2024.11.26

Server DRAM and HBM Boost 3Q24 DRAM Industry Revenue by 13.6% QoQ, Says TrendForce

서버 DRAM과 HBM이 2024년 3분기 DRAM 산업 매출을 전 분기 대비 13.6% 증가시켰다고 TrendForce가 발표했습니다.

TrendForce’s latest investigations reveal that the global DRAM industry revenue reached US$26.02 billion in 3Q24, marking a 13.6% QoQ increase.

TrendForce의 최신 조사에 따르면, 2024년 3분기 전 세계 DRAM 산업 매출은 전 분기 대비 13.6% 증가한 260억 2000만 달러를 기록했습니다.

The rise was driven by growing demand for DDR5 and HBM in data centers, despite a decline in LPDDR4 and DDR4 shipments due to inventory reduction by Chinese smartphone brands and capacity expansion by Chinese DRAM suppliers. ASPs continued their upward trend from the previous quarter, with contract prices rising by 8% to 13%, further supported by HBM’s displacement of conventional DRAM production.

DDR5와 HBM에 대한 데이터 센터 수요 증가가 주요 원인으로 작용했으며, 중국 스마트폰 브랜드의 재고 감소와 중국 DRAM 공급업체들의 생산 확대로 인해 LPDDR4 및 DDR4 출하량은 감소했습니다. 계약 가격은 전 분기 대비 8%에서 13% 상승했으며, HBM이 기존 DRAM 생산을 대체하면서 이러한 상승세를 더욱 뒷받침했습니다.

Looking ahead to 4Q24, TrendForce projects a QoQ increase in overall DRAM bit shipments. However, the capacity constraints caused by HBM production are expected to have a weaker-than-anticipated impact on pricing. Additionally, capacity expansions by Chinese suppliers may prompt PC OEMs and smartphone brands to aggressively deplete inventory to secure lower-priced DRAM products. As a result, contract prices for conventional DRAM and blended prices for conventional DRAM and HBM are expected to decline.

2024년 4분기를 전망하며, TrendForce는 전체 DRAM 비트 출하량이 전 분기 대비 증가할 것으로 예측하고 있습니다. 하지만 HBM 생산에 따른 용량 제약이 가격에 미치는 영향은 예상보다 약할 것으로 보입니다. 또한, 중국 공급업체들의 생산 확대로 인해 PC OEM 및 스마트폰 브랜드들이 저가 DRAM 제품을 확보하기 위해 공격적으로 재고를 소진할 가능성이 있습니다. 이에 따라 기존 DRAM과 HBM의 혼합 가격 및 기존 DRAM의 계약 가격은 하락할 것으로 예상됩니다.

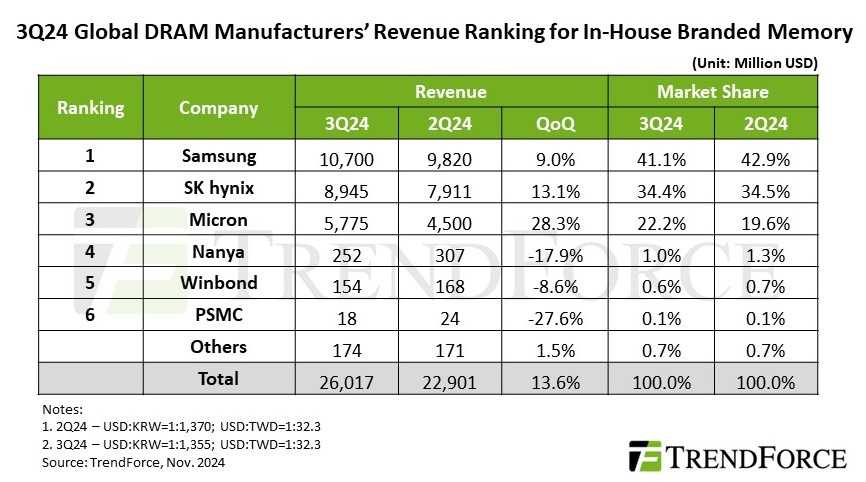

Server and PC DRAM contract price increases lifted revenues for the top three DRAM manufacturers. Samsung retained the top spot with revenue of $10.7 billion, up 9% QoQ. By strategic inventory clearing of LPDDR4 and DDR4, bit shipments remained flat compared to the previous quarter.

서버 및 PC DRAM 계약 가격 상승은 주요 DRAM 제조사들의 매출을 끌어올렸습니다. 삼성은 107억 달러의 매출로 전 분기 대비 9% 증가하며 1위를 유지했습니다. LPDDR4와 DDR4의 전략적 재고 정리를 통해 비트 출하량은 전 분기와 유사한 수준을 유지했습니다.

SK hynix reported $8.95 billion in revenue—a 13.1% QoQ increase—maintaining its second-place position. Although its HBM3e shipments ramped up, a 1%–3% QoQ decline in bit shipments from weaker LPDDR4 and DDR4 sales offset these gains.

SK하이닉스는 매출 89억 5000만 달러를 기록하며 2위 자리를 유지했으며, 이는 전 분기 대비 13.1% 증가한 수치입니다. HBM3e 출하량이 증가했지만 LPDDR4와 DDR4 판매 약세로 인해 비트 출하량은 전 분기 대비 1%에서 3% 감소했습니다.

Micron saw its revenue surge by 28.3% QoQ to $5.78 billion, driven by strong growth in server DRAM and HBM3e shipments, which led to a 13% QoQ increase in bit shipments.

마이크론은 서버 DRAM 및 HBM3e 출하량의 강력한 성장으로 인해 매출이 전 분기 대비 28.3% 증가한 57억 8000만 달러를 기록하며 비트 출하량도 13% 증가했습니다.

Taiwanese DRAM suppliers saw their revenues decline in 3Q24, falling significantly behind the top three manufacturers. Nanya Technology faced a more than 20% QoQ drop in bit shipments due to weaker consumer DRAM demand and intensified competition in the DDR4 market from Chinese suppliers. Its operating profit margin further deteriorated from -23.4% to -30.8%, reflecting losses from a power outage incident.

대만 DRAM 공급업체들의 매출은 3분기에 감소하며 상위 3개 제조사와의 격차가 더욱 커졌습니다. 난야 테크놀로지는 소비자용 DRAM 수요 약세와 중국 공급업체들의 DDR4 시장 경쟁 심화로 인해 비트 출하량이 전 분기 대비 20% 이상 감소했으며, 운영 이익률은 -23.4%에서 -30.8%로 더욱 악화되었습니다. 이는 정전 사고로 인한 손실을 반영한 결과입니다.

Winbond experienced an 8.6% QoQ decline in revenue, falling to $154 million, as consumer DRAM demand softened and bit shipments decreased. PSMC reported a 27.6% QoQ decline in revenue from its in-house consumer DRAM production. However, including foundry revenue, its total DRAM revenue rose 18% QoQ, driven by ongoing inventory replenishment from its foundry clients.

윈본드는 소비자용 DRAM 수요 약세와 비트 출하량 감소로 매출이 전 분기 대비 8.6% 감소한 1억 5400만 달러를 기록했습니다. PSMC는 자체 소비자용 DRAM 생산 매출이 전 분기 대비 27.6% 감소했으나, 파운드리 매출을 포함하면 전체 DRAM 매출은 전 분기 대비 18% 증가했으며, 이는 파운드리 고객들의 재고 보충 지속에 따른 결과입니다.

윈본드는 소비자용 DRAM 수요 약세와 비트 출하량 감소로 매출이 전 분기 대비 8.6% 감소한 1억 5400만 달러를 기록했습니다. PSMC는 자체 소비자용 DRAM 생산 매출이 전 분기 대비 27.6% 감소했으나, 파운드리 매출을 포함하면 전체 DRAM 매출은 전 분기 대비 18% 증가했으며, 이는 파운드리 고객들의 재고 보충 지속에 따른 결과입니다.

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| 델과 HP Inc., 실망스러운 PC 판매 실적 발표 후 주가 하락/2025년은 PC 교체시기 도래(2024.11.28) (2) | 2024.11.28 |

|---|---|

| 미국은 중국의 200개이상의 반도체에 HBM등 수출 금지 조치할 듯(2024.11.26) (2) | 2024.11.27 |

| 더 나은 인공지능(AI) 주식: 엔비디아 vs. 마이크론 테크놀로지(2024.11.15) (6) | 2024.11.16 |

| 주식을 ‘비싸게’ 만들지만 여전히 좋은 매수 기회가 될 수 있는 5가지 요인(2024.11.14) (4) | 2024.11.14 |

| 소프트뱅크의 자회사가 엔비디아 블랙웰 칩을 사용해 슈퍼컴퓨터를 구축할 계획(2024.11.14) (1) | 2024.11.14 |