2022.07.07

요약:TrendForce 리서치에 따르면 8인치 공정(0.35~0.11μm 포함)의 공장 가동률이 가장 많이 떨어질 수 있습니다.

이러한 공정을 활용하는 제품은 주로 Driver IC, CIS, Power 관련 칩(PMIC, Power Discrete 등)입니다.

그러나 5G 스마트폰, 전기차 등 관련 애플리케이션의 보급률이 해마다 증가하고 있는 가운데

5G 기지국의 비축 모멘텀, 자동 보안 점검 등 각국의 인프라, 클라우드 서비스의 서버 수요가 지속적으로

가동률을 뒷받침해 파운드리 가동률은 대략 90% 이상일 것입니다.

Driver IC(디스플레이 구동 칩)

PMIC(전력관리 반도체)

CIS(이미지 센서)

Order Cancellations Strike, 8-inch Fab Capacity Utilization Rate Declines Most in 2H22, Says TrendForce

TrendForce에 따르면 주문 취소로 8인치 팹 가동률이 하반기에 가장 많이 감소할 것이다.

According to TrendForce investigations, foundries have seen a wave of order cancellations with the first of these revisions originating from large-size Driver IC and TDDI, which rely on mainstream 0.1Xμm and 55nm processes, respectively.

TrendForce 조사에 따르면, 파운드리 회사는 각각 주류 0.1Xμm 및 55nm 프로세스에 의존하는 대형 드라이버 IC 및

TDDI에서 시작된 이러한 수정의 첫 번째와 함께 주문 취소의 물결을 보았습니다.

Although products such as MCU and PMIC were previously in short supply, foundries’ capacity utilization rate remained roughly at full capacity through their adjustment of product mix.

MCU, PMIC 등의 제품은 이전에 공급이 부족했지만 파운드리의 가동률은 제품 믹스 조정을 통해

거의 완전 가동률을 유지했습니다.

However, a recent wave cancellations have emerged for PMIC, CIS, and certain MCU and SoC orders.

Although still dominated by consumer applications, foundries are beginning to feel the strain of the copious order cancellations from customers and capacity utilization rate has officially declined.

그러나 최근 PMIC, CIS 및 특정 MCU 및 SoC에 대한 주문취소가 나타났습니다.

여전히 소비자 애플리케이션이 지배하고 있지만 파운드리는 고객의 대량 주문 취소를 느끼기 시작했고

공장 가동률이 공식적으로 하락했습니다.

Looking at trends in 2H22, TrendForce indicates, in addition to no relief from the sustained downgrade of driver IC demand, inventory adjustment has begun for smartphones, PCs, and TV-related peripheral components such as SoCs, CIS, and PMICs, and companies are beginning to curtail their wafer input plans with foundries.

TrendForce는 2022년 하반기 추세를 살펴보면 드라이버 IC 수요의 지속적인 하락으로부터 탈출이 없을 뿐만 아니라

스마트폰, PC 및 SoC, CIS, PMIC와 같은 TV 관련 주변 부품에 대한 재고 조정이 시작되었으며

기업들이 파운드리와 함께 웨이퍼 투입 계획을 축소하기 시작했습니다.

This phenomenon of order cancellations is occurring simultaneously in 8-inch and 12-inch fabs at nodes including 0.1Xμm, 90/55nm, and 40/28nm. Not even the advanced 7/6nm processes are immune.

이러한 주문 취소 현상은 0.1Xμm, 90/55nm, 40/28nm를 포함한 공정의 8인치 및 12인치 팹에서 동시에 발생하고 있

습니다. 7/6nm같은 선단 공정도 예외는 아닙니다.

Capacity utilization rate unbound, resources effectively allocated, material mismatch issues eased

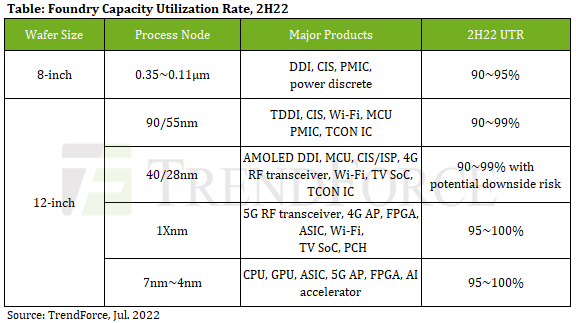

According to TrendForce research, the capacity utilization rate of eight-inch nodes (including 0.35-0.11μm) may decline the most. Products utilizing these processes are primarily Driver IC, CIS, and Power-related chips (PMIC, Power discrete, etc.).

TrendForce 리서치에 따르면 8인치 공정(0.35~0.11μm 포함)의 공장 가동률이 가장 많이 떨어질 수 있습니다.

이러한 공정을 활용하는 제품은 주로 Driver IC, CIS, Power 관련 칩(PMIC, Power Discrete 등)입니다.

Among these products, Driver IC has been directly impacted by cooling demand for TVs and PCs, reflected by the most severe downward revision of wafer inputs. At the same time, the supply of PMICs, which was still tight in 1H22, gradually achieved greater equilibrium after the redistribution of production capacity.

이 중 Driver IC(디스플레이 구동 칩)는 TV와 PC의 수요 약세에 직접적인 영향을 받았고, 웨이퍼 투입량 하향 조정이 가장 심했다. 동시에 22년 상반기에 여전히 타이트했던 PMIC(전력관리 반도체)의 수급은 생산능력 재분배 이후

점차 더 균형을 이루었다.

However, as demand continues to fall in 2H22, inventory adjustment has also begun for consumer PMICs and CISs.

그러나 하반기에도 수요 감소세가 지속되면서 소비자용 PMIC와 CIS도 재고 조정이 시작됐다.

Although there are still demand backstops for PMICs and power discrete originating from servers, automotive, and industrial applications, it is still difficult to make up the difference generated by driver IC, consumer PMICs and CISs order cancellations and the subsequent decline in the capacity utilization rate at some 8-inch fabs.

서버, 자동차 및 산업용 애플리케이션에서 발생하는 PMIC 및 전력 디스크리트에 대한 수요 백스톱이 여전히 존재하지만 드라이버 IC, 소비자 PMIC 및 CIS 주문 취소 및 이에 따른 용량 활용률 감소로 인해 발생하는 차이를 메우기는 여전히 어렵습니다.

TrendForce believes that the overall capacity utilization rate of 8-inch fabs will be roughly 90~95% in 2H22, while some fabs manufacturing a greater proportion of consumer applications may have to fight an uphill battle to maintain production capacity at 90%.

TrendForce는 8인치 팹의 전체 가동률이 2022년 하반기에 대략 90~95%가 될 것으로 보고 있으며,

소비자 애플리케이션 부문을 더 많이 제조하는 일부 팹은 생산 능력을 90%로 유지하기 위해

힘든 싸움을 해야 할 수도 있습니다.

The same situation has also occurred in mature 12-inch processes.

However, since 12-inch products are more diverse and their production cycle generally takes at least one quarter, coupled with upgrades to some product specifications, trends such as process transition have not been affected by broader short-term economic fluctuations.

성숙한 12인치 공정에서도 동일한 상황이 발생했습니다.

그러나 12인치 제품은 더 다양하고 생산 주기가 일반적으로 1분기 이상 소요되고 일부 제품 사양의 업그레이드가 결합되기 때문에 공정 전환과 같은 추세는 광범위한 단기적 경제 변동의 영향을 받지 않습니다.

As a result, overall production capacity utilization rate can still be maintained at a high operational watermark of approximately 95%. Compared with operating rates that easily hit 100% in the past two years, production line operation has gradually normalized and stabilized, demonstrating a steady balancing of resource allocation.

결과적으로 전체 생산 가동률은 여전히 약 95%의 높은 운영 워터마크로 유지될 수 있습니다.

지난 2년 간 쉽게 100%에 도달한 가동률과 비교하여 생산 라인 가동은 점차 정상화되고 안정화되어

자원 할당의 꾸준한 균형을 보여줍니다.

In terms of advanced processes, these are utilized primarily to produce CPU, GPU, ASIC, 5G AP, FPGA, AI accelerator, etc. Terminal applications remain dominated by smartphones and high-performance computing (HPC).

선단 공정 측면에서 이들은 주로 CPU, GPU, ASIC, 5G AP, FPGA, AI 가속기 등을 생산하는 데 사용됩니다.

터미널 애플리케이션은 스마트폰과 고성능 컴퓨팅(HPC)이 여전히 지배하고 있습니다.

Affected by the weak smartphone market, 5G APs have also experienced downward revisions of order volume but stocking momentum for HPC-related products remains stable.

5G AP 역시 스마트폰 시장 부진의 영향으로 주문량이 하향 조정을 받았지만

HPC 관련 제품의 재고 모멘텀은 안정적이다.

Coupled with plans to announce a number of new products, TrendForce believes that 7/6nm capacity utilization rate will decline marginally to 95~99% in 2H22 due to product mix conversion, while 5/4nm processes will remain near full load, driven by several new products.

여러 신제품을 발표할 계획과 함께 TrendForce는 제품 믹스 전환으로 인해 7/6nm 생산 가동률이 2H22에 95~99%로

소폭 하락할 것으로 보고 있으며, 반면에 5/4nm 공정은 몇 가지 신제품 생산으로 인해 완전 가동에 가깝게

유지될 것으로 예상합니다.

Looking forward to 2023, TrendForce believes, after nearly two and a half years of chip shortages, cooling of consumer product demand will ease the capacity utilization rate of wafer foundries in the short term and applications that were starved for chips in the past are now able to obtain a reallocation of resources.

TrendForce는 2023년까지 거의 2년 반 동안의 칩 부족 이후 소비재 수요 약세가 단기적으로 웨이퍼 파운드리의

가동률을 완화하고 과거에 칩이 부족했던 애플리케이션이 이제 생산이 가능하게 될 것이라고 믿습니다.

The penetration rate of related applications such as 5G smartphones and electric vehicles has increased year by year while the stocking momentum of 5G base stations, infrastructure in various countries including automated security inspection measures, and server demand from cloud services will continue to support the capacity utilization rate of foundries at a level roughly above 90%.

5G 스마트폰, 전기차 등 관련 애플리케이션의 보급률이 해마다 증가하고 있는 가운데 5G 기지국의 비축 모멘텀, 자동 보안 점검 등 각국의 인프라, 클라우드 서비스의 서버 수요가 지속적으로 가동률을 뒷받침해

파운드리 가동률은 대략 90% 이상일 것입니다.

However, some manufacturers that mainly produce consumer products may see capacity utilization rate fall below 90%. At this time, foundries must rely on their own internal diversified planning and resource allocation of product applications to overcome the inflationary crisis of component inventory adjustments.

그러나 소비자 제품을 주로 생산하는 일부 제조업체는 가동률이 90% 이하로 떨어지는 것을 볼 수 있습니다.

이때 파운드리는 부품 재고 조정의 증가하는 위기를 극복하기 위해 자체 내부의 다양한 계획 및 제품 애플리케이션의

자원 할당에 의존해야 합니다.

'파운드리-TSMC-난야-UMC-DB하이텍' 카테고리의 다른 글

| TSMC 2분기 주당 순이익 1.55달러 예상치 상회/ 투자액 감액(2022.07.15) (0) | 2022.07.15 |

|---|---|

| 디램 제조업체 난야는 2분기 매출이 전분기대비 9.6% 감소(2022.07.12) (0) | 2022.07.12 |

| 2022년 28나노이상 성숙 공정 파운드리 캐파 20% 증가(2022.06.23) (0) | 2022.06.24 |

| 대만 파운드리 공장 가동률은 3분기에 하락할 듯(2022.06.21) (0) | 2022.06.22 |

| TSMC의 2022년 매출은 30% 증가할 것(2022.06.09) (0) | 2022.06.09 |