2024.11.15

Will Nvidia Be a $5 Trillion Stock by 2028?

Nvidia는 2028년까지 시가총액 5조 달러를 달성할 수 있을까?

Nvidia (NASDAQ: NVDA) recently overtook Apple to become the world's largest company in terms of market cap. The chipmaker's rise to the top position is justified thanks to the impressive growth it delivers quarter after quarter on the back of the robust demand for its chip systems, which are playing a central role in the proliferation of artificial intelligence (AI).

이 반도체 거대 기업의 현재 시가총액은 약 3.6조 달러입니다. 긍정적인 점은, 컨센서스 추정치에 따르면 Nvidia의 사업이 앞으로 5년 동안 연평균 57%의 수익 성장률을 기록하며 놀라운 속도로 계속 성장할 것으로 예상된다는 것입니다. Nvidia가 이러한 야심 찬 성장 예상치를 충족시키고 2028년까지 시가총액 5조 달러를 달성할 수 있을까요?

Nvidia's pricing power is going to be a big tailwind for the company

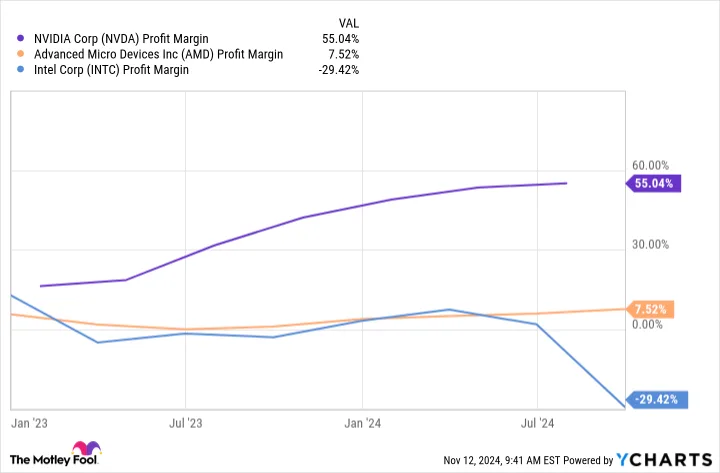

Though Nvidia is a hardware company, it has seen a stunning increase in its profit margin since the beginning of 2023. In fact, Nvidia's profit margin is significantly higher than its rivals Advanced Micro Devices and Intel.

Nvidia의 가격 결정력이 회사의 큰 성장 동력이 될 것입니다

Nvidia는 하드웨어 회사임에도 불구하고, 2023년 초부터 놀라운 수준의 이익률 증가를 보였습니다. 실제로, Nvidia의 이익률은 경쟁사인 AMD(Advanced Micro Devices)와 인텔(Intel)보다 훨씬 높습니다.

NVDA Profit Margin data by YCharts

The company's impressive profitability can be attributed to the pricing power it enjoys in the market for AI graphics processing units (GPUs), thanks to its dominant market share of as much as 95%. According to a report by Citi earlier this year, Nvidia was reportedly charging 4 times the price for its extremely popular H100 AI GPUs compared to AMD's competing MI300X AI accelerator.

Nvidia의 놀라운 수익성은 시장에서 AI 그래픽 처리 장치(GPU)에 대한 가격 결정력 덕분입니다. 이는 최대 95%에 이르는 지배적인 시장 점유율 덕분입니다. 올해 초 Citi의 보고서에 따르면, Nvidia는 AMD의 경쟁 제품인 MI300X AI 가속기와 비교해 자사의 매우 인기 있는 H100 AI GPU에 대해 4배 높은 가격을 책정한 것으로 알려졌습니다.

More specifically, Nvidia was charging somewhere between $30,000 and $40,000 for the H100 when AMD was offering its MI300X for $10,000 to $15,000. A big reason why Nvidia has been able to charge such a massive premium is because of the immense demand for the H100, the waiting period for which extended to as long as eight to 11 months before coming down to three to four months earlier this year.

더 구체적으로, Nvidia는 H100에 대해 3만~4만 달러를 책정한 반면, AMD는 MI300X를 1만~1만 5천 달러에 제공했습니다. Nvidia가 이렇게 높은 프리미엄을 받을 수 있었던 큰 이유는 H100에 대한 엄청난 수요 때문입니다. H100의 대기 기간은 한때 8~11개월에 달했으며, 올해 초에는 3~4개월로 줄어들었습니다.

This reduction in waiting time can be attributed to an increase in the advanced chip packaging capacity by Nvidia's foundry partner, Taiwan Semiconductor Manufacturing, popularly known as TSMC. Market research firm TrendForce reported earlier this year that Nvidia accounted for 40% to 50% of TSMC's advanced packaging capacity.

대기 기간 단축은 Nvidia의 파운드리 파트너인 TSMC(Taiwan Semiconductor Manufacturing Company)의 첨단 칩 패키징 용량 증가 덕분으로 볼 수 있습니다. 시장 조사 기관 TrendForce에 따르면, 올해 초 Nvidia는 TSMC의 첨단 패키징 용량의 40~50%를 차지한 것으로 보고되었습니다.

However, there is a good chance of Nvidia controlling a bigger portion of the supply chain as the chipmaker reported $26.3 billion in data center revenue in the previous quarter (the second quarter of fiscal year 2025, ended July 28, 2024), which is way higher than AMD's $3.5 billion revenue from its data center segment in the third quarter of 2024. This suggests that TSMC may be allocating more capacity to Nvidia than the 40% to 50% estimated by TrendForce.

하지만, Nvidia가 공급망의 더 큰 부분을 통제할 가능성이 높습니다. Nvidia는 2025 회계연도 2분기(2024년 7월 28일 종료)에 데이터 센터 매출로 263억 달러를 기록했는데, 이는 AMD의 2024년 3분기 데이터 센터 부문 매출 35억 달러보다 훨씬 높은 수치입니다. 이는 TSMC가 TrendForce가 추정한 40~50%보다 더 많은 용량을 Nvidia에 할당하고 있을 가능성을 시사합니다.

What's more, AMD's data center GPU revenue guidance for 2024 is nowhere close to the figure that Nvidia could generate from this segment. In simpler words, Nvidia's big share of TSMC's production capacity and the strong demand for its AI GPUs position the company to command a higher price and generate impressive levels of data center revenue.

게다가 AMD의 2024년 데이터 센터 GPU 매출 전망은 Nvidia가 이 부문에서 기록할 수 있는 수치에 비할 바가 아닙니다. 간단히 말하면, TSMC의 생산 용량에서 Nvidia의 큰 점유율과 AI GPU에 대한 강력한 수요가 Nvidia가 더 높은 가격을 요구하고 데이터 센터 매출에서 놀라운 성과를 낼 수 있는 위치에 있음을 보여줍니다.

Another reason why customers are willing to pay a higher price for Nvidia's AI chips is because of a better price-to-performance ratio. For instance, Nvidia's latest Hopper flagship processor -- the H200 -- reportedly outperforms AMD's MI300X by more than 40% in AI inference tasks. The performance advantage explains why Nvidia has been able to charge premium pricing as compared to rivals such as AMD.

고객들이 Nvidia의 AI 칩에 더 높은 가격을 기꺼이 지불하는 또 다른 이유는 더 나은 가격 대비 성능 비율 때문입니다. 예를 들어, Nvidia의 최신 Hopper 플래그십 프로세서인 H200은 AI 추론 작업에서 AMD의 MI300X보다 40% 이상 뛰어난 성능을 발휘하는 것으로 알려졌습니다. 이러한 성능 우위 덕분에 Nvidia는 AMD와 같은 경쟁사에 비해 프리미엄 가격을 책정할 수 있었습니다.

And now, Nvidia is set to push the performance envelope further with the launch of its Blackwell series of AI GPUs, which are reportedly going to be 4 times faster than the Hopper chips. Not surprisingly, Nvidia is expected to charge between $50,000 and $70,000 for its Blackwell GB200 superchips, as per Japanese investment bank Mizuho.

이제 Nvidia는 AI GPU의 성능을 더욱 끌어올리기 위해 Blackwell 시리즈를 출시할 예정이며, 이 칩들은 Hopper 칩보다 4배 더 빠를 것으로 알려졌습니다. 일본 투자은행 미즈호에 따르면, Nvidia는 Blackwell GB200 슈퍼칩에 대해 5만~7만 달러 사이의 가격을 책정할 것으로 예상됩니다.

As a result, Nvidia should be able to maintain its pricing power and clock outstanding earnings growth in the coming years. But will that be enough for it to achieve a $5 trillion market cap?

결과적으로 Nvidia는 가격 책정 권한을 유지하고 향후 몇 년 동안 뛰어난 수익 성장을 기록할 수 있을 것입니다. 그러나 이것만으로 Nvidia가 5조 달러의 시가총액에 도달할 수 있을까요?

The path to a $5 trillion valuation

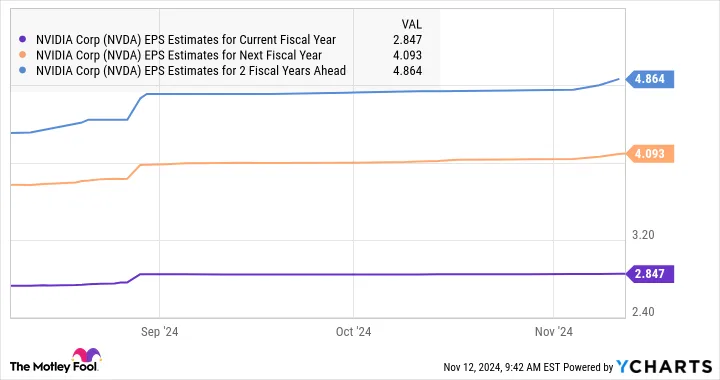

Nvidia finished fiscal 2024 with $1.19 per share in earnings. The following chart shows us that its bottom line could hit $4.84 per share by fiscal 2027, translating into a compound annual growth rate of almost 60% over this three-year period.

**5조 달러 평가로 가는 길**

Nvidia는 2024 회계연도를 주당 1.19달러의 수익으로 마감했습니다. 아래 차트는 2027 회계연도까지 Nvidia의 순이익이 주당 4.84달러에 이를 수 있음을 보여주며, 이는 3년 동안 연평균 성장률(CAGR)이 거의 60%에 달함을 의미합니다.

아래는 엔비디아의 현재와 향후 2년간 주당순이익 추정치.

NVDA EPS Estimates for Current Fiscal Year data by YCharts

Let's assume Nvidia's earnings grow at a significantly conservative rate of 20% in fiscal years 2028 and 2029. Its bottom line could hit $6.97 per share after four years. It is worth noting that Nvidia's fiscal 2029 will coincide with 11 months of calendar year 2028. Assuming Nvidia does achieve $6.97 per share in earnings at that time and trades at 30.7 times forward earnings (in line with the tech-heavy Nasdaq-100 index's forward earnings multiple), its stock price could jump to $214 by then.

Nvidia의 수익이 2028년과 2029년 회계연도 동안 연 20%라는 보수적인 성장률로 증가한다고 가정해봅시다. 이 경우 4년 후 주당 수익이 6.97달러에 이를 수 있습니다. Nvidia의 2029 회계연도는 2028년 달력 기준으로 11개월을 포함한다는 점을 고려할 가치가 있습니다. Nvidia가 그 시점에 주당 6.97달러의 수익을 달성하고, 기술 중심의 나스닥-100 지수의 선행 주가수익비율(P/E)과 일치하는 30.7배로 거래된다고 가정하면, 주가는 그때 214달러까지 상승할 수 있습니다.

That would be a 48% jump from current levels, which would be enough to send Nvidia's market cap to $5 trillion based on its current valuation. Of course, Nvidia could hit that valuation faster assuming it can maintain a higher pace of earnings growth over the next four years, a possibility that cannot be ruled out considering its strong market share and the prospects of the AI chip market.

이는 현재 수준에서 48% 상승한 것으로, 현재 평가 기준으로 Nvidia의 시가총액을 5조 달러로 끌어올리기에 충분한 수치입니다. 물론, Nvidia가 향후 4년 동안 더 높은 수익 성장률을 유지할 수 있다면 이 평가에 더 빨리 도달할 가능성도 있습니다. 이는 Nvidia의 강력한 시장 점유율과 AI 칩 시장의 전망을 고려할 때 배제할 수 없는 시나리오입니다.

'엔비디아-마이크로소프트-AMD-인텔' 카테고리의 다른 글

| 엔비디아 3분기(8-10월) 실적 발표/어닝콜(2024.11.21) (1) | 2024.11.21 |

|---|---|

| 과열 문제로 인해 엔비디아(NVIDIA)의 새로운 블랙웰(Blackwell) AI 서버 출시가 지연될 가능성(2024.11.18) (1) | 2024.11.18 |

| 팔란티어palantir(2024.11.09) (1) | 2024.11.09 |

| Microsoft, Amazon 또는 Alphabet: 누가 클라우드 경쟁에서 앞서가고 있는가?(2024.11.02) (4) | 2024.11.05 |

| Nvidia의 Blackwell 출시 이후 이 데이터 센터 주식이 기하급수적으로 성장할 수 있다-Virtiv(VRT) (3) | 2024.11.04 |