2024.10.04

Nvidia shares pop as CEO touts high Blackwell demand (yahoo.com)

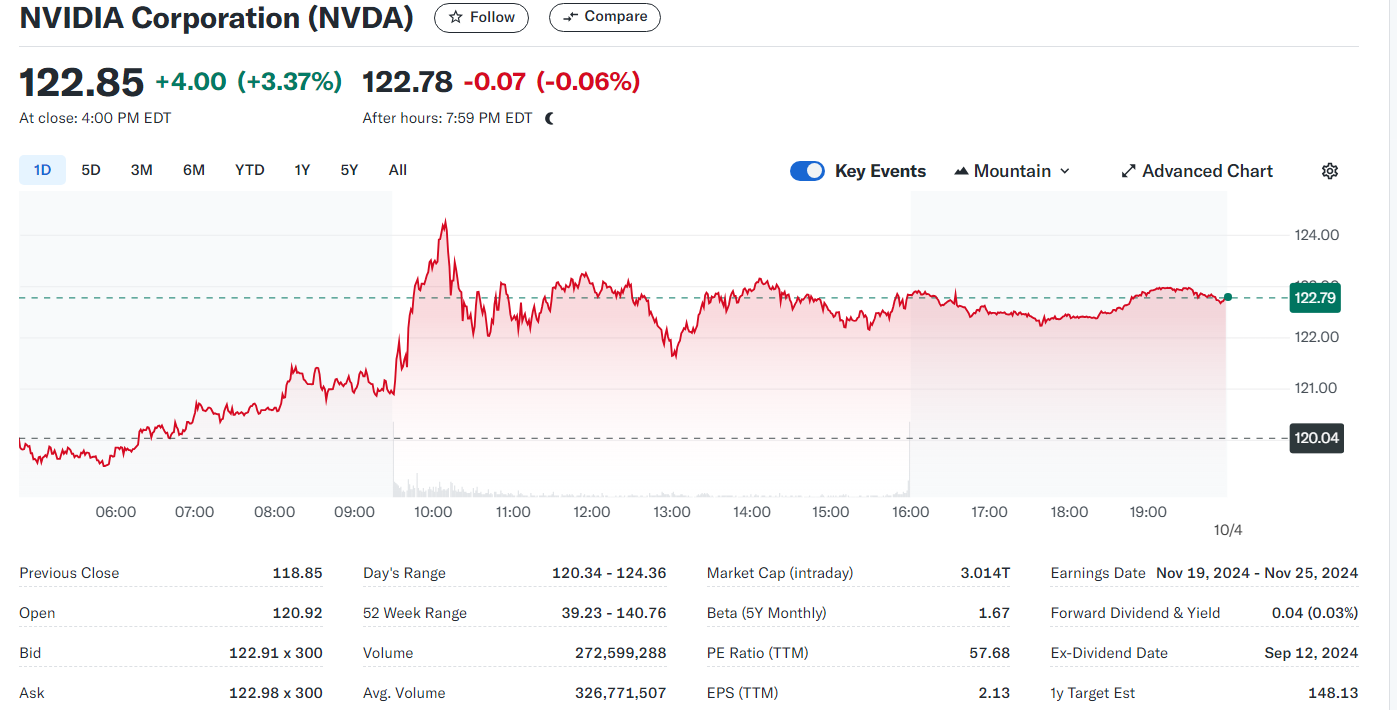

Nvidia (NVDA) stock rallied Thursday following comments from CEO Jensen Huang about overwhelming demand for the company's next-generation AI chips. In a recent CNBC report, Huang described the interest in Nvidia's upcoming Blackwell processors as "insane," emphasizing the strong market appetite for the chipmaker's AI computing hardware.

목요일, 엔비디아(Nvidia) 주가는 CEO 젠슨 황(Jensen Huang)이 차세대 AI 칩에 대한 압도적인 수요에 대해 언급한 후 상승했습니다. 최근 CNBC 보고서에서 황은 엔비디아의 차세대 블랙웰(Blackwell) 프로세서에 대한 관심이 "엄청나다"며, 이 반도체 회사의 AI 컴퓨팅 하드웨어에 대한 강력한 시장 수요를 강조했습니다.

'Market Domination'의 공동 진행자 매디슨 밀스(Madison Mills)와 조시 샤퍼(Josh Schafer)가 그 세부 사항을 분석했습니다.

더 많은 전문가의 통찰과 최신 시장 동향을 알고 싶다면, 'Market Domination'의 전체 에피소드를 시청하세요.

Market Domination co-hosts Madison Mills and Josh Schafer break down the details.

For more expert insight and the latest market action, click here to watch this full episode of Market Domination.

---------------------------------------------

This Hidden Microsoft Metric Bodes Well for Nvidia (yahoo.com)

There are a lot of reasons why investors get excited about Nvidia (NASDAQ: NVDA). The chipmaking giant has been the big winner in the artificial intelligence (AI) infrastructure buildout which helped it create a large moat and become the dominant provider of the graphic processing units (GPUs) used in AI servers.

엔비디아(NASDAQ: NVDA)에 대해 투자자들이 열광하는 이유는 많습니다. 이 반도체 거대 기업은 인공지능(AI) 인프라 구축에서 큰 승자가 되었으며, 이는 회사가 큰 진입 장벽을 형성하고 AI 서버에서 사용되는 그래픽 처리 장치(GPU)의 지배적인 공급자가 되는 데 기여했습니다.

One thing that kept the stock from performing even better is some investors worry that after an initial surge, spending on AI infrastructure may slow from current levels. However, there is a hidden metric found within Microsoft's (NASDAQ: MSFT) recent annual 10-K filing that should allay any worries that there are even brighter days ahead for Nvidia.

그러나 주식이 더 좋은 성과를 내지 못한 이유 중 하나는, 일부 투자자들이 초기 급등 이후 AI 인프라에 대한 지출이 현재 수준에서 둔화될 수 있다는 우려를 가지고 있기 때문입니다. 하지만 마이크로소프트(NASDAQ: MSFT)의 최근 연간 10-K 보고서에서 발견된 숨겨진 지표는 이러한 우려를 불식시키고, 엔비디아의 앞으로 더 밝은 날들이 다가오고 있다는 것을 보여줍니다.

Data center finance leases

Buried within the footnote of its quarterly and annual reports, Microsoft lists the number of finance leases, mostly for data centers, that have yet to commence. The details include the amount of money it has contracted out for leases that it has not yet begun to use.

데이터 센터 금융 리스

분기 및 연간 보고서의 각주에 묻혀 있는 항목 중 하나로, 마이크로소프트는 아직 시작되지 않은 금융 리스(주로 데이터 센터와 관련된)를 명시하고 있습니다. 이 세부 사항에는 마이크로소프트가 아직 사용하지 않은 리스 계약에 따라 이미 할당된 금액이 포함됩니다.

At the end of June, these finance leases that have yet to begin stood at a staggering $108.4 billion. To put that in context, Microsoft had total finance lease liabilities of $27.1 billion at the end of its fiscal 2024 (which ended in June), and its finance leases yet to be commenced at the end of fiscal year 2023 were $34.4 billion. So the amount of finance leases it has contracted out that have yet to begin has more than tripled in the past year.

6월 말 기준, 아직 시작되지 않은 금융 리스는 무려 1,084억 달러에 달했습니다. 이를 맥락으로 설명하자면, 마이크로소프트는 2024 회계연도(6월에 종료)의 말에 총 271억 달러의 금융 리스 부채를 가지고 있었으며, 2023 회계연도 말에 아직 시작되지 않은 금융 리스는 344억 달러였습니다. 즉, 아직 시작되지 않은 금융 리스 계약 금액이 지난 한 해 동안 세 배 이상 증가한 것입니다.

These leases are expected to begin between fiscal years 2025 and 2030. They will have terms ranging from one year to 20 years.

이 리스들은 2025 회계연도에서 2030 회계연도 사이에 시작될 예정이며, 리스 기간은 1년에서 20년까지 다양합니다.

So what does all this mean? Well, finance leases are typically long-term agreements by which the owner of an asset gives control of it to another party in exchange for payments. Usually at the end of the lease, the lessee (the party making payments) has the option to buy the asset for a nominal amount.

그렇다면 이 모든 것이 의미하는 바는 무엇일까요? 금융 리스는 일반적으로 자산 소유자가 해당 자산의 통제권을 대가로 다른 당사자에게 넘겨주고, 그 대가로 일정한 지불을 받는 장기 계약입니다. 일반적으로 리스가 종료될 때, 리스 이용자(지불하는 당사자)는 소액을 지불하고 해당 자산을 구입할 수 있는 선택권을 가지게 됩니다.

Microsoft has made it clear that these leases are for data centers, which means it has contracts in place to spend a whole lot of money on data centers in the coming years. Now some of this could be through partnerships with Oracle and CoreWeave, as speculated earlier by UBS. But this still leaves a lot of new data center space set to be added.

마이크로소프트는 이 리스가 데이터 센터를 위한 것임을 분명히 했습니다. 이는 앞으로 몇 년간 데이터 센터에 막대한 자금을 지출할 계약을 체결했다는 것을 의미합니다. 일부는 이전에 UBS가 추측한 대로 Oracle 및 CoreWeave와의 파트너십을 통해 이루어질 수도 있습니다. 하지만 여전히 많은 새로운 데이터 센터 공간이 추가될 예정입니다.

How will this impact Nvidia?

For Nvidia, this is just another indication of future data center spending -- and, by extension, GPU spending -- in the future. Hyperscalers such as Microsoft are already spending an enormous amount of money on capital expenditures (capex), with much of that directed toward AI and data centers.

엔비디아에게 이는 향후 데이터 센터 지출, 더 나아가 GPU 지출이 증가할 또 다른 신호입니다. 마이크로소프트와 같은 하이퍼스케일러(대규모 데이터 센터 운영업체)들은 이미 상당한 자본 지출(capex)을 하고 있으며, 그 대부분은 AI와 데이터 센터에 집중되고 있습니다.

In fiscal 2024, Microsoft spent $44.5 billion in capex, almost entirely on the cloud and AI, and it said it would spend even more in fiscal year 2025.

마이크로소프트는 2024 회계연도에 445억 달러를 자본 지출로 사용했으며, 거의 전액을 클라우드와 AI에 투자했습니다. 또한 2025 회계연도에는 더 많은 지출을 할 것이라고 발표했습니다.

Half of its capex last fiscal year was on infrastructure to build and lease data centers, and the other half was on CPU and GPU servers. These not-yet-commenced finance lease obligations point to even more spending ahead and the need for more GPU servers.

마이크로소프트는 지난 회계연도 자본 지출의 절반을 데이터 센터를 구축하고 임대하는 인프라에 사용했고, 나머지 절반은 CPU와 GPU 서버에 사용했습니다. 아직 시작되지 않은 금융 리스 의무는 앞으로 더 많은 지출과 GPU 서버의 추가 필요성을 시사합니다.

And Microsoft isn't the only company spending a boatload of money on AI-related capex. Amazon spent $30.5 billion in capex during the first six months of the year and said it would spend more in the second half, the majority to support the growing need for AWS infrastructure.

그리고 마이크로소프트만이 AI 관련 자본 지출에 막대한 돈을 쓰고 있는 것은 아닙니다. 아마존은 올해 상반기에 305억 달러를 자본 지출에 사용했으며, 하반기에도 더 많은 지출을 할 계획이라고 밝혔습니다. 그 중 대부분은 AWS 인프라의 증가하는 수요를 지원하기 위한 것입니다.

Alphabet, meanwhile, is spending over $12 billion a quarter on capex, with the largest component for servers, and Meta Platforms said it expects a significant increase in capex growth in 2025 from its recently upwardly revised 2024 budget of $37 billion to $40 billion.

한편, 알파벳(구글)은 분기마다 120억 달러 이상을 자본 지출에 사용하고 있으며, 그 중 가장 큰 부분은 서버에 할당되고 있습니다. 메타 플랫폼은 최근 2024년 예산을 370억 달러에서 400억 달러로 상향 조정했으며, 2025년에는 자본 지출이 크게 증가할 것으로 예상된다고 밝혔습니다.

These large tech companies are racing to build out their AI infrastructure, and there appears no end in sight. Large language models (LLMs) need more and more computing power to train as they advance, which means not only more GPUs, but exponentially more.

이 대형 기술 기업들은 AI 인프라를 구축하기 위해 경쟁하고 있으며, 그 끝은 보이지 않습니다. 대형 언어 모델(LLM)은 발전할수록 훈련을 위해 더 많은 컴퓨팅 파워가 필요하며, 이는 더 많은 GPU가 필요할 뿐만 아니라 기하급수적으로 증가한다는 것을 의미합니다.

For example, xAI, backed by Elon Musk, trained its next Grok-3 LLM using 100,000 GPUs, five times the amount of Grok-2, while Alphabet said its Llama 4 model would need up to 10 times the GPUs as the 16,000 used for Llama 3.

All these data points continue to indicate that there is still a lot of spending ahead on AI infrastructure and GPUs, all to the benefit of Nvidia.

예를 들어, 엘론 머스크가 지원하는 xAI는 차세대 Grok-3 LLM을 훈련하기 위해 10만 개의 GPU를 사용했는데, 이는 Grok-2에서 사용한 2만 개의 GPU보다 5배 많은 수치입니다. 알파벳(구글) 또한 Llama 4 모델이 Llama 3에 사용된 1만6천 개의 GPU보다 최대 10배 많은 GPU가 필요할 것이라고 밝혔습니다.

이 모든 데이터는 AI 인프라와 GPU에 대한 지출이 앞으로도 상당할 것이며, 이는 엔비디아에 큰 혜택이 될 것임을 계속해서 시사하고 있습니다.

Is it too late to buy Nvidia?

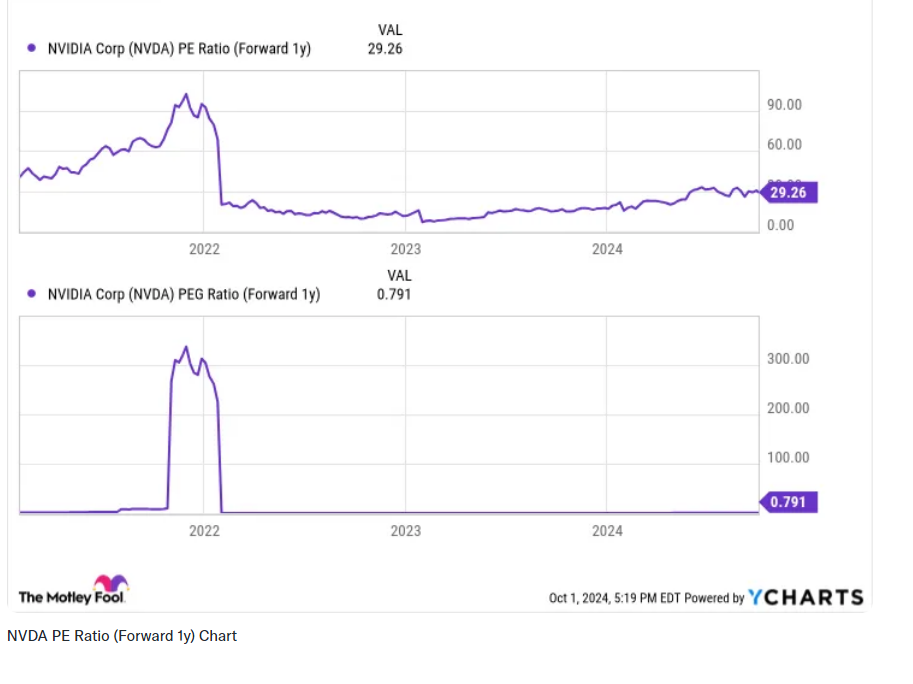

While Nvidia's stock has been a huge winner, the stock is attractively valued given the huge opportunity that appears to still be in front of it. It trades at a forward price-to-earnings ratio (P/E) of only about 29 based on next year's analyst estimates, and a price/earnings-to-growth ratio (PEG) of under 0.8. A PEG under 1 is typically considered undervalued, and growth stocks will often command PEGs well above 1.

엔비디아의 주식은 큰 성공을 거두었지만, 여전히 앞으로의 큰 기회를 고려할 때 매력적인 가치로 평가되고 있습니다. 내년 애널리스트 추정치를 기준으로 예상 주가수익비율(P/E)은 약 29에 불과하며, 주가수익성장비율(PEG)은 0.8 이하입니다. 일반적으로 PEG가 1 이하인 경우 저평가된 것으로 간주되며, 성장주들은 종종 1을 훨씬 넘는 PEG를 기록하곤 합니다.

As such, I think the best approach to take regarding Nvidia is to listen to and follow what Nvidia's largest customers are saying and doing. On that front, it appears those customers plan to spend a lot more money on GPUs from the company in the coming years, with Microsoft looking to be one of the biggest spenders. With Nvidia's stock still attractively priced, I'd be a buyer.

따라서 엔비디아에 대해 가장 좋은 접근 방식은 엔비디아의 주요 고객들이 하는 말과 행동을 주의 깊게 듣고 따르는 것입니다. 이와 관련하여, 이러한 고객들은 앞으로 몇 년 동안 엔비디아로부터 더 많은 GPU를 구매할 계획인 것으로 보이며, 마이크로소프트가 그 중 가장 큰 지출자가 될 것으로 예상됩니다. 엔비디아 주식이 여전히 매력적인 가격에 거래되고 있는 만큼, 저는 매수하는 것이 좋다고 생각합니다.

'엔비디아-마이크로소프트-AMD-인텔' 카테고리의 다른 글

| PEG/5년에서 10년내 부를 가져다 줄 주식-엔비디아(2024.10.09) (19) | 2024.10.09 |

|---|---|

| Nvidia 주식이 561% 더 급등할 수 있다(2024.10.05) (3) | 2024.10.05 |

| 엔비디아는 중국 당국이 자국 기업들에게 Nvidia 칩 구매를 자제하라고 권고하므로 주가가 하락(2024.09.28) (2) | 2024.09.28 |

| "엔비디아 칩 수요 강력" 한마디에 K반도체株 날았다(2024.09.12) (0) | 2024.09.12 |

| 미국 CPI 2.5% 상승 /Nvidia와 AI 랠리를 다시 점화하는 데 많은 시간이 걸리지 않았다.(2024.09.12) (9) | 2024.09.12 |