코시스템은 로봇 공학, 산업 자동화, 3D 디자인 및 렌더링 에코시스템의 타사 개발자와 함께

Omniverse와의 연결을 개발하면서 계속해서 빠르게 확장되고 있습니다.

Moving to automotive. Q1 revenue of $138 million, increased 10% sequentially and declined 10% from the year ago quarter. Our DRIVE O-RAN SoC is now in production and kicks off a major product cycle with auto customers ramping in Q2 and beyond. O-RAN has great traction in the marketplace with over 35 customer wins from automakers, truck makers and robotaxi companies.

자동차로 이동합니다.

1분기 매출은 1억 3,800만 달러로 전분기 대비 10% 증가했으며 전년 동기 대비 10% 감소했습니다.

우리의 DRIVE O-RAN SoC는 현재 생산 중이며 2분기와 그 이후에 자동차 고객이 급증하면서 주요 제품 주기를

시작합니다.

O-RAN은 자동차 제조업체, 트럭 제조업체 및 로보택시 회사에서 35개 이상의 고객을 확보하여

시장에서 큰 견인력을 가지고 있습니다.

In Q1, BYD, China's largest EV maker and Lucid an award winning EV pioneer were the latest to announce that they are building their next-generation fleets on DRIVE O-RAN. Our automotive design win pipeline now exceeds $11 billion over the next six years, up from $8 billion just a year ago.

1분기에 중국 최대 EV 제조사인 BYD와 수상 경력에 빛나는 EV 선구자 Lucid가 DRIVE O-RAN을 기반으로 차세대 차량을 구축하고 있다고 발표했습니다.

우리의 자동차 설계 수상 파이프라인은 이제 1년 전의 80억 달러에서 향후 6년 동안 연간 110억 달러를 초과할 것입니다.

Moving to Data Center. Record revenue of $3.8 billion grew 15% sequentially and accelerated to 83% growth year-on-year. Revenue from hyperscale and cloud computing customers more than doubled year-on-year, driven by strong demand for both external and internal workloads. Customers remain supply constrained in their infrastructure needs and continue to add capacity as they try to keep pace with demand.

데이터 센터부문으로 이동합니다.

38억 달러의 기록적인 매출은 전분기 대비 15% 성장했으며 전년 동기 대비 83% 성장했습니다.

하이퍼스케일 및 클라우드 컴퓨팅 고객의 매출은 외부 및 내부 워크로드에 대한 강력한 수요에 힘입어

전년 대비 2배 이상 증가했습니다.

고객은 인프라 요구 사항에 따라 공급이 제한된 상태를 유지하고 수요에 보조를 맞추기 위해 계속해서 용량을 추가합니다.

Revenue from vertical industries grew a strong double-digit percentage from last year. Top verticals driving growth this quarter include; consumer Internet companies, financial services and telecom. Overall, Data Center growth was driven primarily by strong adoption of our A100 GPU for both training and inference with large volume deployments by hyperscale customers and broadening adoption across the vertical industries.

수직 산업의 매출은 작년보다 두 자릿수의 강력한 성장을 보였습니다.

이번 분기 성장을 주도하는 상위 업종은 다음과 같습니다.

소비자 인터넷 회사, 금융 서비스 및 통신입니다.

전반적으로 데이터 센터 성장은 주로 하이퍼스케일 고객의 대규모 배포와 수직 산업 전반에 걸친 채택 확대에 대한

교육 및 추론 모두에 A100 GPU의 강력한 채택에 의해 주도되었습니다.

Top workloads includes; recommender systems, conversational AI, large language models and cloud graphics. Networking revenue accelerated on strong broad-based demand for our next-generation 25, 50 and 100-gig ethernet adapters. Customers are choosing NVIDIA's networking products for their leading performance and robust software functionality.

In addition, networking revenue is benefiting from growing demand for DGX super pods and cross-selling opportunities. Customers are increasingly combining our compute and networking products to build what are essentially modern AI factories with data as the raw material input and intelligence as the output. Our networking products are still supply constrained though we expect continued improvement throughout the rest of the year.

One of the biggest workloads driving adoption of NVIDIA AI is natural language processing, which has been revolutionized by transformer based models. Recent industry breakthroughs traced to transformers include; large language models like GPT-3, NVIDIA Megatron BERT for drug discovery and DeepMind AlphaFold for a protein structure prediction.

Transformers allow self-supervised learning without the need for human labeled data. They enable unprecedented levels of accuracy for TAF such as text generation, translation, summarization and answering questions. To do that, Transformers use enormous training data sets and very large networks well into the hundreds of billions of parameters. To run these giant models without sacrificing low inference times, customers like Microsoft are increasingly deploying NVIDIA AI, including our NVIDIA Ampere architecture-based GPUs and full software stack.

In addition, we are seeing a rising wave of customer innovation using large language models that is driven by increased demand for NVIDIA AI and GPU instances in the cloud. At GTC, we announced our next-generation Data Center GPU, the H100 based on the new or upper architecture. Packed with 80 billion transistors, H100 is the world's largest, most powerful accelerator, offering an order of magnitude leap in performance over the A100. We believe H100 is hitting the market at the perfect time. H100 is ideal for advancing large language models and deep recommender systems the two largest scale AI workloads today

We are working with leading server makers and hyperscale customers to qualify and ramp H100. As well as the new DGX H100 AI supercomputing system will ramp in volume late in the calendar year. Building on the H100 product side, we are on track to launch our first ever Data Center CPU, Grace, in the first half of 2023. Grace is the ideal CPU for AI factories. This week at COMPUTEX, we announced that dozens of server models based on Grace will be brought to market by the first wave of system builders, including ASUS, Foxconn, Gigabyte, QCT, Supermicro and Wiwynn. These servers will be powered by the NVIDIA Grace CPU Super Chip, which features two CPUs and the Grace Upper Super Chip, which pairs an NVIDIA Hopper GPU with an NVIDIA Grace CPU in an integrated model.

We've introduced new reference designs based on Grace for the massive new workloads of next-generation data centers. CGX for cloud graphics and gaming, OVX for digital twins or Omniverse and HGX for HPC and AI. These server designs are all optimized for NVIDIA's rich accelerated computing software stacks and can be qualified as part of our NVIDIA certified systems lineup.

The enabler for the Grace Hopper and Grace Super Chips is our ultra energy-efficient, low-latency, high-speed memory coherent interconnect NVLink, which scales from die to die, chip to chip and system to system. With NVLink, we can configure Grace and Hopper to address a broad range of workloads.

Future NVIDIA chips, the CPUs, GPUs, DPUs, NICs and SoCs will integrate NVLink just like Grace Hopper based on our world-class SERDES technology. We're making NVLink open to customers and partners to implement custom chips that connect to NVIDIA's platforms.

In networking, we're kicking off a major product cycle with the introduction of Spectrum-4, the world's first 400-gigabit per second end-to-end Ethernet networking platform, including the Spectrum-4 Switch, ConnectX-7 SmartNIC, Bluefield-3 DPU and the DOCA software. Built for AI and video Spectrum 4 arrives as data centers are growing exponentially and demanding extreme performance, advanced security and powerful features to enable high-performance advanced virtualization and simulation at scale. Across our businesses, we are launching multiple new GPU, CPU, DPU and SOC quarters over the coming quarters, with a ramp in supply to support the customer demand.

Moving to the rest of the P&L, GAAP gross margin for the first quarter was 65.5% and non-GAAP gross margin was up 67.1%, up 90 basis points from a year ago, and up 10 basis points sequentially. We have been able to offset rising costs and supply chain pressures. We expect to maintain gross margins at current levels in Q2.

Going forward, as new products ramp and software becomes a larger percent of revenue, we have opportunities to increase gross margins longer term. GAAP operating margin was 22.5%, impacted by a $1.35 billion acquisition termination charge related to the ARM transaction.

Non-GAAP operating margin was 47.7%. We are closely managing our operating expenses to balance the current macro environment with our growth opportunities, and we've been very successful in hiring so far this year and are now slowing to integrate these new employees.

This also enables us to focus our budget on taking care of our existing employees as inflation persist. We are still on track to grow our non-GAAP operating expenses in the high 20s range this year. we expect sequential increases to level off after Q2 as the first half of the year includes a significant amount of expenses related to the bring-up of multiple new products, which should not reoccur in the second half.

During Q1, we repurchased $2 billion of our stock. Our Board of Directors increased and extended our share repurchase program to repurchase an additional common stock up to a total of $15 billion through December 2023.

Let me now turn to the outlook for the second quarter of fiscal 2023. Our outlook assumes an estimated impact of approximately $500 million relating to Russia and China COVID lockdowns. We estimate the impact of lower sell-through in Russia and China to affect our Q2 Gaming sell-in by $400 million.

Furthermore, we estimate the absence of sales to Russia to have a $100 million impact on Q2 in Data Center. We expect strong sequential growth in Data Center and Automotive to be more than an offset by the sequential decline in Gaming. Revenue is expected to be $8.1 billion, plus or minus 2%. GAAP and non-GAAP gross margins are expected to be 65.1% and 67.1%, respectively, plus or minus 50 basis points.

GAAP operating expenses are expected to be $2.46 billion. Non-GAAP operating expenses are expected to be $1.75 billion. GAAP and non-GAAP other income and expenses are expected to be an expense of approximately $40 million, excluding gains and losses on non-affiliated investments. GAAP and non-GAAP tax rates are expected to be 12.5% plus or minus 1%, excluding discrete items. And capital expenditures are expected to be approximately $400 million to $450 million. Further financial details are included in the CFO commentary and other information available on our IR website.

In closing, let me highlight the upcoming events for the financial community. We will be attending the BofA Securities Technology Conference in person on June 7, where Jensen will participate in a keynote fireside chat. Our earnings call to discuss the results of our second quarter of fiscal 2023 is scheduled for Wednesday, August 24.

We will now open the call for questions. Operator, can you please poll for questions? Thank you.

Question-and-Answer Session

Operator

Thank you. [Operator Instructions] We'll take our first question from C.J. Muse with Evercore ISI. Your line is open.

C.J. Muse

Yes, good afternoon. Thank you for taking the question. I guess would love to get an update on how you're thinking about the Gaming cycle from here. The business has essentially doubled over the last two years. And now we've got some crosswinds with crypto falling off, channel potentially clearing ahead of a new product cycle. You talked about macro challenges. But at the same time, only a third of the installed base has RTX and we're moving out from under supply. So we'd love to hear your thoughts from here once we get beyond kind of the challenges around COVID lockdown in the July quarter? How are you thinking about Gaming trends?

Jensen Huang

Yes, C.J., thanks for the question. The -- you captured a lot of the dynamics well in your question. The underlying dynamics of the Gaming industry is really solid, net of the situation with COVID lockdown in China and Russia. The rest of the market is fairly robust and we expect the Gaming dynamics to be intact.

The several things that are driving the Gaming the last two years alone, 100 million new gamers came into the PC industry. The format has expanded tremendously. And the ways that people are using their PCs to connect with friends, to be an influencer as a platform for themselves, use it for broadcast. So, many people are now using their home PCs as their second workstation, if you will, second studio. Because they're also working from home. It is our primary way of communicating these days. The need for GeForce PCs have never been greater. And so I think the fundamental dynamics are really good. And so as we look into the second half of the year, we look -- it's hard to predict exactly what -- when COVID and the war in Russia is going to be behind us. But nonetheless, the governing dynamics of the Gaming industry is great.

Operator

Next, we'll go to Matt Ramsay with Cowen. Your line is open.

Matt Ramsay

Thank you very much. Good morning. Jensun, I wanted to ask a bit of a question on the Data Center business. In this upcoming cycle with H-100, there's some I/O upgrades that are happening in servers that I think are going to be a fairly strong driver for you in addition to what's going on with Hopper and the huge performance leaps that are there.

I wanted to ask a longer-term question, though, around your move to NVLink with Grace and Hopper and what's going on with your whole portfolio. Do you envision the business continuing to be sort of card-driven attached to third-party servers, or do you think revenue shifts dramatically, or in a small way, over time, to be more sort of vertically integrated all of the chips together on NVLink? And how is the industry sort of responding to that potential move? Thanks.

Jensen Huang

Yes. I appreciate the question. The -- let's see, the first point that you made is a very big point. The next generation of servers that are being teed up right now are all Gen 5. The I/O performance is substantially higher than what was available before.

And so, you're going to see a pretty large refresh as a result of that. Brand-new networking cards from our company and others. Gen 5, of course, drives new platform refresh. And so, we're perfectly timed to ramp into the Gen 5 generation with Hopper.

There are a lot of different system configurations you want to make. If you take a step back and look at the type of systems that are necessary for data processing, scientific computing, machine learning and training, inference done in the cloud for hyperscale nature, done on-prem for enterprise computing, done at the edge.

Each one of these workloads and deployment locations, the way that you manage would dictate a different system architecture. So there isn't one size that fits all, which is one of the reasons why it's so terrific that we support PCI Express that we innovated chip-to-chip interconnect for diverse -- before anybody else did, this is now some seven years ago, we're in our fourth generation of NVLink that allows us to connect two chips next to each other, two dies, two chips, two modules, two SXM modules to two systems to multiple systems.

And so our coherent chip-to-chip link, NVLink has made it possible for us to mix and match chips, dies, packages, systems and all of these different types of configurations. And I think that, over time, you're going to see even more types of configurations.

And the reason for that has to do with a couple of very important new type of data centers that are emerging. And you're starting to see that now with fairly large installations, infrastructures with NVIDIA, HPC and NVIDIA AI.

These are really AI factories where you're processing the data, refining the data and turning that data into intelligence. These AI factories are essentially running one major workload and they're running at 24/7.

Deep recommender systems is a good example of that. In the future, you're going to see large language models essentially becoming a platform themselves. That would be running 24/7, hosting a whole bunch of applications.

And then on the other end, you're seeing data centers at the edge that are going to be robotics or autonomous data centers that are running 24/7. They are going to be running in factories and retail stores and warehouses, logistics warehouses, all over the world. So these two new types of data centers are just emerging, and they also have different architectures. So I think the net of it all is that our ability to support every single workload because we have a universal accelerator, running every single workload from data processing to data analytics to high-performance computing to training to inference that we can support Arm and x86 that we support PCI Express to Multisystem NVlink to multi-chip NVLink to multi-die NVLink, that capability for us is -- makes it possible for us to really be able to serve all of these different segments.

With respect to vertical integration, I think that system integration, the better way to make me saying that is that system integration is going to come in all kinds of different ways. We're going to do semi-custom chips as we've done with many companies in the past, including Nintendo. We'll do semi-custom chiplets as we do with NVLink. NVLink is open to our partners. And they could bring it to any fab and connect it coherently into our chip. We could do multi module packages. We could do multi-package systems. So there's a lot of different ways to do system integration.

Operator

Next, we'll go to Stacy Rasgon with Bernstein Research. Your line is now open.

Stacy Rasgon

Hi, guys. Thanks for taking my questions. I wanted to follow up on the sequential. So Colette, I know you said the $500 million was a $400 million hit to Gaming and a $100 million hit to data. So I'm assuming that -- that doesn't mean the Gaming is down $400 million. I mean it's Gaming -- do you see Gaming actually down more than the actual Russia and lockdown hit. And I guess just how do I think about the relative sequentials of the businesses in light of those constraints that you guys are facing?

Colette Kress

Sure. Let me start first with what does that mean to Gaming. What does that mean to Gaming for Q2? We do expect Gaming to decline into Q2. We still believe our end demand remains very strong.

Ampere has just been a great architecture, and there's many areas where we continue to see strength and growth in both our sell-through and probably what we will see added into that channel as well.

But in total, Q2 Gaming will decline from last quarter from Q1 that it will probably decline in the teens.

As we try and work through some of these lockdowns in China, which are holding us up. So overall, the demand for Gaming is still strong. We still expect end demand to grow year-over-year in Q2.

2분기 게이밍부문 매출은 1분기대비 10%대 감소할 것이다.

하지만 게이밍 수요는 여전히 강하기 때문에 전년 동기대비로는 증가할 것으로 예상한다.

Operator

Next, we'll go to Mark Lipacis with Jefferies. Your line is open.

Mark Lipacis

Hi, thanks for taking my question. If you listen to the networking OEMs, this earnings season, it seems that there was a lot of talk about increased spending by enterprises on their data centers and sometimes you hear them talking about how this is being driven by AI. You talked about your year-over-year growth in your cloud versus enterprise spending. I wonder if you could talk about what you were seeing sequentially? Are you seeing a sequential inflection in the enterprise? And can you talk about the attach rate of software for enterprise versus data centers. And, which software is -- are you seeing the most interest? I know you talked about, is it Omniverse? Is it natural language processing, or is there one big driver, or is it a bunch of drivers for the various different software packages you have? Thank you.

Jensen Huang

Yeah. Thanks, Mark. We had a record Data Center business this last quarter. We expect to have a record, another record quarter this quarter, and we're fairly enthusiastic about the second half.

AI and data-driven machine learning techniques for writing software and extracting insight from the vast amount of data that companies have is incredibly strategic to all the companies that we know. Because in the final analysis, AI is about automation of intelligence and most companies are about domain-specific intelligence.

엔비디아는 지난 분기 데이터센터부문에서 사상 최대 매출을 달성했다.

우리는 이번 분기에도 또한번 사상 최대 매출을 달성할 것으로 예상하고 하반기에도 대단히 고무적이다.

소프트웨어를 작성하고 광대한 양의 데이터에서 결과물을 추출해내는 인공지능과 데이터 드리븐 머신러닝 기술은

우리가 아는 모든 회사들에게 믿을 수없을 정도로 전략적이다.

최종 분석에서 AI는 지능의 자동화에 관한 것이고 대부분의 기업은 영역별 지능에 관한 것이기 때문입니다.

We want to produce intelligence. And there are several techniques now that have been created to make it possible for most companies to apply their data to extract insight and to automate a lot of the predictive things that they have to do and do it quickly. And so I think the trend that you hear other people are experiencing about machine learning, data analytics, data driven insights, artificial intelligence. However, it's described, it's all exactly the same thing. And it's sweeping just about every industry and every company.

Our networking business is also highly supply constrained. Our demand is really, really high. And it requires a lot of components aside from just our chips. Components and transceivers and connectors and cables. And just -- it's a really -- it's a complicated system, the network, and there are many physical components. And so the supply chain has been problematic. We're doing our best and our supply has been increasing from Q4 to Q1. We're expecting it to increase in Q2 and increase in Q3 and Q4. And so we're really, really grateful for the support from the component industry around us, and we'll be able to increase that.

With respect to software, there are two, well, first of all, there are all kinds of machine learning models, computer vision, speech AI, natural language understanding, all kinds of robotics applications, the most -- probably the largest, the most visible one is self-driving cars, which is essentially a robotic AI. And then recently, this incredible breakthrough from an AI model called Transformers that has led to really, really significant advances in natural language understanding.

And so they're all these different types of models. There are thousands and thousands of species of AI models and used in all these different industries. One of my favorite, I'll just say it very quickly and I'll answer that question about the software. One of my favorites is using Transformers to understand the language of chemistry or using transformers and using AI models to understand the language of proteins, amino acids, which is genomics.

To apply AI to understand -- to recognize the patterns, to understand the sequence and essentially understand the language of chemistry and biology is a really, really important breakthrough. And all of this excitement around synthetic biology, much of it stands back to the – some of these inventions.

But anyhow, all of these different models need an engine to run on. And that engine is called NVIDIA AI. In the case of hyperscalers, they can cobble together a lot of open source and we provide a lot of our source to them and a lot of our engines to them for them to operate their AI. But for enterprises, they need someone to package it together and be able to support it and refresh it, update it for new architecture, support old architectures in their installed base, etcetera, and all the different use cases that they have. And so that engine is called NVIDIA AI.

It's almost like a sequel engine, if you will. And except this is an engine for artificial intelligence. There's another engine that we provide and that engine is called Omniverse and it's designed for the next wave of AI, where artificial intelligence has to not just manipulate information like recommender systems and conversational systems and such. But it has to interact with physical systems.

Whether it's interacting with physics directly, meaning robotics or being able to automate physical systems like heat recovery steam generators, which is really important today. And so Omniverse is designed to be able to sit at that interface, that intersection between simulation and artificial intelligence, and that's what Omniverse is about.

Omniverse has now – let’s see some -- we're still early in the deployment of Omniverse for commercial license. It's been a couple of quarters now since we've released Omniverse enterprise. And I think, at this point, we have 10% of the world's top 100 companies that are already customers, licensing customers, substantially more who we're evaluating. I think it's been downloaded nearly 200,000 times. It has been tried in some 700 companies.

And Colette highlighted some of the companies, you might see some of the companies that are using it in all kinds of interesting applications at GTC. And so, I fully expect that the NVIDIA AI engine, the Omniverse engine, are going to be very successful for us in the future and contribute greatly to our earnings.

Operator

Next, we'll go to Vivek Arya with BofA Securities. Your line is open.

Vivek Arya

Thanks. Just wanted to clarify, Colette, if your Q2 outlook includes any destocking benefits from the new products that you're planning to launch this year? And then my question is gentleman for you. You're still guiding Data Center to a very strong, I think, close to 70% or so year-on-year growth, despite all the headwinds. Are you worried at all about all the headlines about the slowdown in the macro economy? I like is there any cyclical impact on Data Center growth that we should keep in mind as we think about the second half of the year?

Colette Kress

Yes. Vivek, let me first answer the question that you asked regarding any new products as we look at Q2. As we discussed about it, most of the ramp that we have of our new architectures, we're going to see in the back half of the year. We're going to start to see, for example, Hopper will probably be here in Q3, but starting to ramp closer to the end of the calendar year. So, you should think about most of our product launches to be ramping in the second half of the year on that part. I'll turn it over for Jensen Huang for the rest.

Jensen Huang

Thanks. Our Data Center demand is strong and remains strong. Hyperscale and cloud computing revenues, as you mentioned, has grown significantly. It's doubled year-over-year. and we're seeing really strong adoption of A100. A100 is really quite special and unique in the world of accelerators. And this is one of the really, really great innovations as we extended our GPU from graphics to CUDA to Tensor Core GPUs. It's now a universal accelerator.

And so you could use it for data processing for ETL, for example, extract, transform and load. You could use it for database acceleration. Many sequel functions are accelerated on NVIDIA GPUs. We accelerate Rapids, we accelerate which is the Python version a Data Center scale version of Pandas, we accelerate Spark 3.0. And so from database queries to data processing, to extraction, and transform and loading of data before you do training and inference and whatever image processing or other algorithmic processing you need to do can be fully accelerated on A100.

And so we're seeing great success there. on at the core and closer to what is happening today, you're seeing several different very important new AI models that are being invested in at very, very large scale and with great urgency. You probably have heard about Deep Recommender Systems. This is the economic engine, the information filtering engine of the Internet, if not for the recommender system, it would be practically impossible for us to enjoy our Internet experience shopping experience with trillions of things that are changing in the world every day constantly and be able to use your three-inch phone to even engage the Internet.

And so all of that magic is made possible by this incredible thing call a recommender system second thing is conversational AI. You're seeing chat bots and website customer service, even live customer service being now supported by AI, conversational AI has an opportunity to enhance the customer service on the one hand.

On the other hand, supplement for a lot of labor shortage. And then the third is this groundbreaking piece of work as related to Transformers that led to natural language understanding breakthrough. But within it, is this incredible thing called large language models, which embeds human knowledge because it's been trained and so much data. And we recently announced Megatron 530B. And it was a collaboration we did with Microsoft, the foundation of – I think they call it Turing.

And this language model and others like it, like open AI, GPD 3 are really transformative and they take an enormous amount of computation. However, the net result is a pre-trade model that is really quite remarkable.

Now we're working with thousands of start-ups, large companies that are building who are using the public cloud. And so it's driving a lot of demand for us in the public cloud. I think we have now 10,000 AI inception startups that are working with us and using NVIDIA AI, whether it's on-prem or in the cloud, it saves money, because the computation time is significantly reduced. The quality of service is a lot better and they could do greater things. And so that's driving AI in the cloud. And so all of these different factors, whether it's just the industrial recognition of the importance of AI, the transformative nature of these new AI models recommender systems, large language models, conversational AI. The thousands of companies around the world that are using NVIDIA AI in the cloud -- driving public cloud demand, all of these things are driving our Data Center growth. And so we expect to see Data Center demand remain strong.

Operator

Next, we'll go to Tim Arcuri with UBS. Your line is open.

Tim Arcuri

Thank you very much. I had a question about this $500 million impact for July and whether it's more supply related or demand related. And that's because most others in semis are sort of setting this China stuff, in particular, is more of a logistics issues, so more of a supply issues, but the language Colette you were using in your commentary side of lower sell-through in gaming and sort the absence of sales in Russia, to me that sounds a little more demand which would make sense in the context of this new freeze on hiring that you have.

So, I ask because if it's supply related, then you could argue that it's not perishable and really just timing. But if demand related that might never come back and it to be the beginning of a falling night. So, I wonder if you can sort of walk through that for me? Thanks.

Colette Kress

Thanks, Tim, for the question. Let me try and bet here on the China and Russia, two very different things. The current China lockdowns that we are seeing interestingly has implications to both supply and demand. We have seen challenges in terms of the logistics throughout the country, things going in out of the country. It puts a lot of pressure on just logistics that were already under pressure.

From a demand perspective, it has also been head from the gaming side. You have very large cities that are in full lockdown, focusing really on other important things for the citizens there. So, it's impacting our demand.

We do believe that they will come out of COVID and the demand for our products will come back. We do believe that will occur. The supply will sort it out. It's very difficult to determine how.

Now, in the case of Russia, we're not selling to Russia. That's something that we had announced earlier last quarter. But there were plans and Russia has been a part of our overall company revenue of probably about 2% of our company revenue historically and a little larger percentage when you look at our Gaming business. I hope that helped.

Operator

Next, we'll go to Ambrish Srivastava with BMO. Your line is now open.

Ambrish Srivastava

Hi. Thank you very much Colette and Jensen. I actually really appreciate it that you called out demand from those two companies, it feels like it's healthy to say demand is a problem, so refreshing to hear that.

I had a question on the second half and it relates to both Data Center as well as Gaming. So, last couple of times you have talked publicly, you have made comments that your visibility into the Data Center has never been better. So, I was wondering if you just take out the Russia impact, is that still true, all the orders that you have been getting there intact and you did say that business will see a strong momentum. I just want to make sure that statement of confidence you have made stays?

And then on Gaming, Colette, do we expect second half to be up year-over-year just based on the guide for second quarter? It seems like it could be up sequentially but may not return to year-over-year growth in Q3. Thank you.

Jensen Huang

Yes. Ambrish, thanks for the question. On first principles, it should be the case that our visibility of Data Centers is vastly better, vastly better than a couple of years ago. And the reason for that is several. One, if you recall a couple two, three years ago, deep learning and AI was starting to accelerate in the most computer science deep companies in the world with CSPs and hyperscalers. And -- but just about everywhere else, it was still quite nascent. And there was a couple of reasons for that.

Obviously, the understanding of the technology is not as pervasive at the time. The type of industrial use cases for artificial intelligence requires labeling of data that's really quite difficult. And then now with Transformers, you have unsupervised learning and other techniques, zero-shot learning that allows us to do all kinds of interesting things without having to have human-labeled data. We even have synthetic generated data with Omniverse that helps customers do data generation without having to label data, which is either too costly or, quite frankly, oftentimes impossible.

And so now, the knowledge and the technology has evolved to a place that most of the industries could use artificial intelligence at a fairly effective way and in many industries rather transformative. And so I think, number one, we went from clouds and hyperscalers to all of industries.

Second, we went from training-focused to inference. Most people thought that inference was going to be easy. It turns out the inference is by far the harder. And the reason for that is because there are so many different models and there are so many different use cases and so many quality of service requirements, and you want to run these inference models in a small of a footprint as you can.

And so when you scale out, the number of users that use the service is really quite high. So using acceleration, using NVIDIA's platform, we could inference any model from computer vision to speech to chemistry to biology, you name it. And we do it so quickly and so fast that the cost is very low. And so the more acceleration you do, the more money you will save. And that, I think, that wisdom is absolutely true. And so the second dimension is training to inference.

The third dimension is that we now have so many different types of configurations of systems that we can go from high-performance computing systems all the way to cloud to on-prem to edge. And then the final concept is really this industrial deployment now of AI that's causing us to be able to in just about every industry, find growth. And so as you know, our cloud and hyperscalers are growing very, very quickly. However, the vertical part, vertical industries, which is financial services and retail and telco and all of those vertical industries have also grown very, very nicely. And so, in all of those different dimensions, our visibility should be a lot better. And then starting a couple of years ago, adding the Mellanox portfolio to our company, we're able to provide a lot more solution-oriented end-to-end platform solutions for companies that don't have the skills and don't have the technical depth to be able to stand up these sophisticated systems. And so, our networking business is growing very, very nicely as well.

Operator

Next, we'll go to Harlan Sur with JPMorgan. Your line is open.

Harlan Sur

Hi, good afternoon. Thanks for let me ask the question. I just want to maybe just ask this question a little bit more directly. So, it's good to see the team being able to drive – navigate the dynamic supply chain environment, right? You look strong sequential growth in data center in April, here in the July quarter, even with some demand impact from Russia, right? And so, as we think about the second half of the year, cloud spending is strong, and it's actually, I think, accelerating.

You're getting ready to ramp H100 later in the year. Mellanox, I think, is getting more supply as you move through the year. And in general, I think previously, you guys were anticipating sequential supply and revenue growth for the business through this entire year. I understand the uncertainty around gaming, but does the team expect continued sequential growth in data center through the remainder of the year?

Jensen Huang

Either one of those answers -- the answer is yes. We see a strong demand in data center, hyperscale to cloud computing to vertical industries. Ampere is going to continue to scale out. It's been qualified in every single company in the world. And so, after two years, it remains the best universal accelerator on the planet, and it's going to continue to scale out in all these different domains and different markets.

We're going to layer on top of that, a brand-new architecture Hopper. We’re going to layer on top of that brand-new networking architectures. Quantum 3, CX-7, BlueField 3 and we have increasing supply. And so, we're looking forward to an excellent quarter next quarter again for data centers and going into the second half.

Operator

Next, we'll go to Chris Caso with Raymond James. Your line is open.

Chris Caso

Yes, thank you. Wonder if you could speak a little bit about the purchase obligations, which seemed like they were up again in the quarter. And how that – was that a function of longer-dated obligations or a higher magnitude of obligations? And maybe you could just speak to supply constraints in general. You've mentioned a couple of times in the call, about continued constraints in the networking business. What about the other parts of the business? Where are you still constrained?

Colette Kress

Yes. So let me start here, and I'll see if Jensen wants to add more of that. Our purchase obligations, as well as our prepaid have two major things to keep in mind. One, for the first time ever, we are prepaying to make sure that we have that supply and those commitments long term. And additionally, on our purchase obligations, many of them are for long lead time items that are a must for us to procure to make sure that we have the products coming to market.

A good percentage of our purchase commitments is for our Data Center business, which you can imagine, are much larger systems, much more complex systems and those things that we are procuring to make sure we can feed the demand both in the upcoming quarters and further. Areas in terms of where we are still a little bit supply constrained are networking. Our demand is quite strong. We've been improving it each time. But yes, we still have demand -- excuse me, supply concerns with networking still. Is there others that you want to add on, Jensen?

Jensen Huang

No, I thought you were perfect. That's perfect.

Operator

Our final question comes from Aaron Rakers with Wells Fargo. Your line is open.

Aaron Rakers

Yes, thanks for fitting me in. And most of my questions around Gaming and Data Center have been answered. But I guess I'll ask about the Auto segment. While it's still small, clearly, you guys sound confident in that business starting to see "significant sequential growth" into this next quarter. I'm wondering if you could help us kind of think about the trajectory of that business over the next couple of quarters? And I think, in the past, you've said that, that should start to really inflect higher as we move into the second half of the year. Just curious if you could help us think about that piece of the business?

Jensen Huang

Several data points. We are just starting. We have just started shipping O-RAN in the first quarter of shipping production O-RAN. O-RAN is a robotics processor. It's designed for a software-defined robotic car or robotic pick and placer or a robotic mover, logistics mover.

We've been designed into 35 car and trucks and robo taxi companies and more others, if you include logistics movers and last-mile delivery systems and farming equipment and the number of design wins for O-RAN is really quite fantastic.

O-RAN is a revolutionary processor. And it's designed as a, if you will, a Data Center on a chip. And it is the first Data Center on a chip that is robotic, processes sensor information, it's safe, it has the ability to be rather resilient as confidential computing. It is designed to be secure, designed to be all those things because these data centers are going to be everywhere. And so O-RAN is really a technological marvels in production. We experienced very likely the lowest auto quarter in some time for some time.

And the reason for that is because over the next six years-or-so, we have $11 billion and counting of business that we've secured estimated. And so I think it's a fairly safe thing to say now that O-RAN and our autonomous vehicle and robotics business is going to be our next multibillion dollar business. It's on its way surely there. The robotics and autonomous systems and autonomous machines, whether they move or not move, but AI systems that are at the physical edge is surely going to be the next major computing segment. It is surely going to be the next major Data Center segment. We've been working in this area, as you know, for a decade. We have a fair amount of expertise in this area.

And O-RAN is just one example of our work here. We have four pillars to our strategy for autonomous systems. Starting from the data processing and the AI training part of it, to train robotics AIs; second, to simulate robotics AIs, which is omniverse; third, to the memory of the robotics AI otherwise known as mapping; and then finally, the actual robotics application and the robotics processor in the system, and that's where O-RAN goes. But O-RAN is just one of our four pillars of our robotics strategy and the next wave of AI. And so I am really optimistic and really enthusiastic about the next phase of the computer industry's growth. And I think a lot of it is going to be at the edge. A lot of it's going to be about robotics.

Operator

Thank you. I'll now turn it back over to Jensen Huang for any additional closing remarks.

Jensen Huang

Thanks, everyone. The full impact and duration of the war in Ukraine and COVID lockdowns in China is difficult to predict. However, the impact of our technology and our market opportunities remain unchanged. The effectiveness of deep learning AI continues to stand. The transformer model, which led to the natural language understanding breakthroughs is being advanced to learn patterns with great spatial, sequential and temporal complexity.

Researchers are creating transformer models that are revolutionizing applications from robotics to drug discovery. The effectiveness of deep learning AI is driving companies across industries to adopt NVIDIA for AI computing. We're focused on four major initiatives. First, ramping our next generation of AI infrastructure chips and platforms, Hopper GPU, BlueField DPU, NVLink, InfiniBand, Quantum InfiniBand, Spectrum Ethernet Networking. And all this to help customers build their AI factories and take advantage of new AI breakthroughs like transformers.

Second, ramping our system and software industry partners to launch Grace, our first CPU. Third, ramping O-RAN, our new robotics processor and nearly 40 customers building cars, robo taxis, trucks, delivery robots, logistics robots, farming robots to medical instruments. And fourth, with our software platforms, adding new value to our ecosystem with NVIDIA AI and NVIDIA Omniverse and expanding into new markets with new CUDA acceleration libraries. These initiatives will greatly advance AI. And while continuing to extend this most impactful technology of our time to scientists in every field and companies in every industry. We look forward to updating you on our progress next quarter. Thank you.

Operator

This concludes today's conference call. You may now disconnect.

'마이크로소프트 -엔비디아-AMD-인텔' 카테고리의 다른 글

| 메타버스, 디지털트윈으로 완성 (0) | 2022.06.14 |

|---|---|

| 엔비디아는 지속적인 성장이 희망을 제공(2022.06.12) (0) | 2022.06.13 |

| AMD 실적 발표 (0) | 2022.05.04 |

| PC 수요는 약하고 데이터센터 수요는 강하다(2022.04.29) (0) | 2022.04.29 |

| 엔비디아는 주문 취소로 하락(2022.04.11) (0) | 2022.04.12 |