2021.12.27

매출 총이익은 매출에서 매출원가(원료비, 공장운영비등)를 제외한 금액이다.

영업이익은 매출총이익에서 영업비용(사무실 인건비,광고비등)을 제외한 금액이다.

Micron Stock: My Best Idea For 2022 (NASDAQ:MU) | Seeking Alpha

Summary

- Micron's revenue growth slowed in FQ1’22.

- Micron already guided for weaker sales growth in the previous quarter, so the slowdown was expected.

- 2022 could be a year of strong growth for Micron, if DRAM ASPs bounce back.

- With a P-E ratio of 8X, Micron is a semiconductor bargain.

마이크론의 매출 성장은 FQ1'22에 둔화되었습니다.

마이크론은 이미 지난 분기 매출 성장 둔화를 예상했기 때문에, 둔화될것은 예상되었습니다.

DRAM ASP가 반등한다면 2022년은 Micron에게 강력한 성장의 해가 될 수 있습니다.

PER 8배에 거래되는 Micron은 반도체 주식치고는 싼 주식입니다.

Micron Technology (MU) is my top investment idea for 2022. While revenue growth slowed down in the last quarter, the memory chip maker continued to report strong gross margins.

Given the potential for revenue and gross margin growth in 2022, Micron's valuation is unjustifiably low!

Micron Technology(MU)는 2022년 최고의 투자 아이디어입니다. 지난 분기에 매출 성장이 둔화되었지만,

메모리 칩 제조업체는 계속해서 강력한 매출총이익을 보고했습니다.

2022년 매출과 매출총이익 성장의 잠재력을 감안할 때 Micron의 평가는 부당하게 낮습니다!

Financial performance FQ1'22

Before I go into the actual results Micron submitted for its first quarter, here is the firm's guidance for FQ1'22: Micron projected revenues of $7.65B +/- $200 million and a gross margin of 47% +/- 1 PP.

Based off of low-case estimates, I expected Micron to generate at least $3,427M in gross margins for the last quarter.

재무 실적 FQ1'22

Micron이 1분기에 제출한 실제 결과를 살펴보기 전에, FQ1'22에 대한 회사의 전망치가 있었습니다.

마이크론은 매출 76.5억달러(플마 2억달러)와 매출총이익률 47%(플마 1%)를 전망했었다.

낮은 경우의 매출 추정치를 바탕으로 저는 Micron이 지난 분기 매출총이익으로 최소 3,427백만 달러를

창출할 것으로 예상했습니다.

Micron's projections proved to be very accurate. The memory chip maker submitted its earnings card

for FQ1'22 a week ago and it showed $7,687M in revenues and a gross margin of $3,616M.

Micron의 예측은 매우 정확한 것으로 판명되었습니다. 메모리 칩 제조업체는 일주일 전 FQ1'22에 대한 실적 카드를

제출했으며 $7,687M의 매출과 $3,616M의 매출총이익을 보여주었습니다.

Revenues grew at a rate of 33% year over year while Micron's gross margin, in dollars,

more than doubled compared to the year-earlier period.

On $7.7B in revenues, Micron generated a gross margin of 47% which was down 0.9 PP from FQ4'21 (47.9%), but up 16.1 PP from FQ1-21 (30.9%). The increase in Micron's gross margins is attributable to broad-based strength in end-markets, accelerating demand for memory and storage products and high average selling prices for Micron's DRAM and NAND products.

매출은 전년 대비 33%의 속도로 성장했으며 Micron의 매출총이익(달러)은 전년 동기에 비해 두 배 이상 증가했습니다.

77억 달러의 매출에서 Micron은 FQ4'21(47.9%)보다 0.9PP 감소한 47%의 총 마진을 생성했지만

FQ1-21(30.9%)보다 16.1PP 상승했습니다. Micron의 매출총이익 증가는 최종 시장의 광범위한 강점, 메모리 및

스토리지 제품에 대한 수요 가속화, Micron의 DRAM 및 NAND 제품에 대한 높은 평균 판매 가격에 기인합니다.

Based on Micron's new outlook for FQ2'22, the firm expects revenues of $7.5B +/- $200M and a gross margin of 46% +/- 1 PP. The forecast implies a 3% quarter-over-quarter drop in revenues and a 1 PP decline in gross margins. In the low case, I expect Micron to generate a gross margin of at least $3,285M.

| in mil $ | Guidance FQ2-22 | FQ1-22 | FQ4-21 | FQ3-21 | FQ2-21 | FQ1-21 |

| Revenues | $7.5 billion ± $200 million | $7,687 | $8,274 | $7,422 | $6,236 | $5,773 |

| Gross Margins | Minimum $3,285 | $3,616 | $3,964 | $3,185 | $2,054 | $1,784 |

| Gross Margins (%) | 46.0% ± 1% | 47.0% | 47.9% | 42.9% | 32.9% | 30.9% |

(Source: Author)

Micron generated 73% of revenues from its DRAM business and 24% from its NAND business in the first quarter. The share of DRAM revenue contributions dropped only 1 PP quarter over quarter as the DRAM business continued to show end-market strength. Because Micron faces stronger growth prospects in the NAND business than in the DRAM business, longer term, I see the share of Micron's NAND revenues grow to 30% or higher in the future.

(Source: Micron)

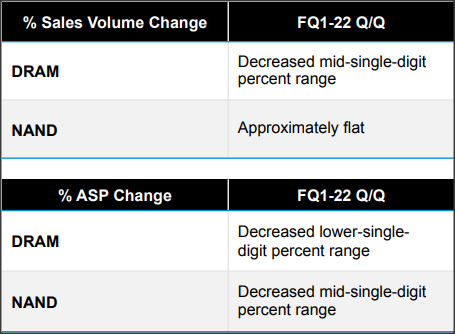

Declining ASPs are a challenge heading into 2022

In FQ3'21, average selling prices for DRAMs soared 20% quarter over quarter due to strong demand and a shortage of DRAM products in the market. ASP growth started to moderate in FQ4'21 and it further softened in FQ1'22. Both DRAM and NAND average selling prices declined in the low- to mid-single digit range in the last quarter due to an easing supply shortage of memory products.

(Source: Micron)

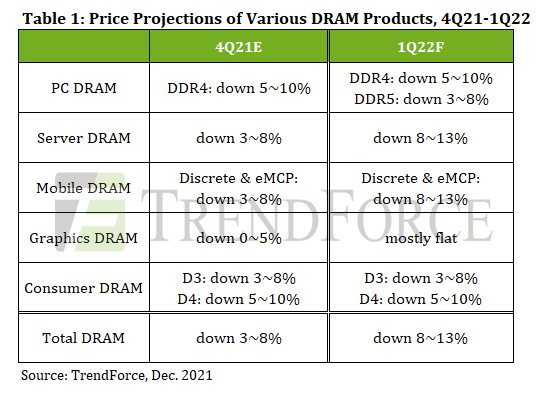

The short-term outlook for DRAM prices is negative, but chiefly because of seasonal factors. I believe DRAM prices will rebound after Q1'22 as seasonal factors subside and demand returns to memory chip makers. TrendForce previously said that DRAM prices could rally in the second half of 2022 as seasonal demand is expected to return at this time.

DRAM 가격에 대한 단기 전망은 부정적이지만 주로 계절적 요인 때문입니다.

DRAM 가격은 22년 1분기 이후에 계절적 요인이 진정되고 메모리 칩 업체에 대한 수요가 회복되면서

반등할 것으로 본다.

TrendForce는 이전에 이 시기에 계절적 수요가 회복될 것으로 예상됨에 따라

DRAM 가격이 2022년 하반기에 상승할 수 있다고 말했습니다.

(Source: TrendForce)

The decrease in product pricing sets up a challenge for Micron heading into 2022 and I believe declining ASP strength is the biggest risk to Micron's gross margins. Micron's gross margin expansion in FY 2021 was significant and it was chiefly driven by a DRAM supply shortage and improved pricing for DRAM products. If DRAM prices fail to rebound after the first quarter 2022, Micron's gross margins may come under additional pressure. Slowing revenue growth and weaker performance in the DRAM business pose serious risks for Micron's stock. If Micron's revenue growth slows down materially in 2022, shares of the memory chip maker may revalue lower.

제품 가격 하락은 2022년으로 향하는 Micron에 대한 도전과제이며, 저는 ASP 강세가 Micron의 총 마진에 가장 큰 위험이라고 생각합니다. 2021 회계연도에 Micron의 총 마진 확장은 상당했으며 주로 DRAM 공급 부족과 DRAM 제품 가격 개선이 주도했습니다. 2022년 1분기 이후 DRAM 가격이 반등하지 않으면 Micron의 총 마진이 추가 압박을 받을 수 있습니다. DRAM 사업의 매출 성장 둔화와 실적 악화는 Micron의 주식에 심각한 위험을 초래합니다.

2022년 Micron의 매출 성장이 크게 둔화되면 메모리 칩 제조업체의 주가는 더 낮게 재평가될 수 있습니다.

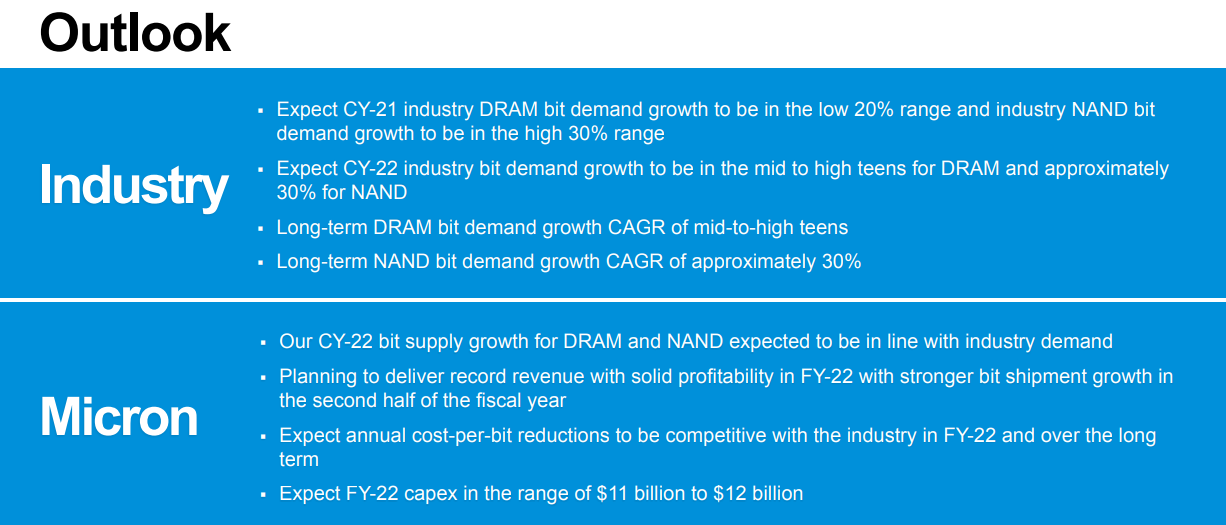

Micron's market outlook for the DRAM and NAND industries

Micron expects strong bit demand growth in both of its core segments, DRAM and NAND, in 2022 which should support pricing. Micron forecasts industry bit demand growth to be in the mid to high teens for DRAM while NAND bit demand growth in the industry is expected at 30% in 2022. Micron's short- and long-term outlooks on the DRAM and NAND markets are consistent, with growth rates in the NAND market also expected to outpace growth in the DRAM market in the long term. This is also the reason why I expect Micron to grow the revenue share from NAND sales significantly in FY 2022 and beyond.

Micron은 2022년에 핵심 부문인 DRAM과 NAND 모두에서 강력한 비트 수요 성장을 예상하여 가격 책정을 뒷받침해야 합니다. Micron은 DRAM에 대한 업계 비트 수요 성장이 10대 중후반이 될 것으로 예측하는 반면 업계의 NAND 비트 수요 성장은 2022년에 30%가 될 것으로 예상합니다. DRAM 및 NAND 시장에 대한 Micron의 장단기 전망은 일관성이 있습니다. NAND 시장의 성장률도 장기적으로 DRAM 시장의 성장률을 능가할 것으로 예상됩니다. 이것이 내가 Micron이 FY 2022 및 그 이후에 NAND 판매로 인한 수익 점유율을 크게 증가시킬 것으로 기대하는 이유이기도 합니다.

(Source: Micron)

Valuation of Micron

Micron's earnings growth is materially undervalued even when considering the sequential drop in ASPs.

Micron is projected to generate $8.84 in profits in FY 2022 and $11.41 in FY 2023.

Based off of $11.41 in FY 2023 profits, implying 29% year over year earnings growth,

Micron's price-to-earnings ratio is 8X.

마이크론의 주당순이익은 2022년 8.84달러, 2023년 11.41달러로 예상된다.

이는 연율 29%의 성장을 의미하며, 2023년 주당 순이익 기준으로 지금 주가는 PER 8배에 불과하다.

| FY 2022 | FY 2023 | FY 2024 | |

| EPS | $8.84 | $11.41 | $11.98 |

| YoY Growth | 45.90% | 29.10% | 4.95% |

| P-E Ratio | 10.68X | 8.27X | 7.88X |

(Source: Author)

Final thoughts 최종 판단

Heading into 2022, I believe Micron has a lot of potential to grow its business and

DRAM ASPs may rise again after a seasonal drop in the first quarter 2022.

Micron's gross margins in FQ1'22 remained strong despite weaker ASPs. Because end-markets are likely to remain strong in FY 2022, based off of Micron's expectations for industry DRAM and NAND bit demand growth, Micron is a top bet on the continual expansion of the current semiconductor growth cycle!

2022년에 들어가면서, Micron은 사업을 성장시킬 수 있는 많은 잠재력을 가지고 있으며

DRAM ASP는 2022년 1분기의 계절적 하락 이후 다시 상승할 수 있다고 생각합니다.

FQ1'22의 매출 총이익은 낮은 평균 판매 가격에도 불구하고 강세를 유지했습니다.

업계 DRAM 및 NAND 비트 수요 성장에 대한 Micron의 기대에 기반하여 2022 회계연도에도 최종 시장이 강세를

유지할 가능성이 높기 때문에 Micron은 현재 반도체 성장 주기의 지속적인 확장에 대한 최고의 베팅입니다!

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| Micron, 중국 시안 봉쇄로 인한 DRAM 칩 공급 지연 (2021.12.29) (0) | 2021.12.30 |

|---|---|

| 중국 시안(西安)의 코로나19 상황과 관련해 말씀드립니다 (0) | 2021.12.29 |

| 8인치 자동차용 반도체 공급은 2025년까지 부족(2021.12.28) (1) | 2021.12.28 |

| 마이크론은 더 많이 상승할 것(2021.12.25) (0) | 2021.12.26 |

| 2022년 서버 출하량은 4~5% 증가할 것(2021.12.21) (0) | 2021.12.26 |