위그래프는 디램 빗그로스 20%달성을 위해 필요한 적정 투자금액(푸른색)과 실제로 투자된 금액(붉은색)을

표시한 그래프. 2019년도 적정 캐펙스는 200억달러인데 여기에 못미치는 170억달러가 투자될 것임.

이는 2020년 디램 공급 부족을 심화 시킬 것.

2019.05.27 Robert Castellano

https://seekingalpha.com/article/4251198-semiconductor-equipment-revenues-drop-

17-percent-2019-29-percent-capex-spend-cuts

Semiconductor Equipment Revenues To Drop 17% In 2019 on 29% Capex Spend Cuts

2019년 장비 업체 매출은 반도체회사들의 전년대비 캐펙스 29% 감소로 17% 감소할 것.

Summary

As memory companies curb capex spend in 2019, revenue of semiconductor equipment companies is forecast to drop from 37% in 2018 to -17% in 2019.

2019년 메모리 업체들의 캐펙스 감축으로, 반도체 장비업체들의 매출은 2018년 37%증가한후

2019년에는 전년대비 17% 감소할 것.

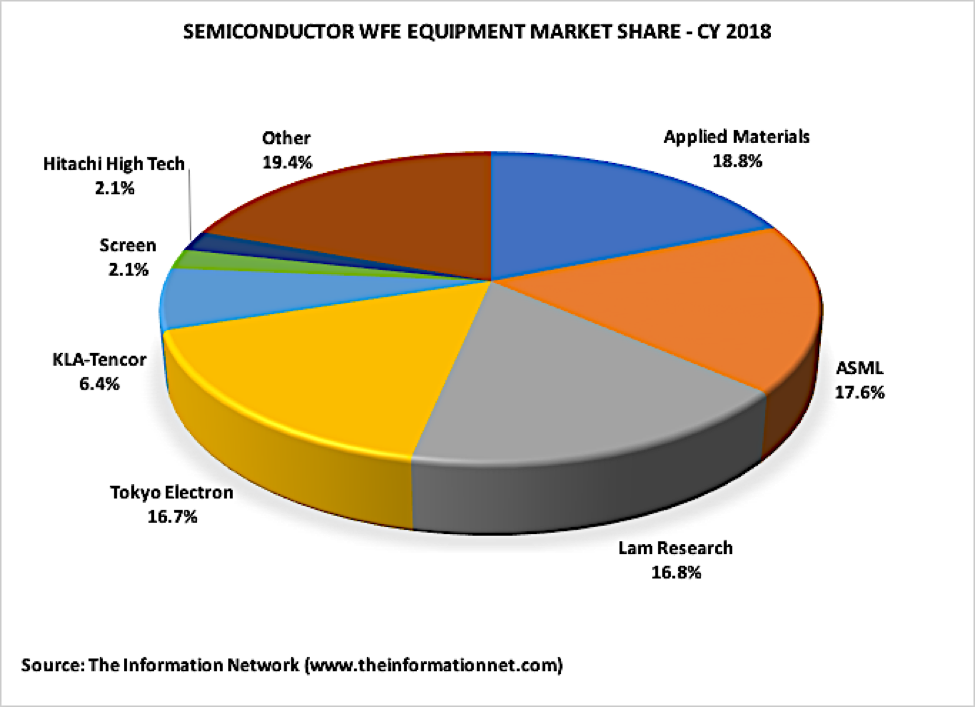

Applied Materials led the equipment market in 2018, but its market share dropped from 21.2% in 2017 to 18.8% as revenues increased only 1.1% YoY.

Billings of Japanese equipment suppliers are down 4.5% YoY for the first two months of 2019, while billings of North American equipment suppliers are down 21.5% in the same period.

2019년 첫 2개월간 일본 장비업체의 매출은 전년대비 4.5% 하락했지만, 북미 장비업체의 매출은

21.5% 감소했다.

The semiconductor equipment market grew 37.3% in 2017 on the heels of capex spend by memory companies in order to increase bit capacity and move to more sophisticated products with smaller nanometer dimensions.

2017년 반도체 장비업체들의 매출은 전년대비 37.3% 증가했다. 이는 메모리 회사들이 빗 용량 증가와

미세공정으로 전환하기위하여 캐펙스가 증가했기 때문이다.

Unfortunately these companies overspent resulting in excessive oversupply of memory chips.

불행히도 이들 회사들의 과다 장비투자는 메모리 칩의 공급과잉을 초래했다.

아래 표는 2017년과 2018년 낸드의 과잉투자를 보여준다.

푸른 색은 적정 투자 금액이고 붉은 색은 실제로 투자된 금액이다.

단위는 십억 달러

As memory prices started dropping, these companies put a halt to capex spend, and global equipment revenues increased only 13.9% in 2018. As excess inventory continues to increase in 2019, capex spend by these companies is projected to drop 29%, which will result in a significant reduction in equipment revenues in 2019.

메모리 가격이 하락하기 시작했기때문에 장비투자를 중단했고, 2018년 장비회사의 매출은

겨우 13.9%증가했다. 과잉 재고는 2019년에 지속적으로 증가하면서, 2019년 장비투자는

전년대비 29% 감소할 것으로 예상되며 이는 2019년 장비업체들의 심각한 매출 감소로 이어질 것.

As a result, the global semiconductor equipment market is forecast to drop 17% in 2019, reaching revenues of $64.5 billion, according to The Information Network’s report, "Global Semiconductor Equipment: Markets, Market Shares, Market Forecasts."

'인포메이션 네트워크'의 보고서에 따르면 2019년 글로벌 장비업체의 매출은 전년대비 17%

감소한 645억달러에 달할것으로 예상.

To analyze the equipment market in 2019, we need to look at revenues and market shares for previous years. For 2018, Applied Materials (AMAT) ended the year with a market share of 18.8%, down from 21.2% in 2017, as shown in Chart 1. Fellow U.S. supplier Lam Research (LRCX) held a 16.8% share in 2018, down from 16.9% in 2017.

2019년 반도체 장비 시장을 분석하려면 전년도의 매출과 점유율을 살펴볼 필요가 있다.

2018년 '어플라이드 머티리얼스'는 점유율이 2017년 21.2%에서 18.8%로 하락했다.

'램리서치'는 16.9%에서 16.8%로 하락했다.

apanese supplier Tokyo Electron Ltd. (OTCPK:TOELY), a major competitor of AMAT and LRCX in the deposition and etch sectors, held a 16.7% share in 2018, an increase of 1.6 points from a 15.1% share in 2017.

일본의 토쿄일렉트론은 AMAT와는 디포지션분야에서, 램리서치와는 에칭분야에서 주요 경쟁자인데,

지난 2018년 시장점유율은 16.7%로 2017년 점유율 15.1%에서 1.6포인트 증가했다.

Chart 2 illustrates the change in revenue YoY for the leading semiconductor equipment companies. As I said above, the overall market increased 13.9%, so Lam’s growth of 13.7% attributed to its 0.1 point loss in share. AMAT’s lackluster growth of only 1.1% in 2018 contributed to its loss of 1.6 share points. Growth was less than the composite growth of companies ranked 8 through 75. The company has been losing market share to competitors YoY for the past three years.

아래의 챠트2는 반도체 장비 업체들의 2017년대비 2018년 매출 증가율을 표시한 것이다.

KLA-Tencor (KLAC) grew 26.1%. I noted in a January 31 Seeking Alpha article entitled “KLA-Tencor And Metrology/Inspection Peers Will Be Less Impacted By Memory Capex Cuts Than The Rest Of The Equipment Industry In 2019” that a shift to more inspection in the fab was underway.

AMAT sells equipment for nearly all the processes used to make a semiconductor chip. Its two major segments are deposition and etch. In 2015-2017, deposition made up 46% of AMAT’s revenue, while etch made up 18-20% of revenues. These two sectors represent 2/3rd of the company's revenues.

In 2018, the deposition market grew 3.9% and etch grew 4.4%. Since AMAT’s total revenues grew just 1.1%, it is obvious that the company lost shares in both sectors to competitors in these sectors, namely Lam Research, Tokyo Electron, and Hitachi High Technologies (OTC:HICTF).

2019 Analysis

Based on capex spend data as detailed in Table 1, The Information Network projects the semiconductor equipment market will drop 17% in 2019,

compared to growth of 13.9% in 2018.

Chart 3 shows equipment billings for North American equipment suppliers from 2015 through February 2019. Note the red arrow to highlight 2019 billings. For the first two months, 2019 billings appear to track seasonally with 2015 and 2016, but are down 21.5% YoY from 2018.

챠트3은 북미 반도체 장비업체들의 2015년부터 2019년2월까지 매출액이다.

Chart 4 shows billings for Japanese equipment suppliers for the same period. Billings data for 2019, highlighted by the red arrow, shows no seasonality.

챠트4는 일본장비 업체들의 같은 기간 장비 판매액이다.

2019년 장비 판매액은 (빨간 화살표가 가리키는 곳) 계절적 효과를 못본 것으로 보인다.

Unlike North American companies, billings are down only 4.5% YoY from 2018.

미국 장비업체와는 달리 일본 장비 매출액이 2018년대비 4.5% 하락한 것을 볼수있다.

To better differentiate between North American and Japanese equipment companies, I’ve plotted billings for the past 14 months between January 2018 and February 2019, as show in Chart 5.

For North American companies, we can see an increase in billings for Q2 followed by a successive MoM decline. There is another bump in December 2018, but that is attributed to revenue pull-in by companies to boost revenues prior to the end of the CY. As was illustrated in Chart 3, this boost occurred every December for each of the four years plotted.

For Japanese companies, there were double peaks in Q2 and into Q4 2018, which resulted in market share gains for Japanese companies over North American companies. I expect a boost in billings in March (similar to the December bump by NA companies) because Japan ends its fiscal year in the month - so we can see the same billing bump in March of each year, as was illustrated in Chart 4.

Investor Takeaway

The U.S. dollar appreciated only 1.5% over the Japanese yen in 2018 versus 2017, so currency is not a factor in the marked difference in revenues between North American versus Japanese equipment companies.

Also, customer base is not a factor. For example, Tokyo Electron’s revenues from South Korea in CY Q1 2018 were 37% and dropped to 25% in Q4 2018 because of cuts in capex spend by memory suppliers Samsung Electronics (OTC:SSNLF) and SK Hynix (OTC:HXSCL). Lam Research’s revenues from South Korea were 36% and 25%, respectively, for the same period.

While there is no clear-cut reason why Japanese equipment companies achieved significantly better YoY billings than North American companies in 2018, what is clear is that 2019 will be a bust, with revenues dropping 17% YoY.

The main reason is the drop in capex spend by memory companies tied to the inventory overhang and oversupply of 3D NAND and DRAM chips. In total, capex spend is projected to drop 29.1% in 2019.

장비투자액의 감소의 주된 원인은 메모리회사들의 재고 증가와 3D낸드와 디램의 공급 과잉때문이다.

2019년 장비투자액은 전년대비 29.1%감소할 것이다.

But there is another important factor investors need to consider: market share gains and losses. Why are market shares important? Semiconductor manufacturers purchase equipment based on a "best of breed" strategy. Market share losses indicate equipment is not best of breed. When a customer decides to make additional equipment purchases to increase capacity, it will buy more from its current supplier. This means further market share gains.

'반도체-삼성전자-하이닉스-마이크론' 카테고리의 다른 글

| 일본 반도체 소재 3가지 수출 규제 (0) | 2019.07.04 |

|---|---|

| 2019년 하반기 메모리 가격 전망 (0) | 2019.07.02 |

| 실리콘웨이퍼 제조사들은 수요가 감소하고 가격이 하락하는 것을 체감 (0) | 2019.07.02 |

| 도시바 정전 사태에대한 웨스턴디지털의 공식 입장 발표 (0) | 2019.06.29 |

| 애플은 LCD 일부 주문을 중국에서 일본(재팬디스플레이)으로 전환 (0) | 2019.06.27 |

{kind=link}