2024.12.11

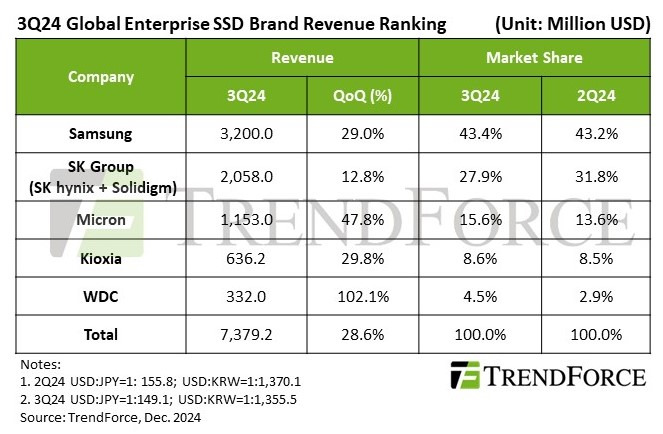

요약:2024년 3분기 글로벌 기업용 SSD 시장은 73.79억달러로 전분기 대비 28.6% 증가했으며,

삼성과 하이닉스가 전체 매출의 75%를 차지했다.

Enterprise SSD Market Sees Strong 3Q24 Growth, Revenue Soars 28.6% on Surging Demand for High-Capacity Models, Says TrendForce

엔터프라이즈 SSD 시장, 2024년3분기 성장률 28.6% 기록하며 강력한 성장세… 고용량 모델 수요 급증 – 트렌드포스(TrendForce)

TrendForce’s latest investigations found that the enterprise SSD market experienced significant growth in 3Q24, driven by robust demand from AI-related applications. Prices surged as suppliers struggled to keep pace with market needs, pushing overall industry revenue up by an impressive 28.6% QoQ.

트렌드포스의 최신 조사에 따르면, 엔터프라이즈 SSD 시장은 2024년 3분기에 AI 관련 애플리케이션의 강력한 수요에 힘입어 상당한 성장을 기록했습니다. 공급업체들이 시장 수요를 따라잡지 못하면서 가격이 상승했고, 업계 전체 매출은 전 분기 대비 28.6% 증가했습니다.

Demand for high-capacity models was especially strong, fueled by the arrival of NVIDIA’s H-series products and sustained orders for AI training servers. As a result, the total procurement volume for enterprise SSDs rose 15% compared to the previous quarter.

특히 NVIDIA의 H 시리즈 제품 출시와 AI 학습 서버에 대한 지속적인 주문이 고용량 모델에 대한 강력한 수요를 견인했으며, 엔터프라이즈 SSD 총 구매량은 전 분기 대비 15% 증가했습니다.

Looking ahead to 4Q24, TrendForce forecasts a slowdown in enterprise SSD revenue as procurement demand begins to cool. Total procurement volume is expected to dip, with the peak buying period behind and server OEM orders being slightly revised downward. As shipment volume declines, overall industry revenue is also projected to decrease in the fourth quarter.

2024년 4분기 전망: 성장 둔화 예상

4분기에는 엔터프라이즈 SSD 매출이 조정 국면에 들어서며 수요가 다소 둔화될 것으로 전망됩니다. 구매량은 정점기를 지나며 감소할 것으로 보이며, 서버 OEM 주문도 소폭 하향 조정될 것으로 예상됩니다. 이에 따라 출하량이 감소하고 업계 매출 역시 하락할 것으로 전망됩니다.

Despite strong market growth, the revenue rankings of enterprise SSD suppliers remained unchanged in Q3. However, differences in order composition for high-capacity products led to varied growth rates among suppliers.

3분기의 강력한 시장 성장에도 불구하고, 엔터프라이즈 SSD 공급업체들의 매출 순위는 변동이 없었습니다. 다만, 고용량 제품에 대한 주문 구성 차이로 인해 공급업체별 성장률에는 차이가 있었습니다.

Samsung maintained its position as the top enterprise SSD supplier with Q3 revenue reaching US$3.2 billion. The company’s growth exceeded expectations thanks to a surge in demand for high-capacity models, although some shipments were delayed due to production adjustments. Enterprise SSDs now account for an increasing share of Samsung’s overall revenue. Looking ahead, Samsung is expected to sustain revenue growth in Q4, driven by strong shipments of sub-8TB SSD products.

1. 삼성전자

삼성전자는 3분기 매출 32억 달러를 기록하며 엔터프라이즈 SSD 공급업체 중 1위를 유지했습니다. 고용량 모델 수요 급증 덕분에 예상치를 초과하는 성장을 기록했으나, 일부 출하량은 생산 조정으로 인해 지연되었습니다. 엔터프라이즈 SSD는 삼성전자 전체 매출에서 점점 더 큰 비중을 차지하고 있으며, 4분기에도 8TB 이하 SSD 제품의 강력한 출하량으로 매출 성장이 지속될 것으로 기대됩니다.

SK Group (SK hynix & Solidigm) retained its position as the second-largest enterprise SSD supplier, with Q3 revenue climbing to $2.058 billion. The company achieved record-high shipments for its comprehensive lineup of AI storage products. In Q4, SK Group’s revenue is expected to remain stable, bolstered by the mass production of its next-generation PCIe 5.0 SSDs, which uses 176-layer TLC NAND. These new products—coupled with existing Solidigm PCIe 4.0 SSDs based on 144-layer TLC and large-capacity QLC SSDs—are expected to sustain revenue.

2. SK 그룹(SK하이닉스 & 솔리다임)

SK 그룹은 3분기 매출 20.58억 달러를 기록하며 2위를 유지했습니다. AI 스토리지 제품군의 기록적인 출하량 덕분에 성장세를 이어갔습니다. 4분기에는 176단 TLC NAND를 기반으로 한 차세대 PCIe 5.0 SSD의 대량 생산과 기존 솔리다임 PCIe 4.0 SSD 및 대용량 QLC SSD의 안정적인 매출로 매출 안정세가 예상됩니다.

Micron secured the third spot, posting Q3 revenue of $1.153 billion thanks to stable growth in shipments of high-capacity enterprise SSDs. The increased output of large-capacity products contributed to a rise in Micron’s supply bits. However, Q4 may pose challenges, as some orders have shifted toward 60TB SSDs—a product that Micron is still in the process of validating with multiple clients. This delay could impact the company’s Q4 revenue growth.

3. 마이크론

마이크론은 3분기 매출 11.53억 달러로 3위를 차지했습니다. 고용량 엔터프라이즈 SSD의 안정적인 출하 증가가 주요 성장 동력이었습니다. 하지만 4분기에는 일부 주문이 60TB SSD로 전환되며 도전에 직면할 가능성이 있습니다. 이 제품은 아직 여러 고객사와의 검증 과정을 거치는 중이며, 이러한 지연이 마이크론의 4분기 매출 성장에 영향을 미칠 수 있습니다.

Kioxia saw its Q3 revenue climb to $636 million, ranking fourth among suppliers. While Kioxia’s shipment volume increased, its growth in high-capacity product sales lagged behind competitors. To counterbalance this, the company capitalized on tight supply for sub-8TB SSDs, strengthening partnerships with key North American clients and filling growth gaps in its large-capacity product segment.

4. 키옥시아(Kioxia)

키옥시아는 3분기 매출 6억 3,600만 달러를 기록하며 4위를 유지했습니다. 출하량은 증가했으나 고용량 제품 판매의 성장률은 경쟁업체들에 비해 다소 뒤처졌습니다. 이에 따라 키옥시아는 8TB 이하 SSD의 공급 부족을 활용해 북미 주요 고객사와의 파트너십을 강화하며 대용량 제품 부문에서의 성장 격차를 메우고자 했습니다.

Western Digital/SanDisk underwent a strategic restructuring by splitting its HDD and NAND/SSD businesses into two separately listed companies. This move aimed to increase operational agility and deepen collaborations with key North American customers. In Q3, Western Digital’s enterprise SSD business saw revenue surge over 100% QoQ to $332 million, driven by strong orders from North American clients.

5. 웨스턴디지털/샌디스크

웨스턴디지털은 HDD와 NAND/SSD 사업부를 두 개의 별도 상장 회사로 분리하는 전략적 구조조정을 단행했습니다. 이는 운영 민첩성을 높이고 북미 주요 고객사와의 협력을 강화하기 위한 조치입니다. 3분기 웨스턴디지털의 엔터프라이즈 SSD 사업 매출은 북미 고객사로부터의 강력한 주문에 힘입어 전 분기 대비 100% 이상 증가한 3억 3,200만 달러를 기록했습니다.

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| 마이크론 목표가 180달러-제이피 모건(2024.12.31) (2) | 2025.01.01 |

|---|---|

| NVLink와 PCIe 5.0의 차이점 (0) | 2024.12.31 |

| SK하이닉스,2025년 매출 81조원 (+23% YoY), 영업이익 31.1조원 (2024.12.30) (0) | 2024.12.30 |

| 머스크의 xAI(2024.12.29) (1) | 2024.12.29 |

| 마이크론과 SK하이닉스 차이점(2024.12.29) (5) | 2024.12.29 |