2025.03.08

1 Artificial Intelligence (AI) Semiconductor Stock to Buy on the Dip Hand Over Fist Right Now (Hint: It's Not Nvidia or AMD)

"지금 당장 저가 매수해야 할 인공지능(AI) 반도체 주식 1종목 (힌트: 엔비디아나 AMD가 아닙니다)"

Chipsets known as graphics processing units (GPUs) are perhaps the most important hardware in generative AI development right now. For the last couple of years, investing in semiconductor stocks has generally been a great idea -- as you're nearly guaranteed some form of exposure to GPUs or data centers.

그래픽 처리 장치(GPU)로 알려진 칩셋은 현재 생성형 AI 개발에서 가장 중요한 하드웨어일 것입니다. 지난 몇 년 동안 반도체 주식에 투자하는 것은 전반적으로 좋은 선택이었는데, 이는 GPU나 데이터 센터와 같은 분야에 어느 정도 노출될 가능성이 거의 확실하기 때문입니다.

However, 2025 hasn't gotten off to the best start for chip stocks.

Whether it was drama brought on by Chinese start-up DeepSeek, U.S. President Donald Trump's new tariffs, or lofty investor expectations, many names in the chip realm haven't fared so well this year.

그러나 2025년은 반도체 주식에 있어 최상의 출발을 보이지 못했습니다.

중국 스타트업 DeepSeek의 등장, 미국 대통령 도널드 트럼프의 새로운 관세 정책, 혹은 과도한 투자자 기대 등 다양한 요인으로 인해 많은 반도체 기업들이 올해 들어 부진한 모습을 보였습니다.

From a macro perspective, the VanEck Semiconductor ETF has dropped 4% so far in 2025 (as of March 3). When it comes to specific companies, take Nvidia and Advanced Micro Devices, which have seen their stocks decline by 7% and 17%, respectively, so far this year.

거시적 관점에서 보면, VanEck 반도체 ETF는 2025년 들어 현재(3월 3일 기준)까지 4% 하락했습니다. 개별 기업을 살펴보면, 엔비디아와 AMD는 각각 7%, 17%의 주가 하락을 기록하며 어려움을 겪고 있습니다.

While many investors can't seem to look away from Nvidia or AMD, there's another stock that's been caught up in broader selling in the semiconductor landscape -- and I think it's worth buying the dip right now.

Let's explore why now looks like a lucrative opportunity to buy Taiwan Semiconductor Manufacturing (NYSE: TSM) stock hand over fist.

(hand over fist-->점점 더/ make money hand over fist-->점점 더 돈을 벌다)

많은 투자자들이 엔비디아나 AMD에서 눈을 떼지 못하고 있지만, 반도체 업계 전반적인 매도세에 휩싸인 또 다른 주식이 있습니다. 그리고 저는 지금이 그 주식을 저가 매수할 좋은 기회라고 생각합니다.

지금이야말로 대만 반도체 제조 기업 TSMC(NYSE: TSM) 주식을 적극적으로 매수해야 하는 이유를 살펴보겠습니다.

Don't underestimate Taiwan Semi's influence in the chip realm

When it comes to brand recognition in the chip market, investors don't need to look much further than Nvidia and AMD. These two juggernauts lead the charge in the GPU revolution. Meanwhile, Broadcom plays an integral role in outfitting data centers with advanced chipware, while Micron Technology's high bandwidth memory storage solutions are increasingly important as AI data workloads get bigger and more complex.

대만 반도체(TSMC)의 영향력을 과소평가하지 마세요

반도체 시장에서 브랜드 인지도를 따진다면, 투자자들은 엔비디아와 AMD만 봐도 충분할 것입니다.

이 두 거대한 기업은 GPU 혁명의 선두에서 질주하고 있습니다. 한편, 브로드컴은 데이터 센터에 첨단 칩웨어를 공급하는 데 핵심적인 역할을 하며, 마이크론 테크놀로지의 고대역폭 메모리 저장 솔루션은 AI 데이터 작업량이 더욱 크고 복잡해짐에 따라 점점 더 중요해지고 있습니다.

( 칩웨어(chipware)는 특정 기능을 수행하도록 설계된 집적 회로(IC) 또는 칩의 집합을 의미합니다.

일반적으로 하드웨어와 소프트웨어의 중간 개념으로, 특정 기능을 하드웨어적으로 구현한 칩과 그 칩을 구동하는

소프트웨어를 합쳐서 부르는 말입니다.)

With so many other names dominating headlines and talking points, I wouldn't be surprised if you aren't even aware of Taiwan Semi, or TSMC. The thing is that many leaders in the chip space -- including Nvidia, AMD, and Broadcom -- should credit Taiwan Semi for much of their success.

수많은 다른 기업들이 헤드라인을 장식하고 논의의 중심이 되고 있는 상황에서, 여러분이 대만 반도체(TSMC)에 대해 잘 모르고 있더라도 전혀 놀랍지 않습니다. 하지만 사실, 엔비디아, AMD, 브로드컴을 포함한 많은 반도체 업계 선두 기업들은 그들의 성공의 상당 부분을 TSMC에 돌려야 합니다.

TSMC specializes in foundry solutions, which is basically a fancy term that means it actually manufactures chips and integrated systems for semiconductor companies. In other words, without TSMC, Nvidia's chip architecture would be more of an idea than a tangible product.

TSMC는 파운드리(foundry) 솔루션을 전문으로 하는데, 이는 쉽게 말해 반도체 기업들을 위해 실제로 칩과 통합 시스템을 제조하는 역할을 한다는 뜻입니다. 다시 말해, TSMC가 없다면 엔비디아의 칩 아키텍처는 단순한 아이디어에 그칠 뿐, 실제 제품으로 구현되지 못할 것입니다.

Given how much demand there's been for GPUs over the last couple of years, it shouldn't come as a surprise that Taiwan Semi's revenue and profits are soaring. With that said, I think the company's growth is just beginning to kick into gear.

지난 2년간 GPU 수요가 폭발적으로 증가한 만큼, 대만 반도체(TSMC)의 매출과 이익이 급증하는 것도 당연한 일입니다. 하지만 저는 이 회사의 성장이 이제 막 본격적으로 시작되고 있다고 생각합니다.

Many of the "Magnificent Seven" companies, such as Microsoft, Amazon, Alphabet, and Meta Platforms, are exploring custom silicon as a strategy to migrate from an overreliance on Nvidia's chipware. These big tech giants, as well as ChatGPT maker OpenAI, are reportedly collaborating with TSMC to help bring their visions to life.

마이크로소프트, 아마존, 알파벳, 메타 플랫폼과 같은 ‘매그니피센트 세븐(Magnificent Seven)’ 기업들 중 다수는 엔비디아의 반도체 기술에 대한 의존도를 줄이기 위한 전략으로 맞춤형(커스텀) 반도체 개발을 모색하고 있습니다.

이러한 빅테크 기업들뿐만 아니라 ChatGPT 개발사인 오픈AI(OpenAI) 역시 자신들의 비전을 실현하기 위해 TSMC와 협력하고 있는 것으로 알려졌습니다.

Although TSMC has already acquired nearly two-thirds of the foundry market opportunity, I think the advent of more custom silicon -- in addition to new architectures from Nvidia and AMD over the next couple of years -- will further strengthen the company's leadership position and lead to a prolonged phase of revenue and profit acceleration.

TSMC는 이미 파운드리 시장의 거의 3분의 2를 차지하고 있지만, 저는 맞춤형(커스텀) 반도체의 확산과 함께 향후 2년간 엔비디아와 AMD의 새로운 아키텍처 출시가 TSMC의 시장 지배력을 더욱 강화할 것으로 생각합니다.

이는 TSMC의 매출과 이익이 장기간 가속 성장하는 계기가 될 것입니다.

TSMC shares are priced to perfection

Despite TSMC's strong market position and robust financial outlook, shares of the chip stock are shockingly cheap.

TSMC 주가는 완벽한 가치를 반영하고 있는가?

TSMC가 강력한 시장 지위와 탄탄한 재무 전망을 가지고 있음에도 불구하고, 이 반도체 주식의 주가는 놀라울 정도로 저평가되어 있습니다.

Right now, the average forward price-to-earnings (P/E) multiple for the S&P 500 is about 21. As the chart above illustrates, Taiwan Semi's forward P/E is roughly 19. To me, this disparity suggests that investors may see an investment in the S&P 500 as less risky than TSMC -- and one that potentially carries more upside, too.

현재 S&P 500 지수의 평균 선행 주가수익비율(P/E)은 약 21배 수준입니다. 위 차트에서 볼 수 있듯이,

대만 반도체(TSMC)의 선행 P/E는 약 19배에 불과합니다.

저는 이 격차가 투자자들이 S&P 500 투자에 대해 TSMC보다 낮은 위험을 느끼고 있으며,

더 높은 상승 가능성이 있다고 평가하고 있다는 의미로 해석할 수 있다고 생각합니다.

In my eyes, the two main risks revolving around an investment in TSMC are the following:

- The semiconductor industry being cyclical.

- Geopolitical tensions between China and Taiwan.

제 관점에서 TSMC 투자와 관련된 두 가지 주요 리스크는 다음과 같습니다.

- 반도체 산업의 경기 순환성

- 중국과 대만 간의 지정학적 긴장

While I can understand those points in an academic sense, I think any fears around those topics are overblown.

Chip demand isn't expected to slow down anytime soon, as the market is forecast to increase tenfold over the next decade and reach a size of nearly $1 trillion.

이러한 우려가 학문적으로 이해는 되지만, 저는 그 걱정들이 과장되었다고 생각합니다.

반도체 수요는 향후 감소할 가능성이 거의 없으며, 오히려 향후 10년 동안 시장 규모가 10배 성장해 거의 1조 달러에 이를 것으로 전망됩니다.

On top of that, TSMC's operations are not exclusive to Taiwan. In fact, the company just announced in early March that it will be investing an additional $100 billion to expand its manufacturing footprint in the U.S. This seems like a logical decision given big tech is planning to spend more than $300 billion in AI infrastructure in 2025 alone.

게다가 TSMC의 생산 거점은 대만에만 국한되지 않습니다. 실제로, TSMC는 올해 3월 초 미국 내 생산시설 확장을 위해 추가로 1,000억 달러(약 130조 원)를 투자할 계획이라고 발표했습니다. 이는 2025년 한 해 동안 빅테크 기업들이 AI 인프라 구축에 3,000억 달러(약 400조 원) 이상을 지출할 예정이라는 점을 고려할 때, 매우 합리적인 결정으로 보입니다.

I think TSMC stock is a bargain right now. Long-term investors may want to consider buying this stock hand over fist, before the company's manufacturing operation witnesses even further scale as the AI revolution continues to move full steam ahead.

저는 TSMC 주식이 지금 매우 저평가된 상태라고 생각합니다.

장기 투자자라면, AI 혁명이 본격적으로 가속화되기 전에 TSMC의 제조 역량이 더욱 확장되기 전에 적극적으로 매수하는 것을 고려해볼 만합니다.

--------------------------

2025.03.08

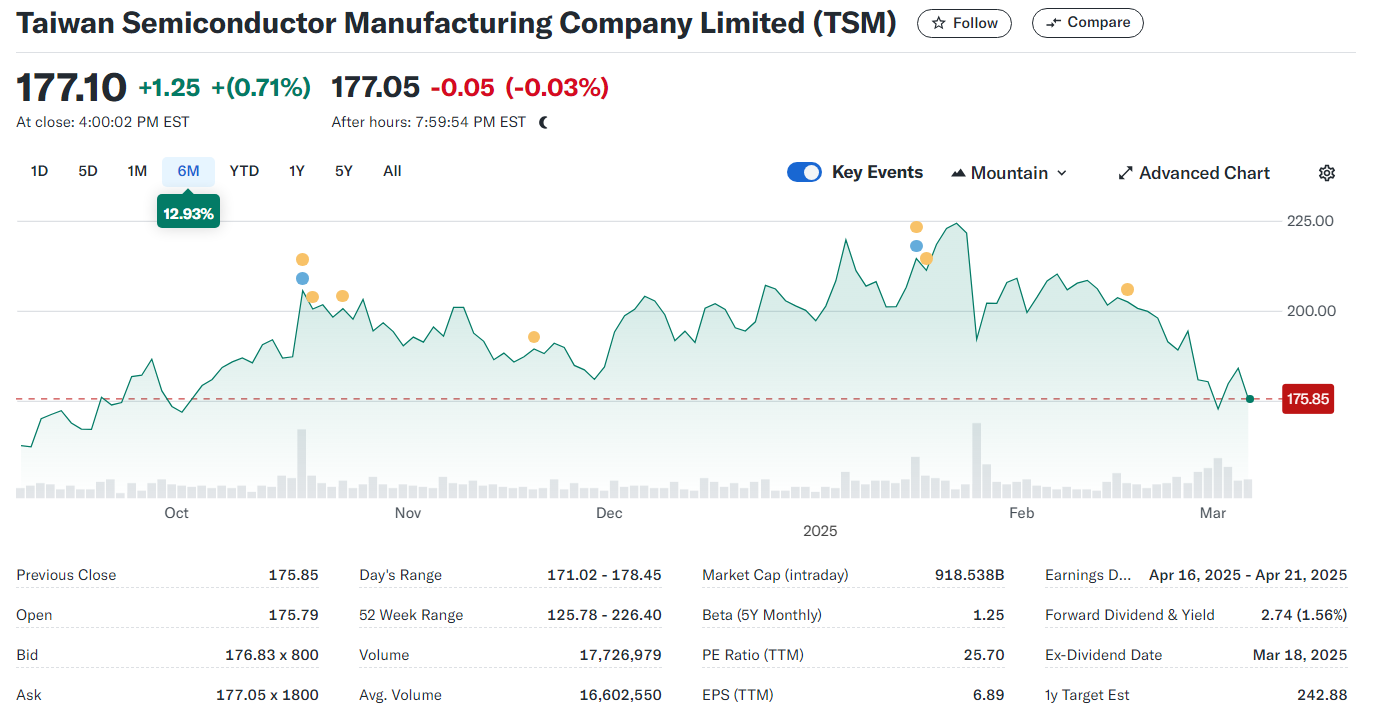

1.다음은 TSMC의 6개월 챠트.

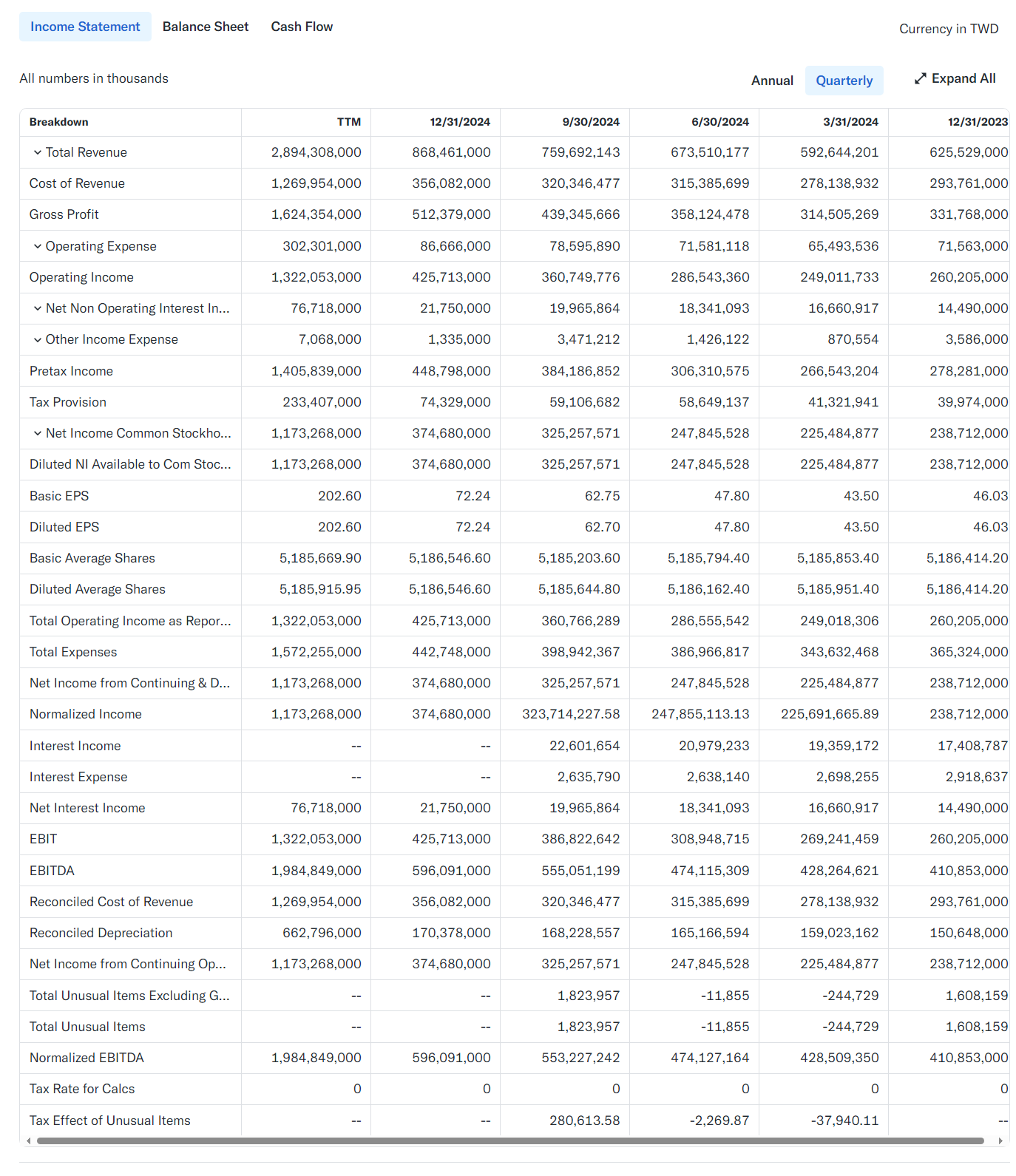

2.다음은 TSMC의 연간 및 분기 손익 계산서

단위는 대만 달러

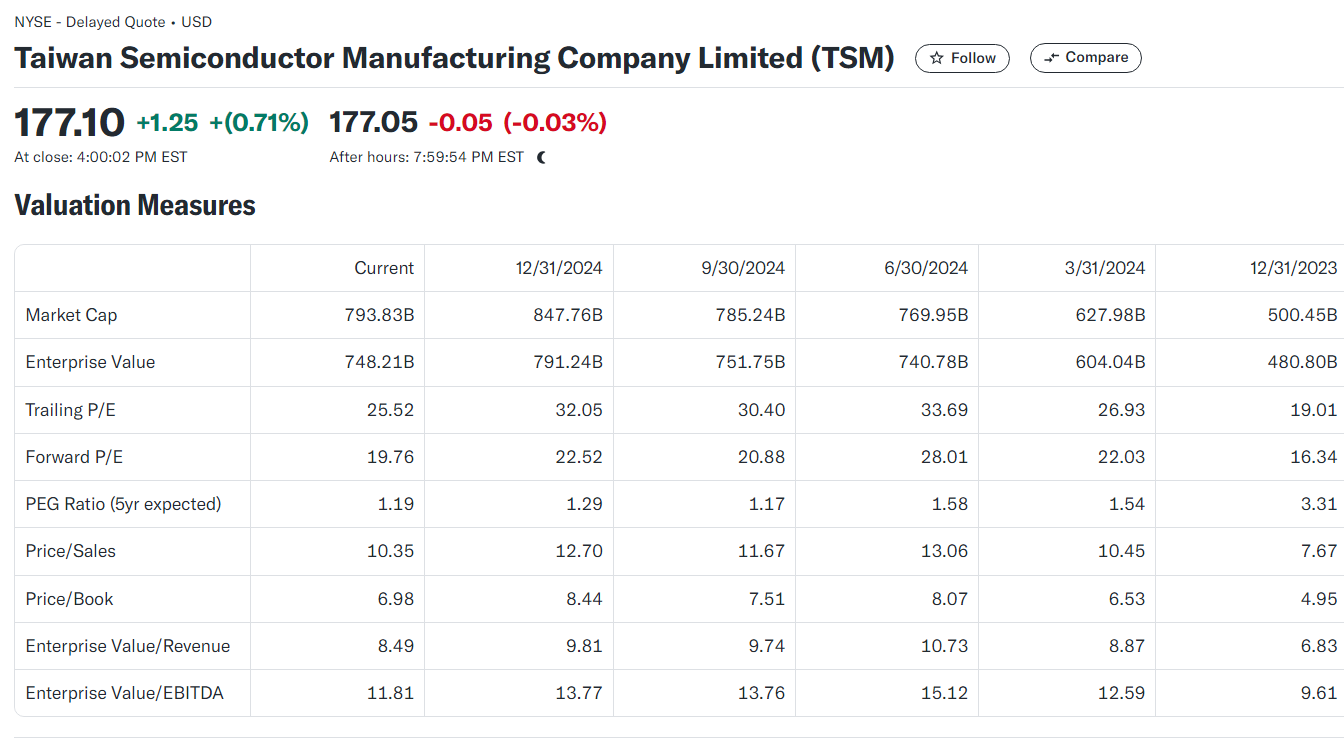

3.다음은 밸류에이션 지표.

단위는 미국 달러

2025년3월7일 현재 TSMC의 주가는 177.10달러이고, 예상 순이익 대비 PER는 19.76배,

BPS(주당 순자산)은 6.98달러로 PBR은 25배입니다.

참고로 지난 3월6일 씨티그룹이 발표한 한국의 SK하이닉스의 목표가는 기존 PBR 1.9배에 30% 프리미엄을 준

2.5배를 적용하여 34만원으로 설정했습니다.

즉 주문을 받아 생산하는 TSMC같은 파운드리 회사는 재고 걱정이 없으므로 더 높은 배수의 PBR을 적용하고,

하이닉스같은 메모리 반도체 회사는 단일 상품을 생산하여 공급하는 구조이므로 공급과 수요에 따라,

주가가 요동치는 시클리컬 산업으로 더 낮은 배수의 PBR을 적용하게 됩니다.

그래서 한국의 애널리스트들은 하이닉스나 삼성전자의 목표가를 설정할 때 보통 주당 순자산(BPS)의

2배를 적용합니다.

하지만 올해 하반기에 HBM4의 샘플이 나오고.2026년부터 양산이 시작된다면 하이닉스의

PBR도 더 높게 적용되야 합니다. HMM4는 커스터마이즈(고객의 주문에 따라 생산) 상품이고,

주문 물량 만큼만 생산하므로 재고 걱정이 없어지게 됩니다.

그러면 하이닉스의 매출의 일부는 TSMC와 같은 파운드리 회사의 기능도 갖게 됩니다.

씨티 그룹이 하이닉스의 PBR 2.5배를 적용한 이유도 이런 이유도 있을 것입니다.

물론 씨티그룹은 하이닉스가 HBM 선두 주자임을 감안했다고 합니다.

향후 HBM4가 양산으로 주력 상품이 된다면 SK하이닉스의 PBR이 5배~10배 적용되는 것이

이상하지 않은 날이 오기를 기대해 봅니다.

'파운드리-TSMC-난야-UMC-DB하이텍' 카테고리의 다른 글

| TSMC, 4분기 매출 37.6조원, 순이익 16.2조원 달성(2025.01.16) (1) | 2025.01.16 |

|---|---|

| TSMC,2024년3분기 실적 발표(2024.10.17) (6) | 2024.10.17 |

| TSMC,3분기 이익 40% 급증할 듯 (2) | 2024.10.14 |

| TSMC 매출은 AI 칩 수요가 견조함을 보여주며 예상치 상회(2024.10.09) (1) | 2024.10.09 |

| AI 배포 및 높은 재고 수준에서의 공급망 회복이 웨이퍼 파운드리 시장 가치를 2025년까지 연간 20% 성장으로 이끌 것(2024.09.19) (4) | 2024.09.20 |